The Centers for Medicare & Medicaid Services (“CMS”) has proposed changes to the risk adjustment program—the permanent premium stabilization program under the Affordable Care Act (the “ACA”)—for the 2018 benefit year.1Proposed HHS Notice of Benefit and Payment Parameters for 2018 (“2018 Proposed NBPP”), 81 FR 61455, 61466-491. The risk adjustment program transfers funds from plans with healthy enrollees to plans with relatively sick enrollees. This mitigates the harm of “adverse selection” by compensating an insurer who is selected by enrollees with chronic conditions. It also incentivizes insurers to not engage in “risk selection” or “cherry picking”—a practice whereby insurers seek to target healthy enrollees and avoid sick enrollees by, for instance, selling plans that do not appeal to sick enrollees or by only marketing to healthy individuals.2Further detail as to the processes of “risk selection” and “adverse selection” may be found at Final HHS Notice of Benefit and Payment Parameters for 2014 (“2014 Final NBPP”), 78 FR 15409, 15411-13 (Mar. 11, 2013) and Henry J. Kaiser Family Foundation, Explaining Health Care Reform: Risk Adjustment, Reinsurance and Risk Corridors (Aug. 17, 2016), available at http://kff.org/health-reform/issue-brief/explaining-health-care-reform-risk-adjustment-reinsurance-and-risk-corridors/ .

In its most recent proposed rule, CMS suggests including a “high-cost risk pooling” mechanism that would collect a payment from all risk-adjusted insurers and would use those funds to pay insurers for a portion of member claim costs in excess of an attachment point. If this sounds like a new permanent reinsurance program, that is because it is one. The proposal is motivated by a concern that there are insurance markets that are too small to handle extremely high-cost enrollees. A risk adjustment model attempts to reflect average costs for a condition, but there is always a range of costs, and for high-cost conditions that range can be exceedingly large. So ideally, a high-cost reinsurance pool would allow an insurer in a small market who expects to enroll a particularly expensive member, i.e. a hemophiliac, to pass some of the cost to the pool rather than having to raise rates to the point where healthier members are driven away, destabilizing the market.32018 Proposed NBPP, supra note 1, at 61471-72.

This new proposal, while well intended, could create adverse effects that may very well outweigh the benefit of any risk-sharing, including new political challenges or litigation, controversy over cross-regional subsidization, gaming opportunities for providers or insurers, and uncertainty over the program’s cost.

The risk adjustment program has already been the subject of controversy and litigation, with plans citing inflated risk adjustment charges as the basis for exiting the exchanges or closing their doors altogether. This new proposal, while well intended, could create adverse effects that may very well outweigh the benefit of any risk-sharing, including new political challenges or litigation, controversy over cross-regional subsidization, gaming opportunities for providers or insurers, and uncertainty over the program’s cost. CMS has recognized some of these concerns, but its suggestions in response water down the proposal to the point that it provides little or no meaningful protection to unstable markets.

In sum, although a reinsurance pooling mechanism to reduce the impact of high-cost outliers is a laudable endeavor, the current proposal is much like whipped cream on top of a chocolate mocha. It may look good, but it is largely unnecessary, potentially ineffective and may cause more harm than benefit. There may be more viable solutions for dealing with high-cost enrollees, such as state-based programs using “State Innovation Waivers” under Section 1332 of the ACA, commercial reinsurance, broad-based funding, or a pool limited to known conditions and that includes monetary caps.

Methodology of the Proposed Reinsurance Pool within Risk Adjustment.

The present risk adjustment model predicts plans’ liability based on the age, sex and diagnoses (risk factors) for each enrollee.42018 Proposed NBPP, supra note 1 at 61467. CMS creates the risk factors by taking three years of large group claims data (not ideal, but the best information available) and builds models that predict the cost that might be attributable to a given condition or demographic factor. Enrollees’ risk scores are then totaled and folded into an enrollment-weighted average risk score for the plan—the plan liability risk score.5Id. Each insurer’s aggregate plan liability risk score is then compared to other plans’ scores to determine whether, and to what extent, an insurer pays a risk adjustment charge or receives a risk adjustment payment, with total transfers netting to zero within a market within a state. Risk adjustment transfers are not based on an insurer’s paid claims costs, only the insurer’s risk, leaving insurers with an incentive to ensure conditions are managed properly. Since the models use aggregate data to predict the average cost of a diagnosis, as opposed to an insurer’s actual claims costs, risk adjustment does not fully compensate for the cost of outlier enrollees with catastrophic claims.6Id.; Centers for Medicare & Medicaid Services, Center for Consumer Information and Insurance Oversight, March 31, 2016, HHS-Operated Risk Adjustment Methodology Meeting, Discussion Paper, 70-71 (March 24, 2016) (the “March 31, 2016 Discussion Paper”), available at https://www.cms.gov/CCIIO/Resources/Forms-Reports-and-Other-Resources/Downloads/RA-March-31-White-Paper-032416.pdf. For example, assume hemophilia has a median cost per patient of around $73,0007See Sheh-Li Chen, Economic Costs of Hemophilia and the Impact of Prophylactic Treatment on Patient Management, AJMC, (April 18, 2016), available at http://www.ajmc.com/journals/supplement/2016/incorporating-emerging-innovation-hemophilia-ab-tailoring-prophylaxis-management-strategies-managed-care-environment/incorporating-emerging-innovation-hem per year, but if there is an episode requiring hospitalization, the cost for a patient can easily explode into the millions. As a result, the average cost is around $155,000, and that can mean a substantial risk adjustment overpayment to an insurer who enrolls a hemophiliac who does not experience complications and a massive underpayment to the insurer who enrolls a hemophiliac that experiences complications.

As a solution, CMS proposes two high-cost risk pools across all states—one for the individual market and one for the small group market.82018 Proposed NBPP, supra note 1 at 61472. The pools would be used to make reinsurance payments to insurers worth 60 percent of the members’ paid claims that exceed $2 million (the insurer would still be liable for the other 40 percent).9Id. at 61472. The high-cost risk pools would be funded by an adjustment to each issuer’s risk adjustment transfer amount in each market, calculated as a percent of each issuer’s total premiums in the respective market. CMS proposes a uniform percentage of premium adjustment across all states for all markets and expects total adjustments to be less than one tenth of one percent of total premiums for either market. The proposed payment methodology is much like the premium for a reinsurance policy, except the “policyholders” (insurers participating in the program) will not know how much they have to pay until after the benefit year closes and the size of the high-cost pool becomes apparent. This retrospective cost setting allows CMS to maintain the balance of payments and charges within the risk adjustment program without needing to rely on outside funding, but makes it impossible for the participating insurer to reliably predict the program’s cost.10See id.

Vulnerabilities Associated With the Proposed High-Cost Reinsurance Pool.

Despite the well-intended benefits of the program, the imposition of a high-risk reinsurance pool on top of risk adjustment is subject to multiple drawbacks and vulnerabilities, including (i) the political or litigation risk stemming from potential questions about the statutory authority for such a program, (ii) the lack of predictable costs and benefits, (iii) a reliance on inter-state subsidization of high-cost enrollees and (iv) potential gaming by insurers and providers that could lead to increased costs and/or a less predictive risk adjustment model depending on the applicable high-cost threshold. Each of these potential challenges and vulnerabilities are discussed herein.

Issue No. 1: Political and Litigation Risk.

The statutory authority for CMS to implement a high-risk pooling mechanism may be subjected to legal or political challenges. The implementing statute for risk adjustment, ACA Section 1343, contemplates risk adjustment charges and payments to and from plans at the state level, not nationally.1142 U.S.C. § 18063; 2014 Final NBPP, supra note 2, at 15417. In addition, under Section 1343, risk adjustment charge and payment amounts are determined according to a prediction as to the “actuarial risk” (meaning, a prediction as to the relative health or sickness) of enrollees in each plan compared to the state average—not an assessment of plans’ actual claims experience.122014 Final NBPP, supra note 2, at 15417; 2018 Proposed NBPP, supra note 1, at 61467; 42 U.S.C.A. § 18063 (risk adjustment charges and payments are based on “actuarial risk”); 45 CFR §153.20 (defining “calculation of plan average actuarial risk” as the “specific procedures used to determine plan average actuarial risk from individual risk scores for a risk adjusted plan” and defining “individual risk score” to mean “a relative measure of predicted health care costs for a particular enrollee that is the result of a risk adjustment model”) (underline added). Indeed, CMS touts the proposal as one that will improve the “predictive accuracy” of the risk adjustment model.

To be sure, another section of the ACA, Section 1341, provides for the implementation of a separate Temporary Reinsurance Program based on actual claim costs.1342 U.S.C. § 18061. The Temporary Reinsurance Program provides a means to ameliorate the effects of catastrophic claims by providing reinsurance payments to plans that enroll members who experience claims above a certain threshold (an attachment point) up to a cap with a coinsurance rate that is subject to change each year of the three-year program.1445 CFR § 153.230(a)-(c). Importantly, there is no statutory authority for the reinsurance program to operate for the 2017 benefit year or beyond.1542 U.S.C. § 18061(a)-(b).

Plans that are dissatisfied with their risk adjustment obligations may take aim at the program on the basis that there is no authority for reinsurance within risk adjustment, particularly a permanent program that incorporates actual claims experience at the national level. For instance, CMS’s proposal may be subject to challenge under the Administrative Procedure Act,165 U.S.C. §702 (the “APA”). which provides a private right of action against the federal government where a federal agency has overstepped its authority under the governing statute. Such attacks on the ACA premium stabilization mechanisms are not new. The risk adjustment methodology has already been the subject of several lawsuits by insurers claiming that because the current risk adjustment model does not accurately measure “actuarial risk,” CMS has acted in a manner that is in violation of the APA because its actions are “arbitrary and capricious” and/or outside its statutory authority.17Evergreen Health Cooperative, Inc. v. U.S. Dept. of Health & Human Servs., No. 1:16-cv-02039-GLR (D. Md. filed June 13, 2016); Minuteman Health, Inc. v. U.S. Dept. of Health & Human Servs., No. 1:16-cv-11570-FDS (D. Mass. filed July 29, 2016); New Mexico Health Connections v. U.S. Dept. of Health & Human Servs., No. 1:16-cv-00878-JB-WPL (D.N.M. filed July 29, 2016). Political opponents to the ACA may advance similar arguments. Implementation of the Temporary Reinsurance Program has been the subject of congressional scrutiny, with ACA opponents claiming that CMS has acted beyond its authority and illegally transferred reinsurance payments to health insurers before paying sums allegedly due to the U.S. Treasury.18See Jason Dubner, Sandra Durkin and Ursula Taylor, Emerging Disputes Over Risk Sharing Under the ACA (April 18, 2016), available at http://www.butlerrubin.com/wp-content/uploads/Emerging-Disputes-Over-Risk-Sharing-Under-The-ACA.pdf . ACA opponents have gone so far as to introduce a bill in the Senate that would slash the budget of HHS in half unless HHS immediately deposits $4 billion into the U.S. Treasury and another $1 billion in March of 2017.19S.2803 - Taxpayers Before Insurers Act (Sen. Sasse, Ben (R-NE)), introduced 4/14/2016, available at https://www.congress.gov/bill/114th-congress/senate-bill/2803; Mary Ellen McIntire, Sasse Bill Would Slash HHS Budget Over Reinsurance Program, Morning Consult (April 15, 2016), available at https://morningconsult.com/alert/sasse-bill-slash-hhs-budget-reinsurance-program/.

Political and legal challenges to the proposed high-cost reinsurance pool premised on the lack of a clear statutory directive would not be inconsistent with the persistent challenges to ACA financial management programs, including risk adjustment, that have occurred within just the first few years of implementation.20For further background concerning the political and legal attacks against ACA financial management programs, see also Jason Dubner, Sandra Durkin and Ursula Taylor, ACA Risk Corridor Funding Falls Short, Litigation Ensues (June 9, 2016), available at http://www.butlerrubin.com/wp-content/uploads/ACA-Risk-Corridor-Funding-Falls-Short-Litigation-Ensues.pdf . Like the other financial management programs, any benefit that might come from the high-cost pool requires that when insurers set their rates (or choose which markets they will participate in at all), they trust the program will pay as expected when it is adjudicated. Perceived political and legal vulnerability may undermine this trust and negate the program’s potential benefit.

Issue No. 2: Lack of Predictability and Increased Exchange Volatility.

The charges associated with the proposed reinsurance pool are subject to variation depending on the size and incidence of claims exceeding the high-cost threshold. Although CMS expects the total adjustments to be a small percentage of total premiums, the actual cost of the proposal cannot be known in advance since CMS intends to maintain the balance of payments and charges within the risk adjustment program.212018 Proposed NBPP, supra note 1, at 61472. Thus, insurers must cross their fingers and guess as to how much they should accrue when setting their rates, which happens roughly two years before the cost of this high-cost pool is disclosed.

The inherent lack of predictability is exacerbated by potential gaming (discussed below), the proposed national scope of the pooling, and the volatility resulting from raising the attachment point to $2 million from the original proposal of $1 million in March 2016. Frankly, neither insurers nor CMS has enough information to properly price the cost of this program. And, as noted by Blue Shield of California, the difficulty in prospectively predicting the average premium load to bear for the nationwide high-dollar claims could cause carriers to over-predict, which would be counterproductive to ensuring member affordability.22Centers for Medicare & Medicaid Services, Center for Consumer Information and Insurance Oversight, HHS-Operated Risk Adjustment Methodology Discussion Paper Comments, 71 (July 2016) (the “July 2016 Discussion Paper Comments”), available via the Registration for Technical Assistance Portal (“RegTap”), https://www.regtap.info/. Presumably, CMS’s hope is that, by increasing the attachment point of the proposal, the incidence of claims exceeding the threshold would be so infrequent that the program cost would be minimal, even if it turns out to be far more expensive than predicted.

Anthem and the Blue Cross Blue Shield Association have proposed broad-based public funding to support the proposed reinsurance pool.23Id. at 35, 66-67. This would create predictability by allowing CMS to fix a per-plan charge in advance, and would address cross-regional subsidization issues, but securing public funding depends on the politics and priorities of Congress. In addition to the continued political pressure surrounding the allocation of payments under the Temporary Reinsurance Program, funding for the Temporary Risk Corridors program has been thwarted for at least the 2015 and 2016 fiscal years by political opposition.24See Emerging Disputes Over Risk Sharing Under the ACA, supra note 18; ACA Risk Corridor Funding Falls Short, Litigation Ensues, supra note 20. Thus, securing additional dollars for plans with high-cost enrollees as part of a reinsurance pool depends on the priorities of congressional leadership.

In sum, a self-funded reinsurance pooling mechanism funded completely by its participants is subject to a lack of predictability, and the premium load necessary to balance that lack of predictability may outweigh any premium benefit from the program itself.

In sum, a self-funded reinsurance pooling mechanism funded completely by its participants is subject to a lack of predictability, and the premium load necessary to balance that lack of predictability may outweigh any premium benefit from the program itself.

Issue No. 3: Cross-Regional Subsidization of High-Cost Enrollees.

Traditional Risk Adjustment transfers are made within a market within a state; however, CMS proposes to calculate payments and charges for the high-cost risk pool using national-level data. This will result in certain geographic areas subsidizing others based on regional differences that have little to do with actual disparities in the incidence or magnitude of high-cost enrollees. Whether a state might expect to be a net funder or recipient of high-cost risk pool funding depends on enrollment numbers and demographics in the individual market, the presence of existing state pooling or reinsurance programs and pricing and utilization of health care services within the state. While a condition’s rarity might be the same across the country, the cost of care to treat that disease, and whether it qualifies as a “high-cost” condition, depends heavily on the bargaining power of payers and providers and the available health care services. The national scope of the proposed reinsurance pool would cause low-cost regions to subsidize high-cost regions, creating “winner” and “loser” states.25See comments by Florida Blue and Kaiser Permanente, among others, July 2016 Discussion Paper Comments, supra note 22, at 100-101, 118-119.

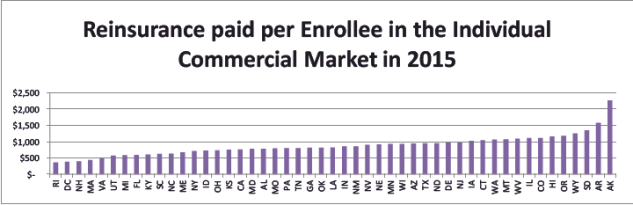

While the ACA has successfully attracted high-cost enrollees to individual marketplace coverage throughout the country, states have had very mixed results attracting healthy enrollees, and if some states have significantly worse ratios of sick to healthy enrollees, the states that have better ratios may end up paying for those who do not. The Temporary Reinsurance Program has had a far lower attachment point, but it is similar to the high-risk pool proposal in terms of pooling and payment methodology. Thus, looking at the reinsurance payments per individual market member for each state under the Temporary Reinsurance Program provides an indication as to the magnitude of the reinsurance transfers these states might expect under the proposed high-cost risk pool. Nationally, the average 2015 Temporary Reinsurance Program payment was $780 per individual market member. However, on a state-by-state basis, the average payment per enrollee varies significantly, as depicted in the following graph:26The reinsurance per enrollee is derived by taking the total reinsurance payments in the state (which is available in the Summary Report on Transitional Reinsurance Payments and Permanent Risk Adjustment Transfers for the 2015 Benefit Year, June 30, 2016 at https://www.cms.gov/CCIIO/Programs-and-Initiatives/Premium-Stabilization-Programs/Downloads/June-30-2016-RA-and-RI-Summary-Report-5CR-063016.pdf) and dividing by the total marketplace enrollees. On-Marketplace enrollment data can be found in the December 31, 2015 Effectuated Enrollment Snapshot (https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2016-Fact-sheets-items/2016-03-11.html). There is no good source of off-marketplace effectuated enrollment data, but the best estimate based on industry experts looking at state filings is that it is roughly 15 percent of on-Marketplace enrollment. Due to perceived inaccuracies, the CMS data for Minnesota was replaced with data from Healthinsurance.org (https://www.healthinsurance.org/minnesota-state-health-insurance-exchange/).

If the incidence of high-cost enrollees under the proposed reinsurance pooling mechanism is distributed similarly to the distribution for the Temporary Reinsurance Program—a reasonable assumption as the former will be a subset of the latter—then it is likely that the same high-cost states will consistently garner more reinsurance benefits under the proposal, raising the question of whether any stability from the proposed high-cost risk pool is the result of markets that have enrolled more healthy members paying for markets that have failed to enroll enough healthy members. The perception that certain states are unfairly subsidizing other states may incentivize increased political and legal challenges to the program or discourage state-level policies and programs that may create efficiencies, reduce costs and/or smooth risk.

Issue No. 4: Gaming.

CMS’s original proposal ($1 million attachment point and 90 percent coinsurance rate) would have created a substantial gaming incentive or “contracting risk,” attributable to the flexibility providers and payors have when they negotiate their contracts.27Several issuers and trade groups expressed concern about the possibility of contract gaming in response to the original proposal. See comments by America’s Health Insurance Plans, the Association for Community Affiliated Plans, Blue Cross / Blue Shield Association, Blue Shield of California and Cigna, among others. See July 2016 Discussion Paper Comments, supra note 22 at 23, 47-48, 66-67, 71, 88. Prices for health care services are not determined by traditional notions of supply and demand. Consumers have little transparency or sensitivity around medical pricing.28See Steven Brill, Bitter Pill: Why Medical Bills Are Killing Us, 7, 18-19, Time (Feb. 20, 2013), available at http://www.uta.edu/faculty/story/2311/Misc/2013,2,26,MedicalCostsDemandAndGreed.pdf . So, prices are determined through complex negotiations between health insurers and health care providers that allow for creative contracting. For example, under the original proposed $1 million threshold, payors might be incentivized to offer lower discounts for high cost services in exchange for steeper discounts on low-cost services. The hospital can expect to recover the same amount regardless of which services are allocated the deeper discounts, but the creative contracting will allow more costs to be shifted to the high-risk pool.29The temporary reinsurance program under ACA Section 1341 (42 U.S.C. Section 18061) is not as susceptible to contract gaming because the program addresses a more frequent type of risk. The temporary reinsurance program under Section 1341 provides reinsurance payments in connection with claims that fall within a narrower range, as defined by a low threshold and a cap that narrows each year of the three-year program, along with a reduction in the coinsurance rate. The “target” that narrows further each year, combined with the temporary nature of the program, makes it much more difficult to game through contracting than the present proposal that provides permanent reinsurance payments for high-cost enrollees that simply exceed a defined threshold. Since CMS intends to use the parameters of the high-cost pool in the recalibration of the risk adjustment model beginning with the 2019 benefit year, persistent “contract gaming” would be reflected by inflating the costs of high-cost conditions, eventually resulting in warped data and a less predictive model.30While CMS has said that they will reduce claims data used to create the risk adjustment models by truncating costs by the coinsurance amount over the threshold in their data set, contracting risk would incentivize providers by increasing the likelihood that a member may reach the attachment point as well as increasing the cost of the member who does so. 81 Fed. Reg. 172, at 61472, Sept. 6, 2016. The effects would worsen each year that the warped data is used for calibrating the risk adjustment model.

However, by doubling the attachment point and lowering the coinsurance rate, the high-cost claimants will not be numerous enough for insurers to reliably shift costs with predetermined contracts. But when a high-cost claim does appear, providers can still benefit by shifting costs into the high-cost pool through “provider gaming”—a more opportunistic event where a provider who sees a potentially high-cost patient realizes there might be little scrutiny if he or she inflates the cost of that patient, possibly in exchange for off-sets or reductions in charges for the more routine claims. This is not dissimilar to the practice of “Hollywood accounting” in the film and television industry.31“Hollywood accounting” is the practice of using opaque or creative accounting methods to budget and record profits and costs for a film project, causing largely successful movies to appear unprofitable. See Derek Thompson, How Hollywood Accounting Can Make a $450 Million Movie ‘Unprofitable,’ The Atlantic (Sept. 14, 2011), available at http://www.theatlantic.com/business/archive/2011/09/how-hollywood-accounting-can-make-a-450-million-movie-unprofitable/245134/ . Issuer-owned hospitals or insurers that have risk-sharing arrangements with providers are best situated to engage in such “provider gaming.” Where health care payors and providers have an opportunity to realize the reinsurance benefits to help subsidize expensive claims there may be even less incentive to seek to achieve cost efficiencies. Reducing the coinsurance rate from 80 percent to 60 percent may reduce the relative value of this gaming opportunity, but it does not close it off entirely. In sum, regardless of the attachment point or coinsurance rate, a reinsurance pooling mechanism can be gamed because the prices paid to hospitals and doctors by health care payors are limited only by the bounds of human creativity in negotiating contracts and/or billing across services, patients and/or physicians.

Other Potential Solutions or Adjustments: Some Better than Others And None Are Perfect.

In response to comments, many of which focused on the above-described concerns, CMS has suggested some changes since its original proposal, namely decreasing the incidence of qualifying high-cost claims and increasing their impact on providers. It is not clear how much of a benefit this scaled-back program might provide and whether the benefit would even outweigh the program’s administrative costs.

32As noted by CMS, the predictive power of the risk adjustment model improves the lower the high-cost threshold and the higher the coinsurance rate. March 31, 2016 Discussion Paper, supra note 6, at 71. There may be preferable alternatives that can create a program large enough to deal with high-cost, outlier claims without stretching statutory authority. First, states may address the problems for themselves through Section 1332 waivers and may qualify for government funding to the extent the state-based program reduces the premium or cost-sharing subsidies required to be paid under other sections of the ACA.33A “State Innovation Waiver” under Section 1332 allows states to implement innovative ways to provide health care that is at least as comprehensive and affordable as would be provided without the waiver, provides coverage to a comparable number of residents and does not increase the federal deficit. See

42 U.S. Code §18052. See

also information at cms.gov, the Center for Consumer Information and Insurance Oversight, available at https://www.cms.gov/CCIIO/Programs-and-Initiatives/State-Innovation-Waivers/Section_1332_state_Innovation_Waivers-.html. Although the waivers are not available until January 1, 2017, Alaska has already passed legislation providing for a two-year high-cost reinsurance pool funded through an existing broad-based 2.7 percent premium tax on all Alaskan insurers, not just health insurers, which may lead to a Section 1332 waiver.34For details concerning the Alaska legislation see https://www.billtrack50.com/BillDetail/733156/2838. See also Louise Norris, Alaska Health Insurance Exchange / Marketplace 2017: Moda Exiting Market, Premera Increasing Rates 7.3%, Healthinsurance.org (October 11, 2016), available at https://www.healthinsurance.org/alaska-state-health-insurance-exchange/. Should this reduce premiums, the waiver could allow Alaska to recoup the benefit that the premium has on the cost of federal marketplace premium subsidies. State-based solutions, such as the Alaska legislation, allow states to tailor programs to the unique regional issues affecting their markets and constrain the costs of the program to the individuals and entities who most directly benefit from the subsidization. State-based solutions would also quell concerns about cross-regional subsidization.

State-based solutions allow states to tailor programs to the unique regional issues affecting their markets and constrain the costs of the program to the individuals and entities who most directly benefit from the subsidization.

In addition, insurers may be able to use commercially available reinsurance arrangements to mitigate risk associated with high-cost acute (as opposed to known or chronic) conditions because such conditions are random, unexpected, and, therefore, more susceptible to such risk management solutions. With commercial reinsurance, the amount of coverage and the price can be tailored to each plan and market, and commercial reinsurance offers guaranteed terms, whereas the cost/benefit of an annual budget-neutral reinsurance program must be adjusted depending on the claims, making it inherently unreliable. Unexpected high-cost acute conditions are also not susceptible to risk selection and arguably are not an “actuarial risk” that risk adjustment is intended to address.

In devising a properly funded high-cost pool program, it might also help to use a model that includes both diagnosis and monetary limits to reduce the potential for gaming and constrain the program to conditions that are actually susceptible to risk selection. Thus, for the included conditions, monetary limits could cap the payments depending on the conditions, i.e. a cap of $1 million for treatments associated with a high-risk pregnancy or $2 million for hemophilia. The caps could be calculated by periodically identifying the cost of the top one percent of members with that diagnosis. The complexity would make it difficult to game, as providers would need to be careful to avoid exceeding the various limits, and it would incentivize insurers to continue to police provider practices. Such diagnosis and monetary limits may engender controversy as to the included conditions and applicable caps, but by focusing on the chronic conditions with high potential costs and high volatility, only a small number of conditions or combinations of conditions may qualify. In addition, the exclusion of high-cost acute conditions would allow plans to innovate and differentiate around managing risk for high-cost claimants.35See comments by Care Source in the July 2016 Discussion Paper Comments, supra note 22, at 75. However, monetary and diagnosis limits—by themselves—do not solve the above-described challenges associated with the lack of predictability, cross-regional subsidization, or litigation and political risk presented by CMS’s proposal.

Conclusion: Less is More, at Least for Now.

Comments on the proposal for a high-cost reinsurance pooling mechanism are being reviewed by CMS and many of the details are yet to be determined, but regardless of the final rule, a high-risk pooling mechanism in conjunction with risk adjustment will engender a number of challenges, including the lack of predictability in terms of the cost of the program and its impact on premiums. In addition, complaints concerning cross-regional subsidization may incentivize litigation or political attacks, while questions as to statutory authority may strengthen such arguments and create further vulnerabilities in the risk adjustment system. Focusing on other improvements to the risk adjustment program that have been proposed by CMS, such as the policies to address partial year enrollment and the incorporation of prescription drug data into the model, would do more to further stabilize and improve the core of the program. And, although there may be more palatable solutions to dealing with high-cost outlier claims, these suggestions are not without their pitfalls or shortcomings. In sum, additional state or federal legislation may be needed to address the issues presented by high-cost claims by either creating a high-cost pool with broad based funding or finding ways to attract more low-risk enrollees to the Marketplace.

The information contained herein is for general informational purposes only. The views are personal to the authors and the information provided is not legal advice and is not intended to be acted upon as such.