In response to proposed Department of Labor (“DOL”) Fiduciary Rules specific to the provision of investment advice and avoidance of conflicts of interest, a substantial number of mutual fund organizations have implemented share classes (often referred to as “clean shares”) that eliminate all indirect expenses that had been incorporated into the expense ratio of the fund. By eliminating marketing fees (front or back-end sales charges, 12b-1 fees) and distribution fees, investment costs are lowered and conflict of interest concerns are lessened.

For individual investors, clean share funds provide their financial advisor with the ability to act in their best interest and adhere more closely to the fiduciary standards contained in the proposed DOL rules. Assuming that the advisor is no longer collecting commission payments, the individual participant is free to negotiate a fee arrangement that is determined as either a percentage of assets, a fixed annual fee, an hourly charge, or a combination of these various alternatives.

For retirement plan sponsors, and by extension individual retirement plan participants, the usage of clean shares eliminates revenue sharing payments that may be used to offset the costs of administrative services. By eliminating revenue sharing payments, the retirement plan sponsor, just like the individual investor, must then negotiate fee arrangements with service providers (recordkeeper, investment consultant, Trust Custody provider, for example) to ensure that each is appropriately compensated for their services. In the same manner as the individual investor, these fee arrangements may be structured in the form of fixed annual fees, asset-based fees, hourly or by project rates, or a combination of these alternatives.

Although clean share classes lower investment costs, they may, depending on the decisions made by the retirement plan sponsor, actually result in higher retirement plan costs and greater costs for certain individual participants. Retirement plan sponsors that are considering changes to their fee and service arrangements should consider the completion of a comprehensive cost analysis and consider how the changes will impact different groups of participants prior to proceeding with share class changes and modifications to fee arrangements.

Higher Plan Cost Example

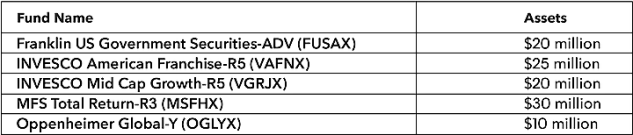

To illustrate how retirement plan costs may increase using lower cost clean shares, assume that the investment fund offerings for our illustrative retirement plan sponsor include the following actively managed funds and assets under management (go to http://src.bna.com/qgb).

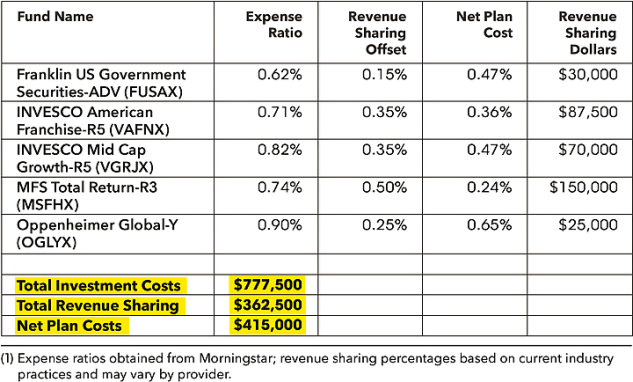

In accordance with the current fee and service arrangement established with the service provider, the fund expense ratio, revenue sharing offset, net expense ratio, and revenue dollars (all revenue sharing is used to offset participant recordkeeping fees), are as follows (1) (go to http://src.bna.com/qgd).

In certain instances, the transition to clean or lower cost share classes results in no additional retirement plan costs. This situation occurs when the expense ratio reduction is equal to the revenue sharing reduction.

For example, the R4 class shares of the American Funds EuroPacific Fund (REREX) have an expense ratio of 0.85% with a 0.35% revenue sharing offset, resulting in a net plan cost of 0.50%. The lowest cost share class (R6 class shares (RERGX) have an expense ratio of 0.50%. For the retirement plan sponsor the decision to change to the R6 class shares is not an economic one (the expense reduction is equal to the revenue sharing reduction) but is instead a decision as to how administrative fees are paid by plan participants.

In other instances, however, the expense ratio reduction is less than the revenue sharing reduction. When this situation occurs, plan costs actually increase even though the plan sponsor is engaging in what would be an appropriate fiduciary decision to lower investment costs.

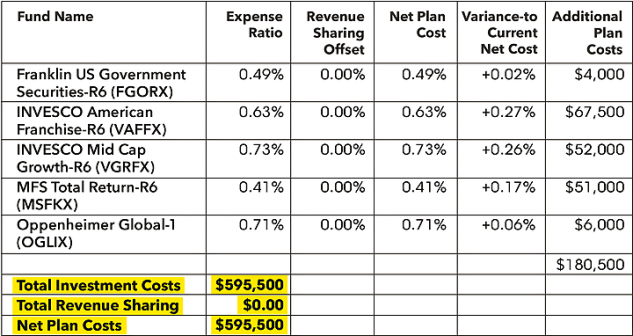

Assume our illustrative plan sponsor decides to transfer the five funds referenced above to the lowest cost or clean share class. The fund expense ratio, revenue sharing offset, net expense ratio, variance to current net costs, and additional plan costs are as follows (go to http://src.bna.com/qgf).

In the above example, the investment management fee reduction is less than the revenue sharing reduction, resulting in higher plan costs.

Assuming that the service providers are currently receiving reasonable and appropriate compensation for services, the plan sponsor or plan participants will need to fund $362,500 of fees that were previously paid from revenue sharing offsets. Depending on how the plan sponsor elects to charge the additional fees, costs for small balance participants may increase while costs for participants with large balances may decrease.

Individual Participant Effect of Share Class Changes

Using the same funds in our example, assume that Participant A has a $200,000 balance allocated in equal 20% increments across all five funds. Under the current arrangement, Participant A incurs $1,516 in investment management fees. Of this amount, $640 represents revenue sharing payments used to fund the costs of administrative services.

Participant B has a smaller balance (assume $20,000) that is also allocated in equal 20% increments across all five funds. Participant B pays investment management fees of $151.60 and contributes $64 in revenue sharing payments to fund the costs of administrative services.

Transitioning to the lowest cost or clean share classes reduces investment management fees for Participant A by $328 and by $32.80 for participant B. If the plan has 5,000 participants and the plan sponsor elects to transition to a fixed fee arrangement, each participant would be subject to a $72 annual fee to offset the reduction in revenue sharing payments. In this example, Participant A would experience a net annual cost reduction of $256 (investment management fee reduction of $328 and administrative fee increase of $72) while Participant B would experience an annual cost increase of $39.20 (investment management fee reduction of $32.80 and administrative fee increase of $72).

In this example, and certainly one that is not unique within the retirement plan servicing industry, the decision on the part of the plan sponsor to change share classes should be viewed as one that may not benefit all plan participants equally. Plan sponsors seeking to lower investment costs through share class changes need to fully understand both the cost impact of the change at the plan level and how that impact will effect individual plan participants.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.