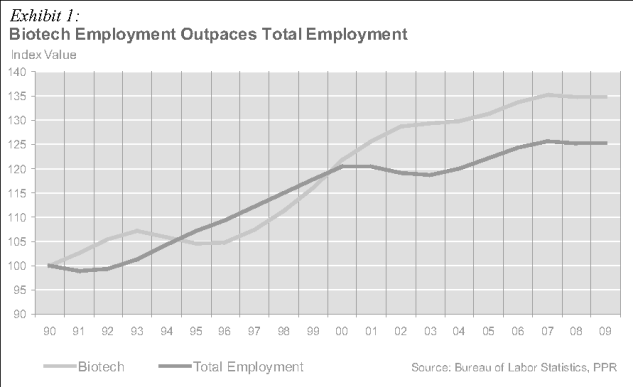

It’s no secret that the nation’s demographics are changing. The largest generation in the country’s history, the baby boomers, are getting closer to retirement (or at least they were until the economy collapsed). By 2025 there will be nearly 64 million Americans 65 years or older, 18 percent of the population, compared to less than 13 percent today, per U.S. Census Bureau estimates.

The technological advances made in studying the human genome are expected to open up a new wave of drugs and medicines to cure even the rarest of diseases. Research into preventive medicine could be a key contributor in reining in the nation’s soaring heath care costs. Another area of biotech outside of drug manufacturing and research is genetically modified food. St. Louis is in the forefront of this as Monsanto, along with the Donald Danforth Plant Science Center and Washington University, have created an industry cluster there. Unpredictable weather patterns have increased the need for drought- and insect-resistent seeds and plants. Alternative fuels such as biofuels are another sector of potential growth, and research is being done on the viability of algae and other plants as fuel sources. It’s clear that there are many areas of potential growth within this industry.

Biotechnology has various definitions,

But despite the relative longevity of the biotech industry, only a handful of markets can really lay claim to being legitimate biotech hubs. The Brookings Institution defines the top nine biotech centers by CMSA (Consolidated Metropolitan Statistical Area), which are broader than PPR-defined metros, as follows: Boston and San Francisco (the biotech leaders, including Oakland and San Jose); San Diego, Raleigh-Durham, and Seattle (the biotech challengers); New York (including North-Central New Jersey and Long Island) and Philadelphia (the nation’s pharmaceutical centers); and Los Angeles (including Riverside and Orange counties) and Washington-Baltimore (other biotech centers, due to their large share of National Institutes of Health (NIH) funding and company headquarters).

Boston and San Francisco, considered the dominant biotech markets in the United States, were at the forefront of this industry back in the 1970s, thanks to their strong research institutions and highly educated workforces. Today they rank as top recipients of NIH funding and biotech venture capital (VC) spending. From 1995–2008, Silicon Valley and New England, with San Francisco and Boston as the pillars of those regions, received 43 percent of all biotech VC spending, according to PricewaterhouseCoopers (PwC). This trend should persist into the foreseeable future, because they continue to be anchored by strong research universities and colleges as well as by hospitals.

Such activity clusters are a competitive challenge for other cities lacking this critical mass. San Diego and Raleigh are the closest challengers, as they have a similar potential for clustering activity (good schools, biotech operations in place, well-educated and specialized workforce, etc.). But metros without a strong presence of research institutions and public policy to lure these types of firms will miss out on the industry’s growth potential. So although research in biotechnology is widespread, established biotech hubs have maintained their dominance in securing these funds, further cementing this industry to those key locations.

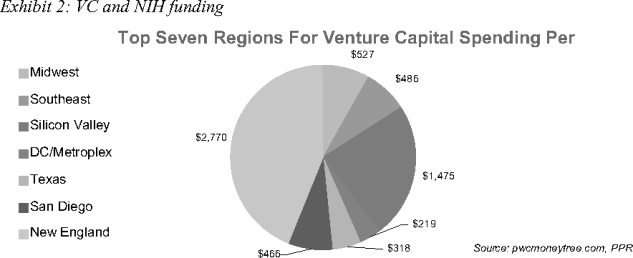

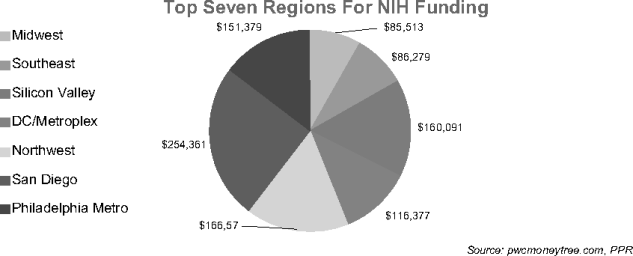

Biotechnology has been a key beneficiary of VC spending in the last 10 years (1999–2008), attracting investment of more than $7 billion. That tally ranks fifth of the 17 categories tracked by PwC. However, over the five years ending in 2008, biotech ranked only third for VC capital flows, with nearly $4 billion, after software and industrial/energy. In addition, biotech continues to grab a larger piece of the VC pie. This support, along with the priorities set in Washington, bode well for growth. In the American Recovery and Reinvestment Act, $9.5 billion was allocated for spending by NIH for biomedical research, while another $2.5 billion was allocated to the National Science Foundation for research. These funds dwarf what the VC has spent in biotech over the past decade, and ancillary benefits and job growth in key biotech hubs along the coasts should be expected. But growth is likely to come from more than just the coasts. Exhibit 2 shows VC spending and NIH allocations (for 2007, the last year of complete data tallies) per capita, based on PwC’s VC regions. VC spending is concentrated in the top biotech hubs (which bodes well for job growth and new company startups), while NIH funding is spread out far more evenly (which bodes well for increased development of new facilities and hiring at local colleges and universities and research institutions).

So which property types will win out if biotech is the next big thing? Biotech is not a true traditional office story, since these firms require specialized space, but medical office and other specialized office space will benefit. It’s not really a warehouse play, either, as these innovations are not easily stored in warehouses. Apartment investment, however, will benefit from the household formation that quality jobs and ancillary impacts of this expanding industry bring. Retail is also a winner, as retail demand is broken down to bodies-times-dollars (biotech jobs are higher-paying than average). Metros like Boston and San Francisco are not fast-growth demographic markets, but they are high-income markets. And with further specialization into emerging industries and cutting-edge technology such as biotech, retail sales growth should benefit. The trickle-down effect of high-paid jobs requires service workers (restaurants, retail stores, etc.) and will also fuel retail sales growth.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.