In recent years, the amount of renewable energy, such as wind and solar, that makes up U.S. energy supply has increased exponentially. This surge has been achieved thanks to state (and to some extent federal) requirements and incentives, as well as growth in consumer demand. With this increase, which is particularly concentrated in areas with the most generous incentives and areas available for development, come valuable benefits including reduced greenhouse gas and other emissions and increased energy independence for the country.

At the same time, however, this proliferation of renewable energy poses certain challenges to the reliability of our electric grid. In particular, given their intermittent production, solar and wind resources are unable to respond to fluctuations in energy demand that occur each day. As people return home and turn on their electronics during the early evening, sunlight declines and the production of solar energy is unable to meet the uptick in demand. Meanwhile, conventional generating resources may be unable to ramp up in sufficient time to meet evening demand. This phenomenon has become known as the “duck curve.”

In order to maintain reliability in the face of this phenomenon, grid operators may be forced to curtail renewable energy generation, or even limit further interconnection of renewable generation to the grid. But the operational challenges presented by the duck curve can also be mitigated through a diverse portfolio of supply- and demand-side options, including both flexible conventional generation and distributed energy resources (DER), without losing the benefits of increasing renewable energy supply.

The Proliferation of Renewable Energy

Renewable energy has experienced substantial growth in the U.S. in nearly all 50 states. Through the first half of 2016, renewables provided 16.9 percent of electricity generation, compared with 13.7 percent in 2015. While several segments of the renewable energy industry are growing—including hydro-electric power, biomass, geothermal, wind and solar or photovoltaic (PV)—electric grid interconnection applications throughout the country are now primarily for wind and solar projects. The U.S. Energy Information Administration (EIA) reports a 418 percent growth in solar energy capacity alone from 2010-2014, from 2,326 MW to 12,057 MW.

Renewable energy growth shows no signs of slowing, and renewables are poised to expand substantially their share of the nation’s future supply mix. One of the states leading the way is California, which has mandated that one-third of its power must be supplied by non-hydro renewable energy sources by the end of 2020. This will require approximately 20,000 MWs of capacity from new variable energy resources. Already, nearly 30 percent of the state’s generation came from non-hydro renewable energy as of summer 2016. Under one policy initiative, by 2030, 50 percent of retail electricity in California may come from renewable power. Currently, 29 states, Washington, D.C., and three territories have renewable energy requirements. An additional eight states and one territory have voluntary renewable energy targets. In addition, large commercial customers, such as Amazon, Google, Apple and Dow Chemical, to name a few, have been entering into renewable energy power purchase agreements with renewable project developers, further supporting the development of renewable generating facilities. Given this momentum, the growth in renewable energy driven by requirements and incentives at the state level and customer demand is unlikely to be affected by policy changes at the federal level.

Rapid Growth of Renewable Resources Presents Challenges

While increased renewable generation can benefit consumers, the environment and U.S. energy independence, the variable nature of renewable resources presents challenges to grid operators.

In California, the influx of solar generation has exceeded demand, resulting in a load imbalance. This phenomenon was predicted by the California system operator (CAISO) in 2013 and made its appearance in the CAISO load data this spring. In order to keep the lights on, grid operators must balance supply and demand in real time. On a periodic basis, the grid operator forecasts the “load” or consumer demand for power and procures a sufficient amount of supply to meet that demand through its day-ahead and real-time energy markets. To ensure adequate energy supply meets growing demand, grid operators also procure energy “capacity,” or a commitment from energy suppliers to bring new resources online by a date typically a few years into the future. In some regions such as California, the state’s aggressive renewable portfolio standard has resulted in an influx of renewable energy and capacity that, given its unique attributes, has outpaced the grid’s ability to safely and reliably absorb the electricity generated from solar power.

Unlike conventional energy resources, solar energy produces the most energy during peak daylight hours. Thus, solar energy is a variable resource that is available only during limited hours of the day. Because it is not continuously available, solar power, as well as other renewable resources such as wind generation, is an “intermittent” energy resource that cannot provide electrical output on demand at any given time. This is in contrast with conventional energy resources, such as generating plants powered by natural gas, nuclear power or fossil fuel. Because they are available for dispatch 24 hours a day, seven days a week, some of these resources are utilized as “baseload generation” providing constant output. In typical markets where solar power constitutes a small fraction of the overall energy mix, peak energy demand occurs during a few hours mid-day. In a market experiencing a high output of solar power, however, the period of peak demand is shifted to a few hours in the evening, requiring grid operators to dispatch conventional energy resources to meet peak evening demand that is unmet by daytime peaking solar energy.

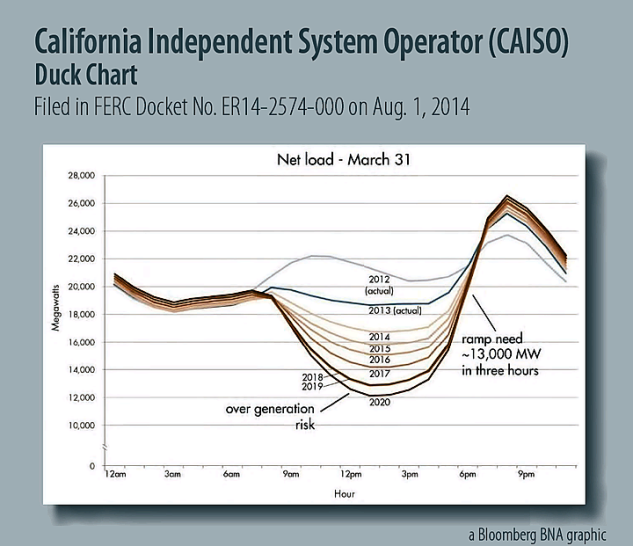

While conventional energy resources, such as generating plants, are available to meet demand during evening hours, unlike renewable or “intermittent” resources, some conventional resources require greater lead time to start, ramp up, and achieve the level of production needed to meet demand. Thus, to meet evening demand, conventional generation must begin running during peak daylight hours when solar power is producing at full tilt, resulting in “over generation” of power during those hours (i.e., more electricity is supplied than is needed to satisfy real-time electricity requirements). In addition, conventional resources are needed in order to support upcoming ramps up or ramps down in power (i.e., the grid operator must quickly dispatch or shut down generation resources to meet increasing or decreasing electricity demand, often over a short period of time). Grid operators depend on conventional generators that require a longer start time to come online to meet these ramps. Finally, generating plants are needed for local voltage support and reliability issues for a certain minimum amount of time, which can also contribute to over generation. As a result, as explained by the CAISO, generators that require a longer start time to come online “must produce at some minimum power output levels in times when the electricity is not needed.” This “over generation” problem is depicted by the “duck curve.”

The duck curve plots “net load” requirements or the total electric demand in the system minus wind and solar generation. This value represents the demand that the CAISO must meet with other, dispatchable resources such as conventional natural gas generating plants or hydropower. The duck curve depicts a significant drop in mid-day net load during the spring season when significant amounts of solar power are added to the system to meet peak demand (i.e., the belly of the duck). Because net load requirements are significantly greater in the evening, after renewable resources come offline, steep ramps are required to meet this peak evening demand (i.e., the duck’s neck). If the conventional power system is unable to accommodate the ramp rate and range needed to fully utilize solar energy, the resulting “over generation” will stress the grid and threaten grid stability.

If unaddressed, over generation may require curtailing renewable energy, which occurs when a system operator decreases the output from a generating resource (such as wind or a solar power plant) below its normal production. Such curtailment undercuts renewable energy’s environmental benefits, such as its low greenhouse gas and other emissions. One report by the National Renewable Energy Laboratory finds that without taking measures to enable greater grid flexibility, solar penetrations as low as 20 percent of annual energy could lead to marginal curtailment rates that exceed 30 percent. However, if greater system flexibility and resource diversity are achieved, solar power curtailment in California can be minimized or avoided, allowing much greater penetration of variable generation resources in achieving the state’s renewable portfolio standard.

Diversity of Supply can `Tame the Duck’

While solar energy curtailment is one solution to the over-generation problem, it should be viewed as a measure of last resort. Rather than reverse the great strides that have been achieved in increasing renewable energy supply, grid operators and policy makers ought to adopt a holistic approach that supports tighter integration of solar power with a diverse portfolio of supply- and demand-side options. Commenting on the challenges of integrating renewables, Federal Energy Regulatory Commission (FERC) Commissioner Cheryl A. LaFleur recently told Bloomberg that “variable renewable generation can be an important part of a reliable grid but it does require other resources to balance [that supply].”

Solutions that include both flexible conventional generation and distributed energy resources (DER), such as demand response and energy storage, can balance supply and mitigate the negative impacts of the duck curve, reduce the need to curtail renewable energy, and preserve the valuable environmental gains achieved with a clean energy mix.

Dispatch Demand Response During Steep Ramping Periods

Demand response programs provide consumers financial incentives to voluntarily reduce or “curtail” their electricity usage during peak periods (i.e., peak shaving), during grid emergencies, or when needed to alleviate local transmission distribution system constraints. Residential, commercial and industrial customers who participate in such programs are commonly referred to as “demand response resources.” Because demand response is controlled by end users of energy, it can be deployed quickly. Consumers are notified that the grid operator or utility has called a demand response event and respond to dispatch instructions in as little as 30 minutes. Because demand response resources reduce the amount of energy pulled from the grid and can postpone the need for building additional peaking resources (i.e., conventional generation), they are environmentally friendly and provide savings to consumers. When aggregated, the contribution of multiple demand response resources is substantial, allowing grid operators to rely on demand response alongside conventional energy resources.

With its low cost, reliability and operational flexibility, demand response is poised to play a key role in responding to the over-generation issue that, if unaddressed, will require renewable energy curtailment. Under many programs, demand response resources are required to be available for dispatch during weekdays year-round, as early as 6 a.m. and until as late as 10 p.m. Resources in some markets could be called for as long as 10 hours per event, and for an unlimited number of calls per year. These availability requirements capture the critical late afternoon net load ramping period from 4 p.m. to 7 p.m., when resources are needed quickly to meet increasing electricity demand, while solar energy output declines into the evening.

The CAISO has recognized demand response in a category of resources meeting the grid operator’s standard for “super-peak ramping flexibility.” This category “addresses each month’s most extreme ramping needs.” As described by the CAISO, such resources must be able to provide at least three hours of energy at their effective flexible capacity value, respond to five dispatches per month, and have daily availability on weekdays that are not holidays. While demand response flexibility is utilized in this category chiefly to respond to net load ramping needs, demand response can also address other challenges to solar variability.

For example, demand response programs supporting advanced technologies such as advanced metering infrastructure (AMI) and direct load control or auto-DR can provide real-time visibility and control over consumer energy use. Such technology allows third-party aggregators to manage and curtail load automatically. This operational flexibility can address multiple challenges of solar variability. A recent analysis published by the Community Solar Value Project suggests that within a 30-minute to two-hour time frame, these technologies can enable demand response to address un-forecasted steep ramps that occur anytime throughout the day because of cloud cover.

Increased Viability of Energy Storage Options

In recent years, battery storage has emerged as a viable option for addressing this issue as well. Long viewed as the holy grail of the energy industry, energy storage, both stand-alone and combined with demand response or renewable resources, can be used to even out the variability of intermittent resources by storing excess electricity during times of high production and releasing that electricity onto the grid during times of lower generation. Energy storage technologies such as pumped hydroelectric, thermal storage and flywheels have been around for many years, but challenges of cost, location restrictions and efficiency have prevented their large scale use on the grid. Battery storage cost decreases in the past few years, combined with increased storage market opportunities and incentives, have fueled aggressive growth in this area, with projections of further increases in installations in the coming years.

As noted above, energy storage combined with a generating facility provides obvious benefits, as it can be used to store electricity generated by the solar or wind facility during peak generating periods that may not coincide with peak usage periods. The stored energy is then discharged during periods of peak usage, or when the sun is down or the wind is not blowing. This type of system works well for larger utility scale projects. Customers with smaller, “behind-the-meter” on-site projects that are net metered presently have little incentive to store excess electricity on-site, as net metering programs effectively allow them to “store” their electricity on the grid. However, in order to address reliability issues caused by large numbers of smaller solar installations, stand-alone batteries can be used on-site by customers and also can be integrated into the distribution system. With their ability to be dispatched quickly, battery storage can serve a role similar to that of demand response of responding to sudden shifts in net load, benefiting the grid as well as individual customers.

Driven by lowering costs and increased incentive programs and market opportunities, we have already seen a significant increase in the U.S. battery storage market. As reported by the Energy Storage Association, the battery storage market saw an increase of 243 percent in 2015, with an increase of 405 percent in the behind-the-meter market. These installations can participate in the wholesale market, providing services to the grid, and can also be dispatched during periods of peak usage, “smoothing” a customer’s load and thereby reducing certain utility charges that are based on peak usage. Similarly, batteries controlled directly or indirectly by the grid operator could be dispatched strategically to help alleviate duck curve challenges.

Removing Regulatory Barriers

In order to capitalize on the promise of demand response and energy storage to address the challenges associated with integrating increased renewables into our energy supply, regulatory policy will need to recognize and appropriately incentivize investment in these areas. FERC has been working on removing barriers to entry of both demand response and energy storage into the markets. While these efforts are encouraging, there is further work to be done.

In the area of demand response, FERC’s Order 745, originally issued in 2011, was designed to place demand response on a level playing field with other resources for purposes of participation in the wholesale markets. After facing challenges in federal court and initially being vacated by the U.S. Court of Appeals for the District of Columbia Circuit, the order was ultimately upheld by the Supreme Court, ostensibly clearing the way for greater demand response market participation.

While demand response has gained momentum with implementation of Order 745, federal policy alone is insufficient to see demand response achieve its full potential. Increasingly, however, states are recognizing the value that demand response provides to consumers and to the local distribution system. Several states have adopted demand response programs that efficiently function alongside the wholesale markets and that require performance parameters often overlapping the critical ramping periods presented with the duck curve. Thus, as more regions face reliability issues resulting from increases in renewable resources, demand response programs that are tailored more closely to address these issues could play a meaningful role in supporting both renewable energy growth and electric grid reliability.

In the area of energy storage, FERC orders such as Order 755 issued in 2011 and Order 784 issued in 2013, which require acknowledgement of the ramp-up benefits of energy storage in wholesale market compensation, have provided great market opportunities for battery storage. In fact, much of the battery storage increase in 2015 was driven by the PJM frequency regulation market, which compensates resources such as battery storage that are able to respond quickly to dispatch signals to maintain the frequency of the grid. At the same time, regulatory treatment of storage has lagged behind the technology, something FERC is working to rectify. In November 2016, FERC issued a Notice of Proposed Rulemaking (NOPR) that would require grid operators under FERC’s jurisdiction to establish market rules that accommodate storage resources’ participation in the markets based on their physical and operational characteristics. The NOPR seeks to address the problem with many existing grid operator tariffs that “were originally developed in an era when traditional generation resources were the only resources participating” in the markets. This development is a promising one for the market and could serve to further expand the ability of battery storage technologies to be used to accommodate the growing demand for renewable resources without jeopardizing reliability.

Looking Ahead

As renewable generating resources continue to make up an increasing part of energy supply, grid operators will continue to face reliability challenges. Those challenges, however, should not limit renewable energy development. Rather, regulatory policies should capitalize on the unique attributes that demand response and energy storage contribute to alleviating the challenges to renewable energy integration. If policies and programs encourage greater innovation, remove barriers to entry, and create incentives for financial investment, renewable generation can continue to grow without threatening reliability.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.