The Latin phrase “suum cuique pulchrum est” is loosely translated to the common saying “to each their own is beautiful,” meaning that people find their preferences attractive and reasonable for their unique circumstances. Asset owners appear to have applied this approach to choosing governance practices for the selection of investment managers for their Defined Benefit (DB) or Defined Contribution (DC) plans. In some cases, plan sponsors utilize their own internal teams for that activity, while in others, the organization opts to hire outside advisors to make recommendations upon which the sponsor may or may not act. Additionally, more frequently than ever before, asset owners are taking the alternative route of fully or partially outsourcing the asset-manager-selection process to a third party in a fiduciary role. As each organization considers these options, how then should the plan fiduciary decide which option is the most beautiful?

Ultimately, a degree of introspection is required. What are the asset owner’s core strengths? What are its weaknesses? How are finite resources best allocated? The answer(s) to each of these questions depends very much on the asset owner’s unique circumstances. And, in the end, there is no “one-size-fits-all” solution that can be used to determine the optimal approach.

In any case, for a plan sponsor considering the best governance approach for a DB or DC program, we suggest a reasonable practice is to consistently employ the same five assessment criteria that have been used to evaluate manager skill for decades: philosophy, process, people, price, and performance. Interestingly, this methodology can be directly applied not only to the decision regarding which of the options above should be selected, but also to the potential service providers if the final decision is to use one or more external vendors. Let us review each of these characteristics in some detail.

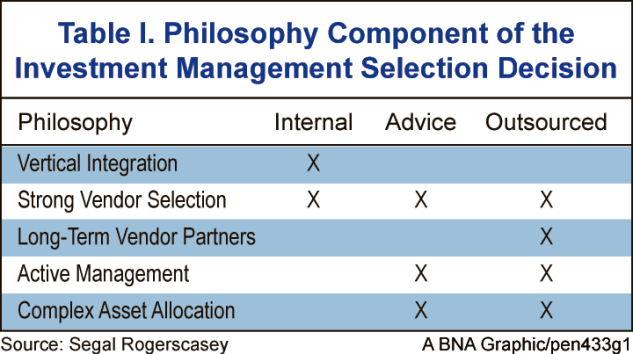

Philosophy

For an asset manager, philosophy might relate to some notion of what drives stock prices or which market inefficiency should be capitalized on. In this context, philosophy relates to a broad business approach regarding the use of outside agents. Does the organization generally prefer to be vertically integrated? Is there a baseline view that the entity’s practices and policies are by nature of such a high caliber that the use of external vendors tends to consistently lower the quality of the outcome? Or, conversely, is the vendor review process that is embedded in the firm so successful that the level of quality is unaffected by the option of in-house versus external?

Also important, particularly as it relates to advisors or implemented services (often referred to as outsourcing), is the nature of the partnerships developed with vendors. If the tendency is to think of vendors as commodities that can be easily traded based upon simple criteria, then the advice option may be more reasonable because changing full-fiduciary vendors is potentially more complicated and costly.

There are also behavioral issues to consider. Many asset owners tend to be overly short-term in their investment focus, leading them to “buy high and sell low,” as opposed to the much more profitable outcome of buying low and selling high. Human behavior is such that without experience (i.e., learning the hard way), many people (and investment committees) tend to overestimate the importance of recent, trailing performance in making investment purchase and sale decisions (including those of asset managers), often getting whipsawed in the process.

Moreover, many investment committees and boards tend to gravitate more toward “defensible” as opposed to “optimal” decisions, meaning that investment committees and boards often intentionally hire an asset manager that has recently exhibited strong performance because that decision “looks good” to other constituents who are evaluating the plan sponsor’s decision-making skills. Never mind the fact that in too many cases, the asset manager that “looks good” at any point in time then often has relatively more expensive securities in its portfolio (limiting future upside potential) and, worse, faces the prospect of short-term losses due to reversion to some longer-term performance mean.

In the end, individuals and organizations, which seem to suffer from these behavioral biases, may be better off delegating asset manager selection to a third party, regardless of other factors.

There are also very relevant fundamental questions that may affect this decision on a philosophical level. Does the organization believe in active portfolio management over passive management? Is the potential for excess active return generation important in terms of achieving entity investment goals? If the answer to these would result in an active portfolio management bias, many asset owners may lean toward using external advisors or outsourced solutions, as identifying and evaluating actively managed strategies is usually more complex and time consuming. Also, are potentially more complicated alternative or nontraditional investments an important element of the asset allocation either by preference or need? Again, if the answer is yes, then this also adds complexity that may benefit from either specialized advice or outsourced investment implementation.

Process

To select asset managers successfully, defined as those that meet or exceed their stated objectives in terms of return and risk on a prospective basis, asset owners must engage in a defined evaluation process. This is not a trivial task as represented by two observations: first, net-of-fees, most asset managers fail to exceed their return benchmarks over reasonable periods; and second, statistical measures such as an evaluation of past performance are demonstrably inadequate as predictors of future returns. In short, the asset owner seeking to add value via manager selection is choosing from a set of options that, on average, tend to be below their benchmarks, and the simplest form of analysis is of limited value.

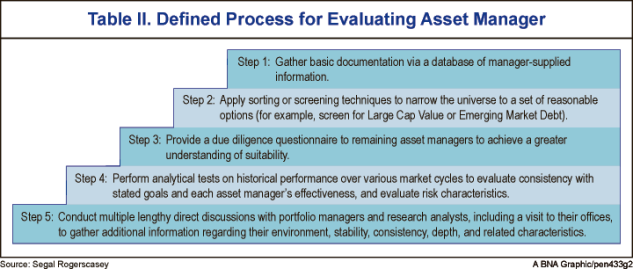

The asset owner, or vendor, seeking to overcome these disadvantages, must employ a rigorous process of assessment to succeed in that endeavor. A successful process has two principle elements: a methodology for gathering relevant relative information from which to reach a conclusion and a systematic technique for evaluating that information to provide insight into the potential for adding future value. Table II represents a typical data sourcing exercise for the sponsor:

Once information is gathered, or in most cases coincident with that track, there must be a methodology or technique for assessing the now substantial set of data points and observations. At this stage, the asset owner must take data and convert it into meaningful insights and then the insights into conclusions. To accomplish this effectively, there are several important preconditions:

- There must be demonstrable conditions or criteria to which successful asset management results can be ascribed.

- There must be adequate breadth of product/asset firm assessments to enable comparison of the various conditions or criteria on a relative basis (it is impossible to know excellence without knowing the lack of excellence).

- There must be a repeatable mechanism or system for housing the collected data and for performing the comparative process described above.

As a brief—and not complete, by any means—example of this part of the manager-selection process, we could consider an assessment of the investment management firm’s strategy. It is important to understand if a manager’s thesis for adding value above a comparable benchmark is compelling:

- What is the value proposition?

- What is the targeted market opportunity or inefficiency upon which the manager is seeking to capitalize?

- Does that inefficiency truly have the potential to generate attractive risk adjusted returns?

This perspective—the answers—then need to be compared with other similarly situated investors to determine if Firm A has a superior thesis than Firm B and then continuing this out to Firm X, and so on. This comparison can best be accomplished by maintaining a repository of responses to enable side-by-side analysis. An asset manager’s strategy is but one of seven key criteria that we consider in this assessment, in addition to more than 30 sub-factors.

It is also important to recognize that this data collection, development of insights, and comparison process will have to be performed across all asset classes, styles, and sub-styles for a substantial number of firms and products to have a robust set of options suitable for investment. Complicating matters, the firms and products covered are not static—they often exit the system via failure or closing or corporate actions (mergers, lift-outs, etc.) and they enter the system via spin-offs, product development, new entities, or just showing up on the radar screen. And, they change—the meetings, assessments, and insights have to be refreshed continuously in some fashion. A firm or product that appeared superior to the evaluator on January 1 when the assessment process was completed may have experienced significant change by July 1 when the asset owner actually makes the planned investment. Count on updating, prior to actually investing, for assurance that the conclusion is still valid.

After this—the confirmation of skill and the hiring—there must also be a process for ongoing evaluation and potential reversal of the original conclusion. It is not enough to know which asset manager to hire and when, but the asset owner must also be able to decide when to fire the manager, or simply take profits, rebalance risks or redeploy assets to more promising opportunities.

People

It is effectively impossible to accomplish all this merely by employing machines or process templates; instead, people must be involved at every step. A successful manager selection process requires these people to create the process itself, to develop the conditions and criteria, to assess skill and reach conclusions, and, finally, to monitor, both results and changes, to assure that the original conclusion retains validity. A significant volume of complex and highly specialized work is necessary. An asset owner typically cannot simply reassign other personnel to this function and certainly cannot bring inexperienced people in and have them have at it, learning at the organization’s expense.

The development of experience necessary to have insights that lead to success in this endeavor usually takes many years, and in several areas, such as private equity and hedge funds, complexity increases the degree of difficulty that much more. In many cases, it is very beneficial to have additional training, such as advanced degrees or designations, demonstrating a certain level of core competency. Said another way—successful asset manager identification and retention requires people who are credentialed, have specialized skills, and are probably not cheap. The number of people needed is a difficult question on which to generalize. There are several variables that come into play here:

- the experience of the people,

- the complexity of the investment program,

- the active versus passive allocation,

- the number of managers and size of the fund, and

- the governance structure and budgets.

These are all relevant to the answer. There is also the question of direct in-house asset management: Will security-level decisions be made by the staff through running live portfolios?

It would be possible to consider the asset consulting industry as a comparative for the kind of team necessary to manage investment functions in-house, but this is a difficult benchmark for several reasons. First, most firms manage multiple clients and so must have even broader coverage to enable them to respond to the customized needs of those varied interests and needs.

In addition, many have consultants who perform research functions as well, making a direct count of “research” personnel difficult. They also typically perform asset allocation and asset liability work often with research staff, and this may confuse any apples-to-apples comparison on the number of people required to manage an effective manager research process.

Another method to gauge necessary staffing would be to look to the plan sponsor or asset owner community. Unfortunately, that is an equally difficult source for directly comparable information given there are so many different models and approaches to the required activities. Ultimately, the variables to consider to assure comparability include:

- Does the plan sponsor use an external advisor? If yes, for what purpose?

- Does the plan sponsor run money directly internally?

- Does the plan sponsor use funds of funds for alternatives?

- How many managers does the plan sponsor have?

- How experienced is the plan sponsor’s team?

- How complex is the investment program?

- Does the plan sponsor use active or passive investment strategies?

Finally, and perhaps most importantly, how successful has each plan sponsor, consultant, or advisor been at adding value? It makes little sense to base a conclusion about a staffing model on examples that have failed to achieve success. In some cases, answers can be discerned from publicly available information, but it is impossible to develop a robust set of disaggregated answers to form a truly informed opinion to respond to the base inquiry. How many people and what type of organizational structure would be required to provide a high degree of confidence of success in an internal manager research operation given the goal of adding value across a broad spectrum of asset classes? The answer is quite opaque and a source of continuous debate in the industry. Perhaps the notions of price and performance, our last two elements, can add to the level of transparency on this question.

Price

In considering the price component of our analysis, we can broadly compare our three potential models (insourcing, advice, or outsourcing). With in-sourcing, the price is the cost of building that staff described previously—office space, tools and databases, travel, and, of course, compensation and benefits. Additionally, there is the issue of opportunity costs. In a world of limited resources, there are often better uses of finite capital, human and financial. By diverting scarce resources to activities outside an asset owner’s area of specific expertise, organizations risk becoming “penny wise and pound foolish.”

The price piece also includes the typically underestimated cost of retention and change. Obviously, when people make career choices, they may move to “greener” pastures and the plan sponsor must not only be prepared to recruit and train, but also must have the “bench” strength to manage during that period.

Market forces do not conveniently wait for the investor to get someone on board and up to speed, and there is a large opportunity cost in the interim. How would a plan sponsor feel if an asset manager with stewardship for plan money, after losing a key portfolio manager, said, “We’ll just hang while we get someone else on board”? In all likelihood, the manager would be summarily terminated. This is a key weakness of the insource approach—it may be economical to have a base team of professionals, but not as economical to have the required depth.

Another key element is the nature of compensation in the investment business; sponsors often have political or other barriers to providing adequate levels of pay to attract and retain the necessary talent. When markets are high (valuations stretched), asset managers can best afford to pay up for people, hiring away sponsors’ talent and making for slim options for replacement, at exactly the time that talent is most important as the next phase of the investment cycle is often a retrenchment.

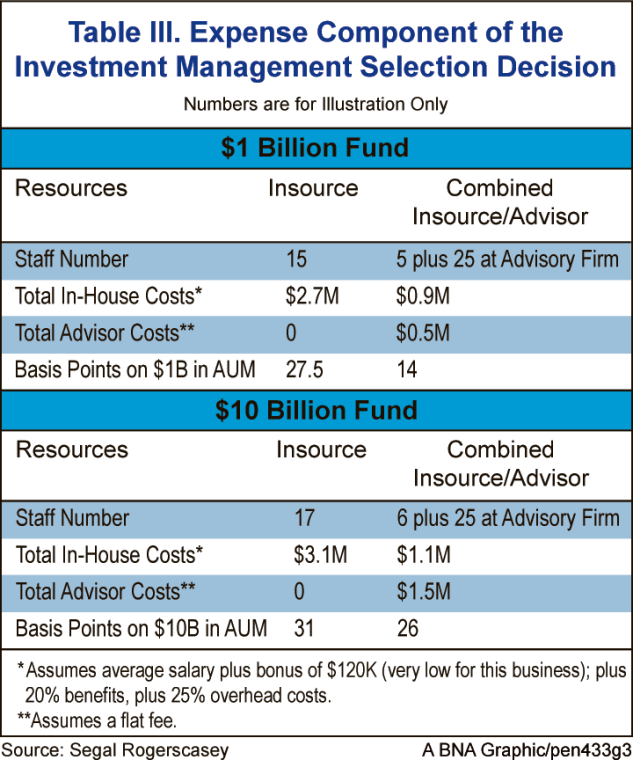

These and other factors are significant reasons why many sponsors have opted for the “staff plus advisor” solution. In this way, internal staff can provide leadership and perspective for the investment effort, taking on substantial amounts of the translation of asset owner’s needs to the program, while supplementing that with the breadth and depth of staff of an advisory firm’s research and consulting team. In addition, the plan sponsor benefits from the leverage inherent in the advisor’s ability to provide similar services to a host of asset owners. The favorable economics of this approach are demonstrated in summary fashion (numbers are for illustration only) in Table III.

The number of staff or research resources at the advisory firm may be variable, but if one simply considers there are five big asset categories (Stocks, Bonds, Absolute Return, Hard Assets, and Private Equity) and adds a few folks for support and a few more for big picture asset allocation/Asset Liability Modeling, then both seem reasonable base needs. There is also performance reporting, custodial search/oversight, risk-management, rebalancing, and related support duties that are required to be performed.

Extending our comparison to a $10 billion fund (Table III), and noting that advisory work generally is not priced purely based on assets (there is usually a sliding scale that declines as assets increase), we could note that the basis points tend to converge, although it is impossible to definitively calculate at what level, again given that the complexity of the larger fund may also increase with assets under management.

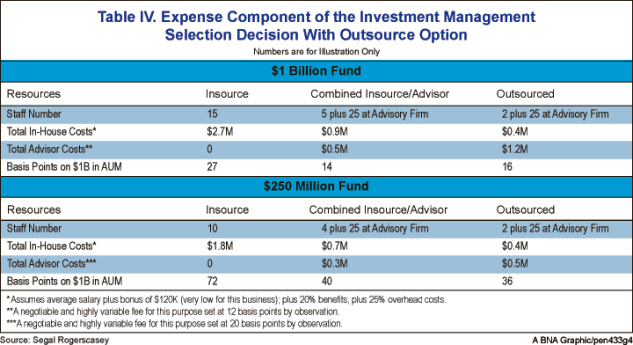

Next, let us add the outsourced option to our equation. In this case, we would expect minimal internal staff. The staff could drop from 15 or 5 people, respectively, in the above examples, to 2 people under the outsourcing option. In Table IV, we estimate the following price comparison for the $1 billion fund.

If, however, we assess potential advantages for a smaller, say $250 million sponsor, Table IV shows fee compression favoring the outsourced solution.

It is important to note that these numbers are for illustrative purposes and can vary widely due to a variety of factors, including complexity, geography, and competitive environment. There are also other considerations that must be assessed in making this comparison:

- How important, or valuable to return, is the ability of an internal staff to directly translate sponsor goals and objectives into results? Is there slippage when applying the advice or outsourced models?

- Can the outsourced model avail itself of reduced fees through collective negotiation?

- Can the outsourced model operate more efficiently in the translation of research insights into portfolio strategy?

- In the event of poor results, which model is the most straightforward to modify to enhance the outcome?

In short, as with most things, it is not only the absolute level of fees that should be the primary determinant, but the expectation of favorable results net of those fees. It is of note here that, just as with the world of active investment management, the successful combination of the factors necessary to generate return above a policy benchmark or to achieve stated plan goals is no easy task, with both winners and losers.

Performance

This leads comfortably into the last element in the process of assessing the optimal governance structure for the asset owner/plan sponsor: performance. Although it is often (and justifiably) said that past performance is not necessarily an indicator of future results, the numeric representation, properly evaluated, can provide valuable insight as an effectiveness metric. Historical returns are also quite straightforward and transparent—either the fund/manager met, failed to meet, or exceeded the goals as established. This clarity and simplicity is likely the prime explanation for the ingenuity with which service providers (both advisors and outsourcers) have sought to shroud their own results.

Interestingly, the most transparent performance assessments of a plan sponsor’s success come at the total plan level. Even this is often confused by focusing on the misdirection of peer group comparisons, which are a distant third in terms of decision-making value, or the assessment of success (the first and second are results versus plan objectives and results versus policy benchmarks, respectively).

Those providing investment advice will claim that the nature of their contractual relationships and the services provided is such that the results of their clients cannot be fully attributed to them. Conversely, they will make impossible claims that both fail the test of logic or are completely unverifiable. (Heard at one major investor conference from a senior executive of a major advisory firm: “All of our clients have outperformed their benchmarks.” Ah, where is the Securities and Exchange Commission when you need it?)

The outsourcers also will cloud the issue by noting that “all our clients have different benchmarks,” or “given that only a portion of the decision making is outsourced, total plan results are not an appropriate measure.” While there is certainly some element of validity to these disclaimers (perhaps “distractions” is a better term) there are ways to assess both the outsourcers’ advice and ability to add value. Consider the overall effectiveness of their manager research process—have they generated excess returns on their universe of recommended managers over time? Can you judge the excess return versus policy benchmark for the clients that have outsourced part or all of their decision-making process? Imperfect disclosures certainly, and ones requiring substantial footnotes to divulge, but complexity or imperfection does not equate to uselessness.

Conclusion: Vive le Différence!

In short, there are some simple tests that sponsors can perform to determine if their current governance structure (the combination of philosophy, people, and process) should be reexamined. First, over a reasonable time frame (at least one market cycle at this level, perhaps two), has the asset owner’s total asset pool achieved the two primary goals (absolute and policy benchmark relative) with reasonable levels of risk? Second, has there been any change, positively or negatively, that would lead the asset owner to believe that the results that were achieved will be more or less favorable than what could have been achieved?

If the answer to the first question is “No” and the second is also “No,” then it is likely time for a review of the governance process, including not only the decision-making and the “in-house versus advisor versus outsource” question, but also who the organizations and people involved are.

If the answer to the first question is instead “Yes,” and then the answer to the second question is “No,” we would still suggest establishing a periodic methodology to assess the ongoing effectiveness of governance, for the best way to stay good is to continuously improve.

The French like to say “vive le différence,” putting a very positive spin on our opening Latin phrase and, in this context, compelling us to recognize that in the world of plan investment governance, the existence of competing models is a good thing. Yet, we would add that being different is not what makes a solution good or effective, but rather what is most beautiful (defined as likely to meet a plan’s goals) is that which fits the specific circumstances of that organization. Often that begins with a clear understanding of the definition of success. As businessman, philanthropist, and author W. Clement Stone said in numerous publications and interviews, “Definiteness of purpose is the starting point of all achievement.”

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.