The spinoff—a transaction whereby a company splits off sections of itself as a separate business—has been at the forefront of corporate strategy in the last few years as companies search for ways to return value to shareholders in the face of challenging market conditions. With recent credit market volatility and companies struggling to create value through increased revenue and earnings, these crucial, but sometimes-forgotten transactions have been resurrected in recent years. The New York Times, citing Dealogic, reported that in 2012, there were 85 spinoffs worldwide worth $109 billion and, in 2011, 93 spinoffs worth $128 billion.

Spinoffs fundamentally change existing corporate structure by transferring an operating division or department, and any liabilities associated therewith, to a new company that exists outside the corporate umbrella. The new company—the successor entity to current and future collective bargaining obligations—may have substantial debt with no earnings history. That’s right—the single-employer defined benefit pension plan may about to be transferred from an established corporation with wherewithal to a new company that may not have any meaningful ability to fund the plan.

Further, as described more fully below, a spinoff is sometimes followed by a joint venture transaction which adds an additional layer of separation and more discomfort concerning pension funding. To address this vulnerability, the union should exercise its rights either under a successorship clause or effects bargaining to secure a Memorandum of Agreement addressing, among other things, pension funding.

Case Study in Business Separation:

Spinoff and Joint Venture Transactions

1. Pre-Transactional Corporate Structure.

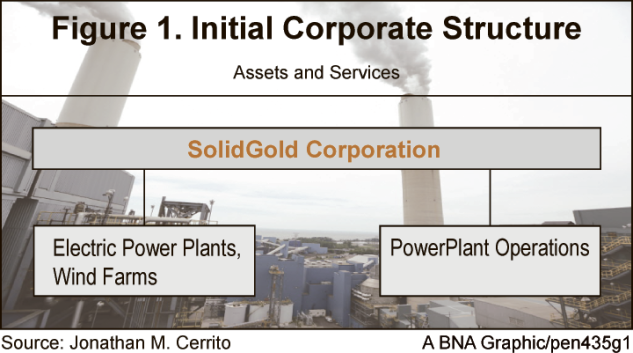

SolidGold Corporation, an energy company that is publicly-traded, owns and operates power plants. Given the recent trend in green technology, SolidGold has delved into wind farms and has developed a portfolio of wind farms that it owns and operates. SolidGold is the plan sponsor of a defined benefit pension plan (“Retirement Plan”) that is maintained under the Employee Retirement Income Security Act of 1974, as amended (“ERISA”). In addition to SolidGold, any corporation 80 percent or more of whose stock (based on voting power or value) is owned directly or indirectly by SolidGold may adopt the Retirement Plan. SolidGold and PowerPlant Operations, Inc.—a wholly owned subsidiary of SolidGold and the licensed operator of the power plants and wind farms—entered into a collective bargaining agreement (“CBA”) with the union covering all workers at the power stations and wind farms. Pursuant to the CBA, PowerPlant Operations shall have in effect a defined benefit pension plan to provide pension benefits to bargaining unit members. To satisfy this obligation, PowerPlant has adopted the Retirement Plan. Figure 1 provides an illustration of SolidGold’s corporate structure.

2. Business Separation (Spinoff and Joint Venture) Transaction.

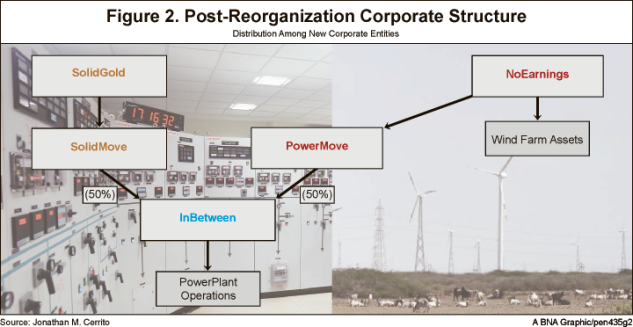

The Board of Directors of SolidGold approved a plan to pursue a spin-off of the wind farms into a newly formed entity called NoEarnings, Inc. (“NoEarnings”). NoEarnings will be a separate and independent company and will have an independent Board of Directors (i.e., a board consisting of directors that are different than the Board of Directors for SolidGold).

After the spin-off, SolidGold and NoEarnings will enter into a joint venture whereby a newly formed entity called InBetween, Inc. (“InBetween”) will be created. SolidGold and NoEarnings will each indirectly own 50% of InBetween. InBetween, in turn, will purchase PowerPlant Operations.

To technically implement the joint venture of InBetween, SolidGold will create a new company called SolidMove, Inc. (“SolidMove”) and PowerPlant will create a new company called PowerMove, Inc. (“PowerMove”). SolidMove and PowerMove will then create, and co-own, In Between.

The post-separation structure is summarized in Figure 2.

As part of the proposed transaction No Earnings will incur substantial indebtedness of approximately $4.5 billion, and the proceeds will be transferred to SolidGold in consideration for the transfer of the wind farms. Debt to capital ratio of No Earnings will be 116.4%. This ratio represents the amount of the debt the company carries after subtracting the company’s cash (here, 120.4% (debt) minus 4.0% (cash)). To put this in perspective, Solid Gold in 2013 had a debt to capital ratio of 39.4%. Thus, No Earnings will have a significantly higher amount of debt than SolidGold historically maintained.

In Between will succeed Power Plant and assume the terms and conditions of existing collective bargaining agreements. In addition, In Between will assume the relevant pension assets and liabilities of both active and inactive participants connected to the wind farms.

3. Analysis.

a. Legal Framework.

ERISA, and the Internal Revenue Code (“Code”) do not, per se, prohibit corporate reorganizations. These bodies of law do, however, impose a set of guidelines that generally must be complied with.

Division of Assets and Liabilities. Generally, assets of a defined benefit plan must be divided in accordance with the requirements of ERISA and the Code.

Evasion Transactions. If the principal purpose of any transaction is to evade pension liability and the transaction takes place within 5 years before termination of a pension plan, any entity involved in the transaction (and that entity’s controlled group on the termination date) can be held liable as if that entity was a contributing sponsor of the terminated plan.

Termination Liability. If a pension plan terminates, any employer (or member of the employer’s control group), with certain limitations, may be liable for any funding deficits.

In PBGC Opinion Letter 85-8, a corporation entering into a similar spin-off transaction, as here, inquired as to whether the former parent would be held liable if the new entity terminated the pension plan. There, Corporation X [here, SolidGold] decided to spin-off its manufacturing subsidiaries, so that the manufacturing subsidiaries were no longer part of the controlled group. This was done by creating New Corp [here, NoEarnings] which acted as a holding company of the manufacturing subsidiaries. Like here, New Corp would be a stand alone entity that would be publicly traded. The employees of the spun-off manufacturing subsidiaries that participated in the MS Pension Plan, a pension plan sponsored by the manufacturing subsidiaries, were transferred to the New Corp Pension Plan, a plan newly established by New Corp, which assumed the accrued liability of the MS Pension Plan. As of the spin-off date, MS Pension Plan transferred assets to the New Corp Pension Plan so that each New Corp Pension Plan received assets in proportion to its accrued liabilities.

Corporation X sought an opinion from the PBGC as to whether it would be responsible for any deficits that occur if New Corp decided to terminate the New Corp Pension Plan with insufficient assets to pay benefits.

Discrimination. It is unlawful for any person to discriminate against a participant for either exercising a right under the provision of a pension plan or for the purpose of interfering with the attainment of any right to which such participant may become entitled under the pension plan.

For purposes of this article, we assume that the separation satisfies the foregoing requirements on the basis that sufficient assets are transferred; benefits immediately before and after the separation will not be different; and no evidence exists that the transaction discriminates or that its principal purpose (ignoring the massive leap in the debt to capital ratio) is to evade or avoid pension liability.

b. Pension Funding Ramifications: Loss of Financial Security in the Controlled Group.

Although ERISA and the Code may not prohibit the proposed spin-off, the transaction has very real ramifications on SolidGold’s collective bargaining obligations, particularly pension funding. This is because the minimum funding requirements for pension plans impose funding liability not only on the plan’s contributing sponsor but each member of its controlled group.

Pre-spinoff, SolidGold is primarily liable, on a joint and several basis, for the funding of the Retirement Plan. In addition, any entity in a parent-subsidiary or brother-sister relationship with SolidGold is also equally liable for pension funding.

Post-separation both of the above will no longer be true. SolidGold will not be a member of a controlled group with NoEarnings and therefore will no longer have primary liability for pension funding. Furthermore, the historical and future earnings of SolidGold will no longer be available to either provide capital or pay liabilities that NoEarnings incurs in the operations of the wind farm assets. Instead, there will be agreements between SolidGold, InBetween and SolidGold’s other businesses that will, in finality, divide assets, liabilities and obligations (including employee benefits and other liabilities) relating to the wind farm assets attributable to periods prior to, at and after the separation.

In addition, the assets of NoEarnings may be removed from the liability of pension funding because the plan sponsor of Retirement Plan will be InBetween, a separate and distinct joint venture (and not NoEarnings), and there will be an intermediate holding company. This is because NoEarnings will own only 50% of InBetween and therefore, since the 80% ownership test is not satisfied, these entities are not members of a controlled group.

4. Tackling the Spinmeister.

It remains to be seen whether in 2014, with the Dow Jones Industrial Average having crossed the 17,000 point threshold and the tentative reopening of debt markets, whether corporate strategy will now shift from spinoffs to sales and buy outs. In any event, when economic environments contract, unions should be aware that just because a third party buyer may not be present in a transaction does not mean the union does not have an interest to protect.

From the union’s perspective, regardless of whether a corporate reorganization transaction technically complies with the law, the security and predictability that existed pre-transaction should continue to exist post-transaction in order to meaningfully preserve collective bargaining obligations, including pension funding.

As such, when confronting spinoff transactions, unions should seek a Memorandum of Agreement (“MOA”) addressing current and future collective bargaining obligations to ensure that, among other things, the successor shall:

- continue to have in effect a defined benefit pension plan to provide pension benefits to bargaining unit members;

- remain jointly and severally liable for pension funding; and

- in the event that the successor or any of its subsidiaries transfers an equity interest in the spun-off assets or transfers to a third party all or substantially all of the spun-off assets, require as a condition of the transaction that such third party assume all of the rights and obligations imposed on the successor or any of its subsidiaries by the MOA and CBA.

In assessing the structure of any corporate reorganization, evaluating assumptions used in allocating liabilities and assets of pension plans, and negotiating related MOAs, unions and their labor counsel will want to assemble a team of professional advisors that includes ERISA counsel.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.