For the next five years, the No. 1 tax issue facing multinationals may center on valuation; the financial stakes are enormous—and the rules are yet to be written.

The Organization for Economic Cooperation and Development has just started a major project on valuation of intangibles, with a scoping paper released in January 2011 and a discussion draft targeted for 2013.

Across the globe, controversies concerning valuation are on the rise. In the multibillion-dollar case Veritas Software Corp. v. Comr., 133 T.C. 297, the IRS—although it did not prevail in the dispute—sent a message that stock market values will be used to challenge related-party valuations based on internal projections. The Vodafone case in India and the Carlyle case in China signal that the tax authorities are aware of the enormous increase in value of entities in their countries and are extending the tax net accordingly.

Exacerbating the controversies is the fact that valuation is frankly an area that is new, or at least relatively unfamiliar, to many transfer pricing professionals and tax inspectors. The transfer pricing regulations are virtually silent on how to do a valuation, and the income method—the cornerstone of the IRS’s approach to valuing cost-sharing buy-in payments—is not even mentioned in the OECD transfer pricing guidelines.

There does exist a parallel universe of valuation professionals, who work within appraisal firms, and who do nothing else but valuation. Their studies are usually done in the context of initial public offerings (IPOs), acquisitions, sales of businesses, and other situations where a valuation is mandated, rather than as part of a tax engagement.

At this point, the transfer pricing community is at a crossroads in terms of its future with regard to valuation projects. A majority of clients are engaging appraisal firms for valuation studies required in the context of transfers of equity. For transfer pricing professionals to stay relevant in the valuation space, they will need to adopt new methods even before the release of the OECD discussion draft.

This article is addressed to the international transfer pricing community and is an outcome of a number of initiatives taken by the author to bridge the gap between the financial and tax-based approaches to valuation, including a five-day meeting in October 2011 organized by the OECD and China’s State Administration of Taxation on the valuation of intangibles and attended by the head of the OECD transfer pricing group, the chair of Working Party No. 6, senior officials from the Indian Ministry of Finance, and more than 100 of China’s leading transfer pricing officials.

Valuation Framework

These days, tax bureaus are requesting studies conducted by appraisal firms in the case of an acquisition. Upon the acquisition, an appraisal firm is engaged to conduct a purchase price allocation (PPA) study, which is conducted according to well-defined international financial reporting standards. The following are the key attributes of a PPA study:

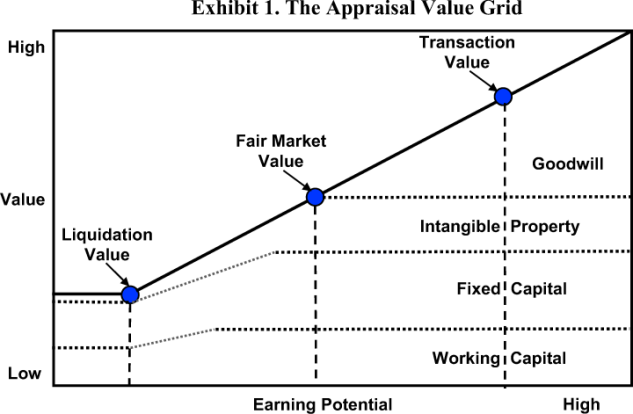

- The acquisition price will be allocated to the following four value blocks: working capital, fixed capital, intangible property, and goodwill.

- Where intellectual property can be separately recognized and valued by the appraiser, separate valuations are undertaken for each key element of IP, such as brand name, patents, and copyrights.

- The total acquisition price minus the book value minus the IP will be a residual and this residual will be classified as goodwill. In effect, goodwill is that excess amount paid for the acquisition that cannot be attributed to either tangible assets or IP.

- After the assets have been valued, there is an annual impairment analysis done on both the goodwill and the IP to assess whether there has been any loss in the value of either IP or goodwill.

- The IP will be amortized over for a period (for example, 20 years in the United States). Goodwill is not amortized.

The following figure shows the four value blocks as derived in a PPA study. Note that if a company is liquidated, it probably will have zero IP and goodwill. Also note that the difference between transaction value and fair market value usually ends up as goodwill.

Areas of Controversy

A number of unresolved controversies make valuation for tax purposes a highly fluid subject. In this section, the principal points of controversy are collected to define the center of future disputes between taxpayers and tax authorities.

Conflicts Between PPA, Tax Studies

PPA estimates and tax estimates can differ. In particular it has been noted that the valuation derived by tax-based professionals is significantly lower than the value that would be implied by examining the acquisition data or other data on the stock market. Since the tax-based analysis is focusing mainly on related-party transactions and because there is a clear benefit to understating values, there is sometimes the suspicion that the tax-based valuation has been rigged to come up with an artificially low value.

To illustrate, say a U.S. parent acquires a company for $120 million, of which $100 million was for its technology. The overseas rights to the technology of that company are then transferred to a related party in Ireland for $5 million. However, the overseas market is 50% of the global market, which implies that the Irish company should have paid $50 million, not $5 million.

Certainly, IRS is using stock market data aggressively. For example, in Veritas, IRS’s expert, Brian Becker, challenged the transfer of IP from the United States to Ireland at a market value of $118 million as being much lower than the values at which subsequent acquisitions were made by Veritas. He noted that Veritas acquisitions, if used as a benchmark to analyze the IP migration to Ireland, would have translated into estimates of between $1.9 billion and $4.4 billion. Becker ultimately decided that a $2.5 billion buy-in payment was appropriate.

Importance of Goodwill

As noted earlier, goodwill associated with a company is in a practical sense derived as residual. In the context of valuation, a highly contentious issue will be the amount assigned to goodwill. As a guideline, goodwill normally should not represent more than between 30% and 40% of the value of the company; however, the author has seen cases in which as much as 97% of the value of the company was assigned to goodwill.

There are two reasons to overstate goodwill. First, goodwill, unlike other elements of IP, is not amortized. Thus, by allocating more to goodwill, earnings as reported for stockholder purposes will not be reduced by an amortization charge. Therefore, from a stockholder reporting point of view, there is a benefit to allocating more to goodwill and less to other elements of IP.

Second, for tax purposes, the greater the amount allocated to goodwill, the less the amount available to go to specific IP. Therefore, if the IP is migrated to another jurisdiction, then there is a basis to justify a lower transfer price.

In the United States,

Market, Buyer-Specific Synergies

In the context of synergies, it is necessary to differentiate between a financial buyer and a strategic buyer. A financial buyer is concerned solely with the stream of income from the asset or enterprise and does not intend to fundamentally alter or take control of the enterprise. For example, an individual stockholder can be regarded as a purely financial buyer. Similarly, a private equity fund can be regarded as a financial buyer.

By contrast, a strategic buyer is an acquirer who has specific reasons for taking over the target company and may substantially alter the company upon its takeover. Acquisitions conducted by strategic buyers sometimes are done at a price that is significantly above the stock market value.

The term “market synergies” refers to the fact that both a strategic investor and a financial investor may wish to acquire a company at a premium, feeling that the acquired company has not fully exploited its potential by, for example, tapping new markets. These synergies are known as market synergies because they do not require any special expertise on the part of the buyer.

Strategic investments recently have occurred in the beer industry. Many foreign breweries have acquired Chinese breweries that are in loss positions because they wanted a gateway to the Chinese market. These foreign breweries had access to brand names and technology that they could freely make available to the Chinese acquisitions, adding significant value. Therefore, a foreign brewery might be willing to pay much more than a private equity fund would for a Chinese brewery.

Control Premium

Another concept relevant to the issue of how much would go to goodwill as opposed to IP is the so-called control premium. Typically, a control premium can be worth between 20% and 40% of the deal value and reflects the fact that the buyer is willing to pay extra to get the complete control that is possible only with 100% ownership.

It has long been acknowledged that a controlling interest in another business entity embodies valuable rights not available to a noncontrolling interest. Included are the rights to appoint management, determine management compensation and perquisites, set policy, change the course of business, acquire or liquidate assets, and pay a dividend.

Marketability Discount

Another controversial issue affecting the amount that should go to goodwill is the so-called marketability discount. In some cases when the acquired company is a private company, the buyer insists on a discount because the shares of a private company cannot be marketed easily. Therefore, the acquisition of a private company typically would be made at a discount compared to the acquisition of a publicly listed company. This discount is known as the marketability discount.

Studies of restricted stock suggest that private transactions take place at an average discount of approximately 35% relative to the price in the same share in the IPO market.

Case Studies

A dramatic example of anticipated buyer-specific synergies and control premium is the 200% premium offer by Coca-Cola, the world’s largest soft drink company, in its offer to buy Hui Yuan at a cash price of $2.5 billion. This offer was 43 times Hui Yuan’s forecasted 2008 earnings and nearly three times its stock market valuation at the time.

Hui Yuan was the leader in the Chinese fruit juice market, closely followed by Coca-Cola. Coca-Cola was willing to pay such a high premium because it hoped to strengthen its grip on the Chinese domestic juice market. Ultimately, the bid was blocked on the ground of antitrust violations.

Another example is the 2004 acquisition by Anheuser-Busch, then the largest beer company in the world, of Harbin Brewery at a price that was more than double its formally traded stock value. Harbin Brewery already was partially owned by SAB Miller, the second-largest brewery in the world. Harbin Brewery is a regional brewery that is dominant in certain parts of Northern China.

The acquisition at more than double the market value was based on the plans that Anheuser-Busch had for extending the Harbin Brewery brand and capitalizing on its distribution network to sell the Budweiser brand.

Going Concern, Workforce in Place

IRS has become convinced that taxpayers are avoiding U.S. tax consequences by attributing the majority of the assets’ value to foreign goodwill and going concern value. For example, a U.S. corporation that operated a global delivery business relying on a network of agents located in many different countries attributed 3% of the value of its network to identifiable intangible assets—specifically, to its contracts—and 97% of the value of the network to foreign goodwill and going concern value (which are not taxable).

However, recent proposals by the Obama administration indicate that despite the language in

A description of the proposals by the Joint Committee on Taxation explicitly confirms what a number of taxpayers already are facing in audits: IRS takes the position that, even absent the administration’s proposed change, workforce in place, goodwill, and going concern value are intangibles under current law.

Valuation of Captive Subsidiaries

This is an issue of enormous relevance to transfer pricing professionals because it involves related-party transactions. In China, as well as in certain other jurisdictions, the internal transfer of a subsidiary may be subject to capital gains. It has been typical for companies to make these internal transfers at book value, and this practice continues even though the book value may be significantly below the market value.

To defend this position, taxpayers assert that because the subsidiary is of a captive nature and relies 100% on funding by the parent company for its revenue, it would not be able to survive as a freestanding entity.

However, this argument fails to recognize that the relative bargaining power between the parent and the subsidiary may vary from situation to situation. In addition, it fails to give recognition to the fact that the subsidiary might have what is referred to as going concern value and a workforce in place and, should the subsidiary cease to exist, the parent would have to undergo a certain amount of cost to create a going concern and establish a new workforce.

Therefore, in the valuation of captive subsidiaries, it is necessary to explore:

- the ability of the parent company to replace the functions and services performed by the captive unit;

- the ability of the captive unit to find an alternative source of funding for its services; and

- the extent to which intercompany arrangements between the parent and the subsidiary allow for contract termination and reflect arm’s-length considerations.

Pyramid of Valuation Methods

The transfer pricing methods currently in use are either ineffective or inadequate for the purpose of conducting a valuation. In particular, note that the OECD transfer pricing guidelines—which were revised in 2010 and represent the gold standard for the analysis of related-party transactions—identify five methods, all of which are essentially static and focused on single-year profitability. These methods are appropriate for the sale of a product or service, but not for sale of a valuable asset or an equity transfer, where there is a long-term cash flow.

IRS in its revised cost-sharing regulations has filled the breach by proposing new methods.

It is imperative that transfer pricing professionals become proficient in new types of methods. The choice of a method is a critical decision in the valuation process. Some methods tend to produce low values and others tend to produce high values. For example, the asset cost method will produce a valuation estimate that is close to liquidation value, while the market capitalization method will produce a significantly larger estimate of the value.

The accompanying table lists 10 possible methods and indicates the extent to which they are suitable for a valuation report. The methods are listed in order of their suitability for the purpose of valuation. For example, the income method, which is the method used most frequently in valuation, is listed first. At the bottom are such methods as cost plus and resale minus, which are traditional transfer pricing methods based on annual profit data and are not suitable for the purpose of valuation.

Methods Described

The income method evaluates a company strictly from the point of view of a financial investor who is acquiring a company or asset for the cash that it can generate. The income method derives a value for the enterprise equal to discounted sum of the future cash flows. It is the workhorse of the valuation professionals and is used for ongoing concerns.

The market method uses stock market data and will involve valuing the equity of the target company relative to certain economic indicators and referring these to the actual ratios observed among either publicly listed companies or publicly disclosed acquisition cases.

In the market capitalization method, IRS once again is signaling that stock market data needs to be taken into account in deriving a value for the asset. IRS in an example under the final cost-sharing provisions at Regs.

Example: (i) USP, a publicly traded U.S. company, and its newly incorporated wholly-owned foreign subsidiary (FS) enter into a CSA on Date 1 to develop software. At that time USP has in-process software but has no software ready for the market. Under the CSA, USP and FS will have the exclusive rights to exploit the software developed under the CSA in the United States and the rest of the world, respectively. On Date 1, USP’s RAB share is 70% and FS’s RAB share is 30%. USP’s assembled team of researchers and its in-process software are reasonably anticipated to contribute to the development of the software under the CSA. Therefore, the rights in the research team and in-process software are platform contributions for which compensation is due from FS. Further, these rights are not reasonably anticipated to contribute to any business activity other than the CSA Activity.

(ii) On Date 1, USP had an average market capitalization of $205 million, tangible property and other assets that can be reliably valued worth $5 million, and no liabilities. Aside from those assets, USP had no assets other than its research team and in-process software. Applying the market capitalization method, the value of USP’s platform contributions is $200 million ($205 million average market capitalization of USP less $5 million of tangible property and other assets). The arm’s length value of the PCT Payments FS must make to USP for the platform contributions, before any adjustment on account of tax liability as described in paragraph (g)(2)(ii) of this section, is $60 million, which is the product of $200 million (the value of the platform contributions) and 30% (FS’s RAB share on Date 1).

The acquisition price method has been put in place by IRS to deal with the scenario where a company makes an acquisition subsequent to a cost-sharing arrangement and wishes to transfer the rights of the acquired company and include them as part of the cost-sharing arrangement. IRS is stating that in this particular case, the value at which the acquisition has been made must be considered in deriving a value for the transfer of the IP.

The asset cost method is used by appraisal firms and is suitable for determining liquidation value. This method also should be used for an ongoing company. The asset cost method evaluates all the assets of the target company and liabilities to get the net asset value. When using the asset cost method, each asset should be separately evaluated as necessary. To apply the asset cost method, the appraisal firm will inspect the assets and examine price guides to assess the price at which specific equipment could be sold. The physical depreciation and technological obsolescence will be factored into the estimates.

The comparable uncontrolled price (CUP) and comparable uncontrolled transaction (CUT) methods involve finding a situation where a similar intangible asset or enterprise has been sold or licensed and using that as the basis for establishing the fair market value. It should be noted this method is favored by taxpayers but not by tax authorities. For example, the JCT in its description of the Obama administration’s 2010 transfer pricing proposals advocated authorizing the income method (or other methods that do not rely on comparables) unless exact comparables exist.

The profit split method, like CUP and CUT, is one of the five methods authorized by the OECD transfer pricing guidelines and is more suited for traditional transfer pricing than for valuation. However, IRS has included it as a method that might be used in the valuation context.

The transactional net margin method (TNMM), also an OECD method, is static and based on comparing the profit of the tested party in any specific year with the profit of comparable companies in that year. It is not useful for an asset whose value derives from a future stream of income that can be generated.

The cost plus method is based on benchmarking profitability in a given year, typically for a contract manufacturing or contract service company. Although it is an OECD method, it is not suitable for valuation.

The resale minus method, like the cost plus method, is one of the five OECD transfer pricing methods but also is not suitable for valuation.

Conclusions

The stakes involved in tax-based valuation are considerable and there is much uncertainty regarding methods and their applications. The OECD selection of valuation as its prime area for transfer pricing investigation for the next three years is one indication of its centrality.

The income method is far and away the No. 1 choice for valuation, and there is a groundswell of support among tax authorities for its use. However, this method relies mostly on internal assumptions and therefore its use will create never-ending controversies. More objective and scientific approaches are needed. Stock market data has the potential for misapplication but has the advantage of placing the taxpayer and the tax authority on an equal footing.

The transfer pricing profession is at a crossroads with regard to its role in valuation. The message is clear: The profession will need to adapt and innovate to stay relevant in the valuation space, especially in the context of those valuations that involve transfer of equity.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.