Introduction

In merger and acquisition (“M&A”) transactions, the definitive purchase agreement (whether an asset purchase agreement, stock purchase agreement, or merger agreement)

In negotiating these provisions, sellers seek to narrow, as much as possible, the scope of indemnification for breaches of the reps and warranties. Typically, this means including various restrictions as to the types of claims available and damages covered, as well as limiting the time period within which claims may be brought. One such limitation often negotiated between buyer and seller in this context involves whether the exclusions and restrictions otherwise reducing the seller’s indemnification exposure should apply equally to a breach of the reps and warranties that was “willful” or “intentional” (as opposed to “accidental” or “unintentional”).

Biennially, the American Bar Association (“ABA”) releases its Private Target Mergers and Acquisitions Deal Points Study (the “ABA study”). The ABA study examines the publicly available M&A purchase agreements for acquisitions of privately-held companies that occurred in the year prior. In 2005, 2007, 2009, 2011 and 2013, the studies reviewed 150, 143, 106, 100 and 136 of these private company transactions, respectively. These transactions ranged in size from $17 million to $4.7 billion, across a broad range of industry sectors.

This article looks at how sellers and buyers deal with intentional breaches of reps and warranties by the seller—and the indemnification coverage applicable to such breaches—in private company M&A transactions.

State of Mind and Breach

That an actor’s state of mind may impact its liability to a party aggrieved by such actor’s wrongful conduct is not a novel concept in law. A person’s punishment for killing another may well depend upon his or her state of mind at or around the time of the crime—hence, the distinctions in criminal law between murder, voluntary manslaughter and involuntary manslaughter. Similarly, a defendant’s state of mind or intent may also expose him or her to increased liability or damages resulting from particular wrongful conduct in a civil setting. The legal concepts of, and distinctions between, negligence, gross negligence, willful misconduct, recklessness, and scienter reflect the significance of intent, even where the categories may be closely related and/or the subject of confusion and misuse.

However, state of mind and intentionality concepts are applied much less frequently to claims arising under contract—instead, what is usually considered most important is whether the contract was breached or not. As Oliver Wendell Holmes once stated, “[t]he only universal consequence of a legally binding promise is, that the law makes the promisor pay damages if the promised event does not come to pass. In every case it leaves him free from interference until the time for fulfilment has gone by, and therefore free to break his contract if he chooses.”

As a practical example, if you enter into a contract with a roofing installer who breaches the contract by using inferior shingles instead of the higher grade called for in the contract, and the roof leaks, do you care much about whether the contractor intended to use lousy materials or whether it was accidental? Either way, you want the roof fixed and your living room dry. If, however, your contract with the roofer exculpates him or her from any liability other than for breaches that are willful or intentional, then your contractor’s state of mind becomes paramount.

Intentional Breaches of Representations and Warranties in M&A Transactions

In the M&A context, suppose that a seller represents and warrants that it has disclosed all pending and threatened litigation and claims, but fails to disclose that a significant customer had recently sent a letter to the target company stating a willingness to pursue “all available legal remedies” if the company did not satisfactorily resolve the customer’s complaints with respect to its products. The failure to disclose this matter may well constitute a breach of the seller’s representations. If the transaction closes, the buyer now has to deal with a potential issue it had not bargained for, and has probably suffered damages as a result.

Does it matter whether the seller knew it should have disclosed the customer letter but decided—intended—not to? Does it change the value of the business if the failure of disclosure was simply an oversight—for example, if the customer correspondence was in a pile of materials to be summarized for disclosure but was inadvertently overlooked? Or that the seller was well aware of the overall disclosure obligation but felt in good faith that the customer complaint did not rise to the level of a “threatened claim” actually requiring disclosure? What if the seller was taking a chance by concealing the potential claim, betting that it would not otherwise be indemnifiable due to other limitations?

The damages to which the buyer is entitled upon breach of a seller’s reps and warranties in an M&A purchase agreement may be subject to numerous limitations: restrictions in type (such as exclusions for consequential or indirect damages)

In turn, a seller and buyer will usually negotiate specific “exclusions from the exclusions”—i.e., certain matters which are not to be subject, in whole or in part, to some or all of the limitations on seller indemnification. These tend to be matters which are considered sufficiently serious or critical to the underlying transaction or target such that, from the buyer’s viewpoint, the seller should be willing to stand behind the related reps and warranties fully and without exception.

For example, representations and warranties considered “fundamental” often are exempt from the time limitations, baskets and caps applicable to the buyer’s recourse for breaches. These fundamental representations typically relate to such matters as title to assets or equity, pre-closing taxes, retained liabilities, or other items or categories of specific concern identified during the buyer’s diligence.

In many cases, a buyer will seek to treat “willful” or “intentional” breaches of representations and warranties differently than “normal” or “unintentional” breaches. Specifically, a buyer may push to exclude a seller’s “intentional” breaches of reps and warranties from the various limitations and restrictions which would otherwise be applicable to the seller’s indemnification obligations (and the buyer’s rights of recovery)—which in practice would usually mean treating intentional breaches of any representation or warranty in the same category of seriousness as breach of a fundamental representation or warranty.

In so doing, the seller’s intent or state of mind becomes a dispositive factor in determining the extent of a buyer’s recovery for certain breaches. A purchase agreement provision excluding willful or intentional seller breaches from indemnification limitations—an “intentional breach carve out”—seeks to treat any intentional breach, no matter the underlying subject matter, as critical.

The Seller’s Argument

In negotiating whether willful or intentional breaches should be relevant to its indemnification obligations the seller will assert that Justice Holmes “had it right,” and that a breaching party’s state of mind should be irrelevant to a buyer’s rights of recovery and a seller’s liability.

If such a breach is actionable, or “more actionable” by a buyer if it is considered “intentional,” won’t that buyer always assert “intent” with respect to such breach of a rep or warranty? For a “garden variety” disclosure omission, the buyer will always argue that the seller “intended” not to disclose. Or for a direct breach of an affirmative statement, the buyer will maintain that the seller knew or should have known of the breach, or “intentionally” chose not undertake the appropriate level of inquiry needed to determine the veracity of the statement.

In other words, the seller will argue that introducing intent into the world of contractual breaches for reps and warranties adds a significant level of complexity, proof and uncertainty into indemnity claim dispute resolution, and is, in any event, irrelevant to the damages suffered by the buyer as a result of the breach. So long as a buyer can recover its damages for the breach, a seller will argue, intent should have no bearing on the claim.

The Buyer’s Argument

The buyer, of course, will argue that the seller’s state of mind should in fact be relevant to the seller’s indemnification, at least in certain circumstances. Specifically, a buyer may assert that:

1. exposing the seller to potentially greater exposure for “intentional” breaches will motivate the seller to do its own vigrorous due diligence to uncover and disclose everything necessary, and that it will remove the seller’s incentive to hide a potential claim in the hope that it would fall outside of its indemnification obligations due to the restrictions otherwise applicable to an “unintentional” breach;

2. successfully proving willful or intentional breach by the seller is difficult absent clear evidence, so in situations where there is in fact such proof, a higher level of seller accountability is appropriate; and

3. “intentional” breaches are arguably a form or variation of fraud, and fraud claims usually are not subject to limitations on the seller’s indemnification obligations.

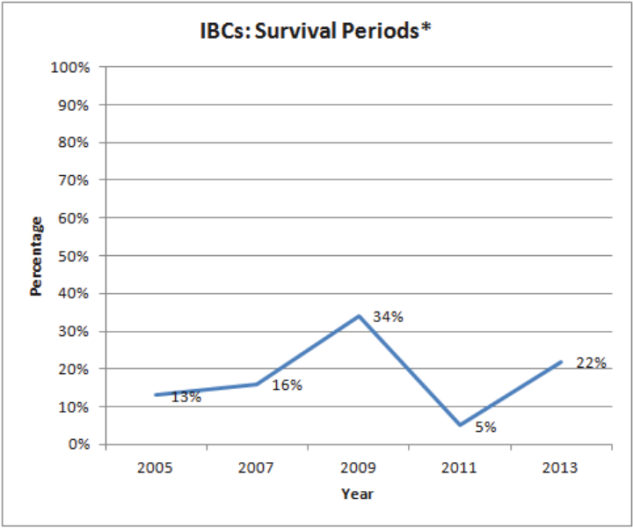

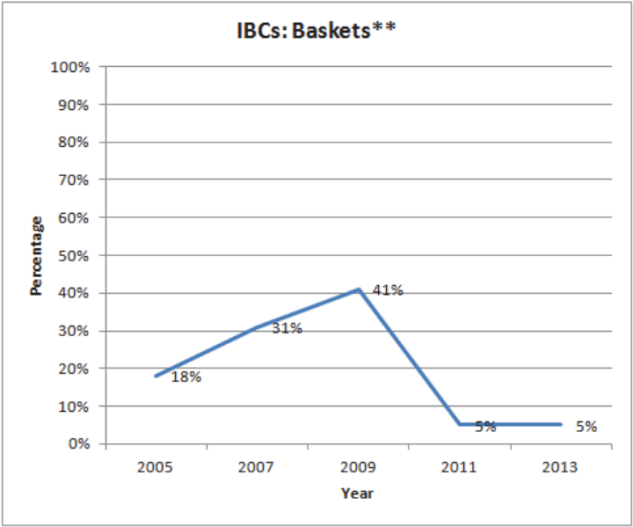

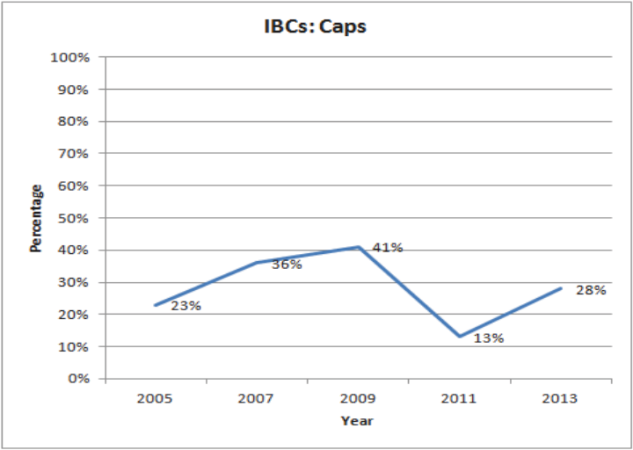

Trends in Intentional Breach Carve-Outs

With these arguments in mind, the charts below show the prevalence and elements of intentional breach carve-outs over the past decade, as compiled by the ABA studies. These charts specify the frequency of intentional breach carve outs from: (i) representation and warranty breach survival periods, (ii) indemnity baskets; and (iii) indemnity caps, in each case expressed as the percentage of deals in which such “exclusions from the exclusions” appears.

* The ABA studies identify where a component is reported under 10% in this area without a specific number; in those cases in these three charts, we have assigned 5% as the “assumed” percentage. In the first chart, that assumed percentage of 5% is used for 2011.

** Assumed percentage of 5% used for 2011 and 2013.

Conclusion

Based on the ABA studies, inclusion of intentional breach carve outs in M&A purchase agreements became increasingly common between 2004 and 2008, dropped significantly at the time of the US recession in 2010, and have seen a rebound in 2012 (other than with respect to indemnity baskets). It’s difficult to know whether there is any connection to the state of the economy—one would think that buyers were fewer and had more negotiating strength during the economic downturn, so an uptick, not a drop, in buyer-friendly intentional breach carve-outs would have been expected. Unlike many of the other customary limitations on a seller’s indemnification obligations (and in particular those tied to such factors as time or dollar amount),

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.