Introduction

In merger and acquisition (“M&A”) transactions, the definitive purchase agreement (whether asset purchase agreement, stock purchase agreement, or merger agreement) typically contains representations and warranties made by the seller with respect to the target company.

One type of representation and warranty often requested by a buyer is commonly referred to as a “10b-5” representation, referencing the Securities and Exchange Commission’s Rule 10b-5, promulgated under Section 10(b) of the

Most representations and warranties referred to as 10b-5 representations track this language at least in part.

This article summarizes the most typical types of 10b-5 representations and examines the trends in practice with respect to 10b-5 representations in private company M&A transactions, as reported by American Bar Association (ABA) studies.

The ABA Studies

In 2005, 2007, 2009 and 2011, the ABA released its Private Target Mergers and Acquisitions Deal Points Studies.

10b-5 representations are among the many items reviewed in the ABA studies. The “sample” 10b-5 representation referred to in all four of the ABA studies is taken from the ABA’s Model Asset Purchase Agreement, and reads as follows:

No representation or warranty or other statement made by Seller or any Shareholder in this Agreement, the Disclosure Schedules attached hereto, the certificates delivered pursuant to Section ___ or otherwise in connection with the Contemplated Transactions contains any untrue statement or omits to state a material fact necessary to make any of them, in light of the circumstances in which it was made, not misleading.

This 10b-5 formulation is the “transaction-related” version described below.

Relying entirely on the ABA studies as precisely reflective of “market” practice with respect to 10b-5 representations is an inexact science, in part because:

- as discussed below, there are different versions of 10b-5 representations, and the ABA studies do not indicate which types were included in the deals under review (or how many of those deals used the model ABA representation above, versus another variation, such as the “agreement only” or “agreement and related materials” versions described below); and

- 10b-5 representations are often negotiated or discussed in connection with “full disclosure” representations. The relationship between 10b-5 and full disclosure representations is discussed below. The three most recent ABA studies differentiated between 10b-5 and full disclosure representations, but the 2005 study did not (and that study, while using the same sample 10b-5 representation as the subsequent three, set forth its results under the title of “full disclosure representations”).

That said, M&A lawyers consider the ABA studies as generally reflective of market practices. Even if one cannot discern what types of 10b-5 representations are included within the study—a problem likely inherent in categorizing any particular type of M&A representation—the studies should provide a reliable picture of how often 10b-5 representations (broadly described) are included within private company M&A transactions.

Common Variations of 10b-5 Representations

While there are many potential variations of 10b-5 representations, there tend to be three variations most commonly seen in practice. All three 10b-5 representations refer to both: (i) untrue statements; and (ii) statements made misleading by omission. The three variations are set forth below.

1. The “Agreement Only” 10b-5 Representation.

a. Sample Language: “None of the representations and warranties in Article __ of this Agreement, taking into account the Disclosure Schedules attached hereto, contain any untrue statement of a material fact or omit a material fact necessary to make each statement contained herein or therein, in light of the circumstances in which they were made, not misleading.”

b. Observations: When referring only to statements in the purchase agreement, the “untrue statement” portion of a 10b-5 representation is arguably circular and confusing. If a representation in the agreement contains “an untrue statement of material fact”, then it’s hard to imagine how the primary representation itself has not been breached. The statements in a representation or warranty are either correct or incorrect (which seems logically the same as being true or untrue). A negotiated representation related to a particular topic “stands on its own” with respect to the truthfulness of statements contained therein.

The value to the buyer of this “agreement only” 10b-5 representation, if any, is therefore due to the “misleading by omission” aspect, which arguably adds an additional standard that may be broader than a “true or untrue” standard. However, even here it is difficult to imagine how a specific representation (with or without related disclosures) could be true and correct (i.e., not breached), and yet still be “misleading.” If an environmental problem at the target arises or is discovered following the closing of the transaction, and that issue is not contrary to the language of the environmental representation in the agreement (which is often a heavily negotiated representation), is the fact of that problem an “omission” that has made the relevant environmental representation “misleading?” How is this the right result if the buyer is a sophisticated party negotiating the topic-oriented representations and warranties?

2. The “Agreement and Related Materials” 10b-5 Representation.

a. Sample Language: “None of the representations or warranties in this Article ___ nor any of the Exhibits or Schedules attached hereto, nor any of the certificates delivered pursuant to Section ___, contain any untrue statement of a material fact or omit a material fact necessary to make each statement contained herein or therein, in light of the circumstances in which they were made, not misleading.”

b. Observations: This version of the 10b-5 representation contains the same “circularity” problems discussed above insofar as it covers the truthfulness of the statements made in other representations and warranties in the agreement, but it goes beyond the agreement’s representations and warranties to also apply to any closing certificates and any schedules or exhibits attached to the agreement. This broadens the scope considerably - - if, e.g., company promotional materials were attached to a disclosure schedule (which would not be unusual), this version of the 10b-5 representation would apply to those materials. And conceptually, it is easier to understand how sales promotional materials might be found to be misleading by omission of a material fact even where a negotiated representation or warranty in the principal agreement is not breached.

3. The “Transaction Related” 10b-5 Representation.

a. Sample Language: “No representation or warranty or other statement made by Seller or any Shareholder in this Agreement, the Disclosure Schedules attached hereto, the certificates delivered pursuant to Section ___ or otherwise in connection with the Contemplated Transactions contains any untrue statement or omits to state a material fact necessary to make any of them, in light of the circumstances in which it was made, not misleading.”

b. Observations: This version of the 10b-5 representation is the broadest, and most pro-buyer, of the three. This type of 10b-5 representation is reflected in the ABA Model APA, though in the authors’ experience is not commonly seen in practice. Significantly, this version covers not only representations and warranties, but also any “statements” within closing certificates or Disclosure Schedules (including attachments), and any statements made by the seller “in connection with” the transactions—which by its terms would not be limited to the “four corners” of the transaction documents but would arguably include “statements” made during business meetings, management presentations, due diligence production, conference calls and otherwise.

Relationship of 10b-5 and Full Disclosure Representations

As noted above, 10b-5 representations are often discussed in conjunction with “full disclosure” representations, though the two are different in approach and focus. An example of a full disclosure representation, which is set forth in the ABA Model APA, is the following:

Seller does not have Knowledge of any fact that has specific application to Seller (other than general economic or industry conditions) and that may materially adversely affect the assets, business, prospects, financial condition or results of operations of Seller that has not been set forth in this Agreement or the Disclosure Letter.

This type of representation is highly buyer-oriented, and (as reflected in the ABA studies), relatively rare, particularly in the absence of an accompanying 10b-5 representation.

Another version of a full disclosure representation, arguably narrower in scope than the representation above, focuses on the buyer’s due diligence checklist:

“Seller has provided to the Buyer all information and materials responsive to the Buyer’s due diligence checklist attached hereto as Schedule ___.”

This representation may be appropriate where there is reason for the buyer to have concerns with the sellers’ disclosures or the disclosure process, and it may help “sharpen” the seller’s focus on the specific diligence checklist responses.

Trends in Usage of 10b-5 Provisions

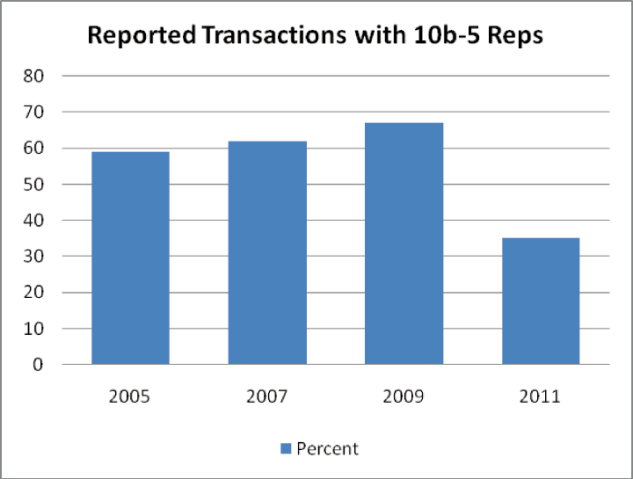

As reflected in the table below, according to the ABA’s studies, 10b-5 representations were reported in 59 percent, 62 percent, and 67 percent of reported transactions in the first three studies, respectively.

Conclusion

Assuming that the ABA studies reasonably reflect general practice in private company M&A transactions, it appears that there has been a sharp drop-off in the inclusion of 10b-5 representations between the deals included in the 2009 study to those in the 2011 study, following a modest increase from the 2005-2009 studies.

Whether or not a 10b-5 representation is to be included in an M&A agreement is often a heavily negotiated point. As discussed above, the different variations of these representations significantly impact risk allocation as between buyer and seller. Counsel on both sides of an M&A transaction should consider these issues carefully when negotiating 10b-5 representations.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.