Roth 401(k) can be a powerful option for your employees to save for retirement, but not for the reasons that are most often cited. This article explains why your 401(k) plan should have a Roth option, and why some of your employees should use it. The same considerations generally apply to Roth IRAs.

When you contribute to a Roth 401(k), you receive no exemption from taxation on that contribution. Unlike a pre-tax 401(k) contribution, your federal income tax does not go down. However, if you withdraw the Roth money after 5 years of participation and age 59-½, you pay no tax on the amount withdrawn, not even on the investment earnings. In contrast, a pre-tax 401(k) contribution will reduce your taxes at the time of contribution, but the entire amount (including investment earnings) is taxable upon withdrawal.

As explained in more detail below, there are four main reasons to make Roth 401(k) contributions instead of the more conventional pre-tax 401(k) contributions:

- High income workers can save more for retirement in Roth 401(k) than in pre-tax 401(k).

- Low wage workers can save more effectively in Roth 401(k).

- You can manage your income taxes more effectively if you have a portion of your savings in Roth 401(k).

- You can leave more money to your heirs if you have savings in a Roth 401(k).

Before examining each of these points in detail, it is worthwhile to understand two key points. First, that savings should be measured in stuff, not dollars. Second, the error in the claim that is most often made about Roth IRAs and Roth 401(k): that you should use Roth if you think tax rates are going to go up.

Measure Your Savings in Stuff

Jane is in the 35% tax bracket and has plenty of savings and income that will continue well into her retirement. We are assuming she will be in the 35% bracket when she retires. Having plenty of money for her own needs, she is now saving even more so that she can visit her grandchildren frequently once she is retired. When you add up airfare, hotel, rental car, and the obligatory presents for the little brats, each visit will cost $2,500. Jane has been putting $20,000 a year into her pre-tax 401(k) account for the last 4 years, and has managed to earn a 25% return (or $20,000) on that $80,000 of contributions. So, Jane now has $100,000 in her 401(k) account. Best of all, each annual $20,000 contribution really only cost her $13,000 because, at the 35% tax rate, she saved $7,000 in taxes when she put $20,000 into her account.

Meanwhile, Jane’s twin brother Jim (whose income and financial position is otherwise exactly the same as Jane’s) was only willing to set aside $13,000 per year out of his paycheck. Over the last 4 years, his savings added up to $52,000. He invested in the same funds as Jane and earned a 25% return, just like Jane. But his 25% was only $13,000. His account stands at $65,000. Jim, however, deposited his contributions into a Roth 401(k) account.

Who has more saved—Jane with $100,000 or Jim with $65,000? The answer is, they both saved the exact same amount and they both have the same amount, measured in stuff. In order to spend her $100,000 on visits to her grandchildren, Jane will have to withdraw it from her 401(k) account, paying federal income taxes of 35%. That will leave her with $65,000 to spend, which purchases 26 visits at $2,500 each.

Jim will pay no tax when he withdraws $65,000 from his Roth 401(k) account and will be able to purchase 26 visits to his grandnieces at $2,500 each.

In order to save $20,000 each year, Jane had to reduce her spending by only $13,000, because she saved $7,000 in taxes each year. However, Jim reduced his spending by the same amount—$13,000—each year in order to make his Roth 401(k) contributions.

In short, measured in stuff, Jane and Jim saved (deferred their current consumption) by exactly the same amount, $13,000 each per year, and each one has 26 future visits saved up. Measured this way, one might conclude that saving in a pre-tax 401(k) and a Roth 401(k) are the same. However, as we shall see, there are important differences and some employees should use pre-tax 401(k), while others should use Roth 401(k) or both Roth and pre-tax 401(k).

Are Your Tax Rates Going Up or Down?

If you know that your marginal tax rate in the future, when you retire, will be higher than it is now, then Roth 401(k) is clearly better than regular 401(k). With regular 401(k), you pay the tax when you withdraw your money, presumably in retirement. If your tax rate will be higher at that time, you have an advantage in paying tax on the income now.

If you know that your tax rate will be lower in the future, then the decision is a bit more complicated. It would seem to make sense to use regular 401(k) so that your income will be taxed at a lower rate. However, as we shall see with Jane and Jim, Roth 401(k) allows you to save more for retirement (measured in stuff) and this fact may outweigh small differences in the tax rate.

The problem with this analysis is that knowledge about the future is not so easy.

Many people are quite convinced that their tax rate in retirement will be higher than it is now. Others are equally certain their tax rate in retirement will be lower than it is now. While these individuals are not necessarily incorrect about the direction of their future tax rates, their certainty is an illusion.

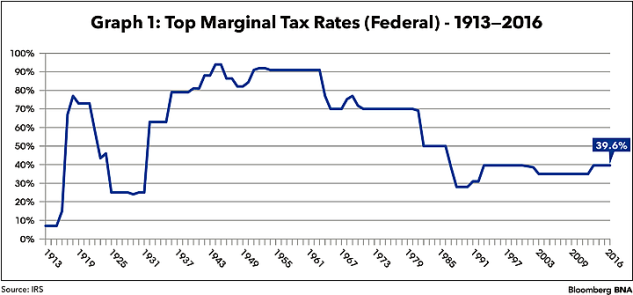

Graph 1 shows a somewhat simplified history of the top marginal income tax rate in the U.S. from 1913 to 2016, excluding such items as Social Security and Medicare taxes, as well as the effects of the phase outs of deductions and exemptions. As you can see, the history contains sudden swings of 20 to 50 percentage points in both directions. (Social Security and Medicare taxes are properly excluded from this analysis, because 401(k) contributions—whether regular or Roth—do not reduce your Social Security or Medicare taxes, and withdrawals from 401(k) accounts are not subject to Social Security or Medicare taxes. Phase outs of deductions and exemptions would generally be relevant to the analysis, but typically account for no more than one to two percentage points in the marginal tax rate, and so would not materially change the results.)

If Graph 1 is insufficient to convince you that you cannot predict your future income tax rates, consider this: discussions of tax reform often involve partial replacement of individual income tax with various forms of consumption taxes, such as a national sales tax, a value added tax or a border adjustment tax. Tax policy discussions also typically involve the idea of reducing rates and simultaneously eliminating deductions, or in the other direction, increasing rates while increasing the standard deduction. Such reforms might well make our tax structure more economically efficient, or more fair, but they also provide the opportunity for wild swings in both directions in marginal income tax rates. In fact, Congress could raise taxes while reducing marginal income tax rates, or reduce taxes overall while dramatically increasing marginal income tax rates.

In addition, it has often been the case that various forms of income are taxed at different rates. Currently, realized capital gains are tax favorably, while unrealized capital gains are not taxed at all (until realized). Income from employment is generally taxed at a higher rate due to Medicare and Social Security taxes, but for many years the top marginal rate on income from employment was 50%, while the top marginal rate on other income was 70%. The Affordable Care Act contains a Medicare tax only on investment income. So, tax rates on the one hand of income from employment, and on the other hand of withdrawals from 401(k) plans and IRAs, could easily go in different directions, with either one going up or down, and the other going in the same direction or the opposite direction.

If you base your decision on Roth vs. regular 401(k) contributions on the future direction of tax rates, the proper question is: will your marginal tax rate on retirement plan withdrawals when you retire be more than your marginal tax rate now on earned income? It is impossible to know.

Our recent history—since the Bush I presidency—has involved more moderate swings in tax rates than most of the 20th Century. However, this seeming trend toward stability is also an illusion. More than ever before, control of Congress and the Presidency can be shifted by a small number of voters in a small number of Congressional districts. In 2016, a shift of fewer than one-half of one-percent of all voters, strategically placed, could have given Democrats control of both houses of Congress as well as the White House. Given the recent exercises of the “nuclear option” by the Senate to eliminate filibusters of presidential appointments, the possibility exists that the legislative filibuster will disappear as well, and a single party controlling both branches of government by even the slimmest margin could control tax rates with no input from the other party. With the two parties espousing significantly different ideas about economic efficiency and fairness, the recent relative stability is no guarantee of future stability in income tax rates.

Save More for Retirement, in Stuff

The discussion above comparing Jane (who used regular 401(k)) and her twin brother Jim (who used Roth) showed that Jane and Jim both reduced current consumption by the exact same amount, and had the ability to buy the same amount of stuff in retirement. However, Jane, who is over age 50, can increase her 401(k) by only 20%, from $20,000 per year to $24,000 per year (the 402(g) limit, with a catch up). Meanwhile, Jim can increase his Roth 401(k) contribution by 85%, from $13,000 to $24,000. Another way of looking at this is that, at the 35% marginal rate, Roth 401(k) allows for 54% more retirement savings, measured in stuff. Change the federal tax rate to 39.6% and add in a state tax of 5.75%, and the advantage of Roth, at the maximum level, increases to 76%.

If you are bumping up against the $18,000 limit or $24,000 limit, and you would like to save even more, you should consider switching from regular 401(k) to Roth.

Non-Discrimination Testing (“NDT”)

A closely related concern is the annual NDT testing applicable to 401(k) plans. In many companies, highly compensated employees are limited to contributing some maximum percentage of pay. In other cases, the highly compensated employees contribute up to the $18,000 limit (plus catch up, which is not subject to NDT testing) but at the end of the year receive some of that back in the form of NDT refunds. In either case, if an employee is hitting the limit or getting a refund, using Roth rather than regular 401(k) would enable the employee to reverse the effect of the NDT limit, either partially or entirely, when retirement savings is measured in stuff.

Note that for purposes of the non-discrimination tests, Roth 401(k) contributions are treated the same as regular 401(k) contributions. In fact, the two are aggregated before testing.

Roth for the Very Young or Low Wage Worker

As explained above, knowledge of the future is generally an illusion. However, there are some workers who can reliably predict that their income tax rate in the future will be greater than it is now. Many workers pay no income tax at all—their income is less than the sum of the standard deduction plus their exemption. Further, many of these workers are in a position to save a substantial percentage of their rather small incomes.

For example, high school and college students who are supported by their parents often work to earn “extra” money or to gain valuable skills or build their resumes. Young workers recently out of school may have low incomes but may still have the frugal lifestyle of their student days or very low expenses because they live with their parents. An unmarried couple may have one partner with very low income (and a zero or low tax rate) while the other partner pays most of the expenses. Even mature workers with affluent lifestyles may find themselves in this position. For example, a worker who has been laid off or retired may have substantial assets (perhaps even from a severance package) and yet, between full-time jobs, have a part-time or temporary job and very little taxable income.

Your tax rate does not have to be zero for this analysis to work for you. If your marginal tax rate is 15%, you may not be certain in which direction it will go. However, you can say that it could go up by a lot, but could not go down by much. Thus, considering both the probability and potential magnitude of increases and decreases, it is generally better to bet that it will go up. For workers who fall into each of these categories, Roth 401(k) is a better choice than regular 401(k).

Skim off the Top—In Retirement

Even if you don’t know where your top marginal tax rate will be in retirement, one thing has been a constant in our income tax structure for many decades: not all income is taxed at the top rate. Whatever your top bracket will be when you retire, you can eliminate the top bracket, or reduce the amount of income subject to the top bracket, by taking some of your retirement income from a Roth 401(k) account or Roth IRA.

Roth and Regular 401(k)—Not a Binary Choice

Roth works best when your tax rate in retirement is high. However, not all of your income will be taxed at the highest rate. If you expect to have other sources of taxable retirement income—such as a pension or part-time work—then it may make sense to put all of your 401(k) contributions into Roth 401(k). However, if your retirement income is going to come primarily from withdrawals from 401(k), then, unless your current tax rate is zero or 15%, you should have some savings in regular 401(k). In retirement, your regular 401(k) withdrawals would fill up the lowest tax brackets before you start withdrawing from Roth 401(k). Obviously, this strategy works only if you split your savings between regular and Roth 401(k).

Premature Withdrawals

The best use of 401(k) is to save for retirement, and hopefully your savings will be there for your retirement. However, if you anticipate the possibility that you will have to withdraw your money from your 401(k) account sooner, for other purposes, then you should consider an advantage of Roth 401(k). When you take a premature distribution from your regular 401(k) account, the entire amount is taxed, and usually there is a 10% excise tax on top of the ordinary income tax. On the other hand, when you have a premature withdrawal from your Roth 401(k) account, only the portion of that withdrawal that is attributable to income is taxed, and only that taxable portion is subject to the 10% excise tax. Thus, you do not have to withdraw as much from your Roth 401(k) account, and your premature withdrawals from Roth 401(k) are subject to much less in penalties.

Leave Money to Your Heirs

You may be in the enviable position of not needing all of your retirement savings for yourself. If you are using 401(k) as a vehicle for accumulating wealth to leave to your heirs, then Roth 401(k) may be a superior vehicle. With a regular 401(k) account, you must begin withdrawing your money (and paying taxes on it) the year after you reach age 70-½ (assuming you have terminated employment, or are a 5% owner). However, with Roth 401(k), you can allow your savings to continue to build, with tax-free investment earnings, for as long as you live, and leave that money for your heirs.

Political Risk

Despite the many advantages of Roth 401(k), it has one disadvantage that is impossible to quantify but nevertheless worthy of consideration—political risk. This is the risk that Congress will change the tax laws in ways that are particularly harmful to those who save using Roth 401(k).

Of course, regular 401(k) also has a political risk—that Congress may increase tax rates. However, virtually all workers consider this possibility—in fact, most people overestimate the likelihood of this contingency. The political risks associated with Roth 401(k) are both more subtle and more substantial.

In evaluating political risk, it is perhaps instructive to consider why Roth 401(k) is so attractive to Congress. The discussion above comparing Jane and Jim shows that in the initial case, they each reduce their current consumption by the same amount, and each have the same amount to spend in retirement. A similar analysis would show that the effect Jane and Jim have on federal tax revenue, over the long-haul, is also the same. Jane and Jim have the same long-term impact on the federal deficit and debt. Jim, however, using Roth 401(k), can increase his savings by 76% while Jane, using regular 401(k), can increase her savings by only 20%. Thus, if each of them were to save the maximum, Jim would save more for retirement, and therefore reduce federal taxes, and increase the federal deficit, by a greater amount. Why then would Congress prefer Roth 401(k) savings to regular 401(k) savings?

The answer, unfortunately, is not that Congress would like Jim to be able to have a more comfortable retirement. Rather, Congress does not look at the federal deficit on a long-term basis. At any given time, Congress looks at the federal deficit over a period of the next ten years. Jane is reducing her federal taxes today. Jim, by comparison, will pay less in taxes in the future. Part of that future is beyond the ten year window that Congress considers. Thus, the reduction in Jim’s future taxes is ignored entirely in the analysis of whether a new law increases or decreases the deficit. When Congress declares a new law to be “deficit neutral,” it just means that federal revenue over the next ten years is not projected to go up or down. The loss of revenue in years 11 to forever is not measured or considered.

Thus, the introduction of Roth 401(k) is considered a revenue raiser, even if the long-term effect is to increase the deficit. Similarly, new laws making Roth more attractive, or allowing things like in-plan rollovers into Roth, raise revenue as Congress measures it, while making the real long-term deficit worse. That fictional revenue raising quality is used to justify more current spending or other tax cuts.

However, the future eventually arrives. Having eroded the future tax base by shielding future income from taxes, Congress will eventually have to find new sources of revenue to replace the lost income from withdrawals from retirement accounts. That new revenue may come from entirely different sources—consumption taxes, carbon taxes, reduced deductions and exemptions, higher rates, corporate taxes, import duties, etc. But future shielding of Roth 401(k) withdrawals from taxation is not a contractual right or Constitutional guarantee—it is nothing more than current law, just as changeable as any other tax law.

To understand why the political risk is greater for Roth 401(k) than for regular 401(k), let’s take one more look at Jane and Jim, now when they are retired. Jane is withdrawing money from her 401(k) account and paying 35% in taxes on each withdrawal. Congress could raise her tax rate, and may well do so. However, Jim is withdrawing money from his account and paying no taxes currently—there is much more room to increase his tax rate. Moreover, while Jim already paid tax back when he was working, he has never paid tax on the investment earnings, and never will. The measurement of retirement savings in stuff shows why this is irrelevant. Jim’s taxes gave as much benefit to the government as Jane’s, but Jim appears to have taken advantage of a “loophole” that Jane did not, and appearances are politically important even if economically irrelevant. Further, if Jim and Jane both increased their savings to the maximum (76% for Jim and 20% for Jane) then Jim simply has more purchasing power than Jane, and taxing Jim would therefore seem more reasonable to Congress. Also, the group of people who utilize Roth tend to be wealthier on average than those who utilize regular 401(k) and therefore easier political targets.

Similarly, the possibility of future tax changes that are favorable to regular 401(k) participants represents a “risk” that the decision to make Roth contributions will have been suboptimal. Despite the government’s likely voracious future appetite for revenue, many likely tax increases could reduce the tax on future 401(k) withdrawals. These include:

- A national sales tax, value added tax, carbon tax, gasoline tax, border adjustment tax, or other consumption tax, combined with lowering the income tax rate. The additional taxes would be neutral as between Roth 401(k) and Regular 401(k), while the reduced tax rates would help only regular 401(k) participants.

- Expansion of the tax base by limiting or eliminating deductions, exclusions, adjustments and exemptions, combined with lowering rates.

- Increasing tax rates for very high income individuals while reducing tax rates—or leaving them as is—for the “middle class.”

- Raising or eliminating the cap on Social Security taxes with corresponding reductions to ordinary income taxes. 401(k) withdrawals are not subject to Social Security taxes.

Perhaps the greatest source of political risk is simply buyer’s remorse. Previous Congresses used an accounting gimmick to justify spending money in the past on the theory that Roth 401(k) reduces the deficit, when in the long run it does the opposite. Future Congresses may not appreciate that erosion of the tax base, and may not have much sympathy for those who took advantage of it.

Conclusion

Predictions about the future direction of tax rates are unreliable. However, despite the uncertainties, Roth 401(k) can be an effective way of boosting retirement savings for those bumping against a limit, or for those who find themselves temporarily in a very low tax bracket. It can also be part of an effective strategy for managing taxes in retirement to avoid the highest tax rates. For employees at the very top and very bottom of the income scale, Roth 401(k) is likely to be a better choice than regular 401(k).

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.