With financial markets in distress and employers making every effort to rein in expenses, it is no surprise that defined benefit pension plans are again under increasing scrutiny.

In response to demands on employers to manage expenses, along with recognition that many employees no longer spend their entire careers with a single organization, employers have reevaluated their commitment to retirement benefits. For many workers, gone are the days when employers were paternalistic and provided for their employees’ retirement following long-term service.

With this change in employers’ perception of their obligations to employees came the realization that defined benefit plans were causing a significant drain on employers’ financial health. That drain has been further exacerbated by today’s declining interest rates and market returns. As employers have continued to reduce their employee population and eliminate whole lines of business, defined benefit plans have been closely examined and, in many cases, steps have been taken to mitigate the financial risks associated with these plans.

This article will focus on one particular strategy that employers have undertaken in connection with mitigating the potentially adverse financial consequences associated with sponsoring a defined benefit plan: plan freezes. We will begin by describing why employers have been freezing their defined benefit plans and the different types of plan freeze amendments that may be considered. We will also provide a road map of strategies and procedures, both financial and otherwise, that employers should consider after a plan has been frozen.

Background on Defined Benefit Plans

While we anticipate that the reader is quite familiar with defined benefit pension plans in general, the critical issue with these plans today has been that, unlike tax code Section 401(k) plans, the employer bears the risk of adverse investment experience and fluctuations in interest rates. Thus, when the financial and stock markets drop precipitously, as they have done in recent years, the employer’s financial obligation with respect to the funding of the plan can increase significantly. This increasing financial obligation, coupled with additional plan benefit accruals and longer life expectancies, has made for a perfect storm with respect to plan funding and related accounting. The combination of these events has driven many employers to consider freezing their defined benefit plans to stem the tide of increasing plan funding obligations.

Why Have Employers Frozen Their Defined Benefit Plans?

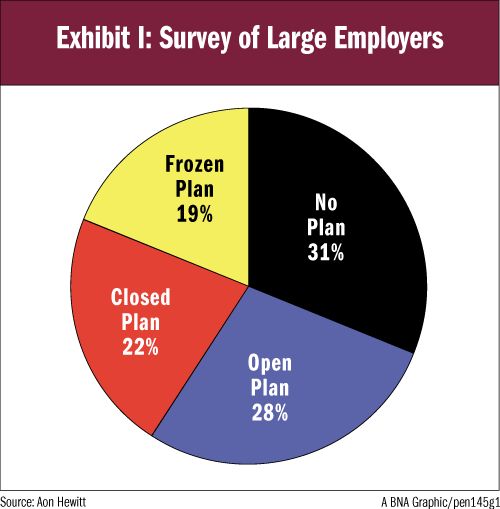

Over the past 10 years, many organizations have frozen, or closed, their defined benefit plans to new entrants. According to a recent study

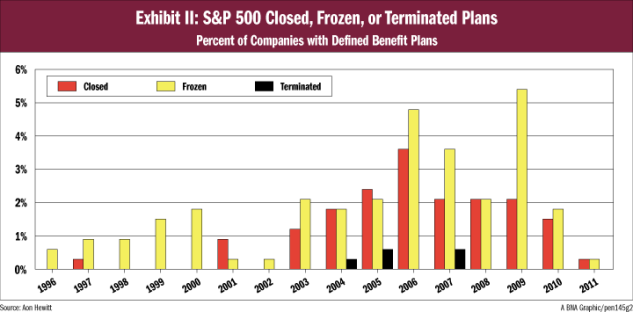

This shift in defined benefit plan sponsorship has mostly occurred in the past five to eight years. Exhibit II in this article shows the percentage of S&P 500 companies that have closed, frozen, or terminated their plans in the past 15 years, with the highest incidence of freeze activity in 2006, 2007, and 2009 (See Exhibit II in this article).

With all of this plan freeze activity, the inevitable question is why have these S&P 500 employers closed or frozen their defined benefit plans? The most common response is cost, both the level of cost and the increasing uncertainty surrounding future costs. In a pension context, cost can mean cash contributions, pension expense, or even balance sheet drain.

While the objective of controlling costs is an admirable pursuit, it is important to remember that without other integrated actions, this goal may not be attained by merely freezing the plan. Cost uncertainty is driven as much by investment decisions and funding requirements as by plan design decisions. Coordination of these activities will help reduce the cost uncertainty. Moreover, as many employers begin to consider offering replacement retirement programs to employees affected by a plan freeze, the full compensation costs associated with any such replacement plan design should be analyzed in determining whether costs and expenses have truly been reduced.

Other reasons employers consider freezing their defined benefit plan include:

- Limited Reaction from Employees. Freezing of defined benefit plans is often an easy target for corporate cost control initiatives since it has a less immediate impact on employees and is generally believed to be undervalued by workforce members, especially younger employees.

- Competition. Competitive pressures, especially from certain industries in which pension benefits are less common, or from overseas where foreign governments may subsidize pension costs, will place the U.S. employer that sponsors a defined benefit plan in a financially disadvantaged position.

- Plan Complexity. Despite the modernization of recordkeeping and calculation systems, defined benefit plans continue to require a significant amount of plan oversight. A plan freeze can reduce some of the complex plan administration and operational requirements although, as we will see below, many of the operational requirements for the plan will continue during the period of a plan freeze.

- Change in Corporate Philosophy. While many employers may have historically designed their plans to provide benefits for long-service employees, with the movement of the workforce among multiple employers throughout their careers, there has been a realignment of the total rewards philosophy, with specific emphasis now being given to shorter-term employment commitments, performance based awards, or more equal pay.

- “Following the Leader” Trend. Employers want to continually evaluate the appropriateness of their benefit programs in light of offerings by their competitors or peer companies. As more plans are frozen, there is an increasing trend for employers in similar industries to follow a similar course of action.

For those employers that continue to sponsor open defined benefit plans, they too may need to evaluate these issues as they find themselves having to defend, with increasing frequency, why the defined benefit plan should not be frozen. In a recent survey,

While defined benefit plan sponsors also reference increasing government regulations and Pension Benefit Guaranty Corporation (PBGC) premiums as continuing concerns with respect to plan sponsorship, as we will see later in this article, those issues do not go away once the plan has been frozen.

Types of Plan Freezes

When an employer is considering freezing its defined benefit plan,

- Hard Freeze. On one end of the spectrum is the full “hard freeze.” In this instance, all participants have their benefit accruals frozen as of a defined date. Employers may decide to fully vest participants at that date

5 Treasury regulations provide that if a defined benefit plan ceases or decreases future benefit accruals, a partial termination will be deemed to occur and full vesting of affected participants would be required if, as a result of such cessation or decrease, a potential reversion to the employer, or employers, maintaining the plan (determined as of the date such cessation or decrease is adopted) is created or increased. If no such reversion is created or increased, a partial termination will not be treated as having occurred by reason of the freeze. - Closed or Soft Freeze. On the other end of the spectrum is closing a plan to new participants, sometimes referred to as a “soft freeze.” In this instance all current participants as of a certain date remain in the plan and continue to accrue additional benefits through age, service, and pay increases just as they did before the plan was closed to new participants; newly hired employees do not become participants in the defined benefit plan. From the perspective of the employer, the soft freeze is generally the easiest to accomplish as it does not adversely affect existing plan participants. In practice, however, the soft freeze can often be the first step to subsequently instituting a hard freeze as the financial concerns that caused the employer to institute a soft freeze are often not sufficiently alleviated with the mere passage of time.

- Combination of Freeze Types. There are several “freeze variations” that may be less severe than the hard freeze that may deserve consideration. Each of these variations is subject to the application of nondiscrimination rules

6 The design of any plan freeze will be subject to applicable nondiscrimination rules under the Internal Revenue Code of 1986, as amended (“Code”). See, e.g.,

- Grandfathered Employees. Some organizations may choose to grandfather a defined population of those who continue to receive additional accruals while those that do not meet the requirements no longer receive benefits. These grandfather rules are often defined based on age, service, and/or points (age plus service). Employers will often look at employees who are five or 10 years away from retirement eligibility as a population of employees that should be protected under these grandfathering rules.

- Separate Business Units. In some larger, multi-industry companies, a pension benefit may be competitive in one part of the business, but not in another part. A company may freeze the benefits for one group and not the other.

- Satisfy Collective Bargaining Commitments. To the extent that the employer operates in a union environment, a plan freeze may be designed only for non-collectively bargained employees.

- Continue Pay Growth. In a final average pay plan, some employers will allow for additional pay growth but freeze the service accruals. This mirrors the Projected Benefit Obligation (PBO) calculation under ASC 715-30 (formerly FAS 87) that counts future pay growth in the liability measure.

- Offer Choice. In an effort to gain more appreciation for retirement benefits, some employers provide their employees with the ability to choose between the current defined benefit plan and an alternative defined contribution plan. Those who elect the defined contribution plan are effectively electing to freeze their defined benefit pension benefit. The provision of participant choice can lead to complex plan administration. The introduction of choice requires significant data needs as well as sophisticated modeling tools to allow employees to make the right decisions. While some employers may find this approach attractive, they need to be mindful of the importance of clear and comprehensive disclosures and the inherent risk associated with employees looking to the employer or plan fiduciaries if their benefits prove to be less attractive than originally estimated.

- Delay Announcement. While not actually that different from a full hard freeze, making the announcement of an intended plan freeze between two and 10 years prior to the actual freeze date may be helpful to employees planning for their retirement, but it may create other employer challenges around workforce planning, benefits modeling, communications, and other business considerations prior to the freeze date.

Freezing the Defined Benefit Plan—

Some Considerations

While we have assumed for purposes of this paper that the reader will be generally familiar with the requirements needed to freeze a defined benefit pension plan, we have provided a brief overview of some of the issues and considerations that will enter into such decision. As a practical matter, the decision to freeze a plan will require significant input from an employer’s human resource, legal, accounting, administrative, and financial organizations in order to address the myriad issues that will arise in moving to a frozen plan.

How to Freeze a Pension Plan

Surprisingly, the minimum requirements for a hard freeze are not very onerous. There are some basic notification and communication requirements to affected participants, but no direct reporting to government agencies is required. While nondiscrimination testing may (or may not) be initially required in connection with the freeze itself, depending on how the freeze is designed, minimum participation rules under tax code Section 401(a)(26) may become an issue over time. Pension curtailment accounting is likely required in the event of a plan freeze, but not settlement accounting. In practice, plan amendments involving less than a complete hard freeze may prove to be more difficult and time-consuming than completely hard-freezing the plan. Some of the more significant plan freeze requirements include addressing:

- Plan Governance. The first and perhaps most important step is to ensure that the proper plan governance is in place. Freezing a pension plan, like any other plan design change, is a plan sponsor or settlor action. It does not involve a fiduciary decision by the benefit, investment, or plan administrative committee and thus is not subject to fiduciary requirements under the Employee Retirement Income Security Act. As a sponsor of a pension plan, an employer generally reserves the right to cease future benefit accruals in its sole discretion (subject to any plan terms or prior collective bargaining commitments). This usually occurs through an action by the board of directors and a related plan amendment freezing the plan.

7 In deciding to freeze a plan, it is critical that the employer ensure that it is following all plan governance and amendment requirements. Failure to have the plan freeze amendment adopted by the board of directors or properly delegated party pursuant to 514 U.S. 73 , 18 EBC 2841 (1995); Overby v. National Association of Letter Carriers,595 F.3d 1290 , 48 EBC 2255 (D.C. Cir. 2010) (38 PBD, 3/1/10; 37 BPR 477, 3/2/10); Coffin v. Bowater Inc.,501 F.3d 80 , 41 EBC 1929 (1st Cir. 2007) (175 PBD, 9/11/07; 34 BPR 2175, 9/18/07).

- Timing of Plan Freeze. In planning ahead for a plan freeze, careful consideration should be given to the effective date selected for the plan freeze. Selecting a plan freeze date that coincides with payroll data and plan benefit calculation periods (e.g., final payroll period for the plan year) may allow future benefit calculations to be more easily addressed and will permit the employer to avoid issues associated with partial payroll and partial year accruals. To the extent that benefit data is readily available at the time of the plan freeze, consideration may also be given to preparing projected service calculations and storing such information for future benefit commencements. In addition, to the extent that there will be a need to track future service (e.g., for early retirement subsidies), consideration may be given to amending the plan to provide for an elapsed time service crediting method so as to avoid the future counting of actual hours of service.

- Plan Notices. The minimum notification standards are defined in Section 4980F of the tax code and

8 Unlike a hard freeze, which would require a timely Section 204(h) notice, there is no formal Section 204(h) notice required for a soft freeze in which no participants are affected. The only individuals affected are new employees who were never participants in the plan and, therefore, have no rights under the plan. 9 10 Many employers provide more details in the Section 204(h) notice, including details on the replacement plan, if any. While this has been a relatively common practice in the past, employers must be mindful of balancing their interest in presenting a positive message with the requirements of 534 F. Supp.2d 288 , 43 EBC 1011 (D. Conn. 2008) (33 PBD, 2/20/08; 35 BPR 469, 2/26/08), aff’d, 47 EBC 2709 (2d Cir. 2009) (192 PBD, 10/7/09; 36 BPR 2352, 10/13/09), vacated and remanded,131 S.Ct 1866 , 50 EBC 2569 (2011)(95 PBD, 5/17/11; 99 PBD, 5/23/11).11 A Section 204(h) notice must be written in a manner that the average plan participant can follow and must include sufficient information to allow applicable individuals to understand the effect of the amendment. This information includes two key components: (i) a narrative description of the amendment including details on the benefit formula prior to the amendment, any remaining pension plan benefits, including the effective date of the amendment, and (ii) sufficient information to determine the approximate magnitude of the reduction. The second requirement is often met by including examples of applicable individuals and a detailed, personal benefit statement or modeling tools that allow employees to see the impact on their own benefit.

- Summary Plan Description. The amendment to freeze benefit accruals is a material modification of the plan and must be reflected in a summary plan description (SPD) or a summary of material modifications (SMM) that is distributed to participants and affected beneficiaries no later than 210 days after the close of the plan year in which the freeze occurs.

12

- Annual Funding Notice. A plan freeze may need to be disclosed as an event having a material effect on assets or liabilities in the annual funding notice. Material events include a plan amendment, scheduled benefit increase, or other known events. Such a freeze is material for the current year if it is projected to result in a change of 5 percent or more in liabilities or assets.

13

Once the Pension Plan Is

Frozen—Now What?

Once the plan has been frozen, the employer’s responsibility for the plan does not end. To the contrary, the frozen plan may actually present new and more challenging issues to address to ensure that the plan continues to remain qualified and does not result in increased financial liability to the employer or additional legal exposure to plan fiduciaries. The freeze period, however, does provide an opportunity for plan fiduciaries to review the plan operations and address any issues of noncompliance.

Ongoing Fiduciary Responsibilities.

While the decision to freeze a plan may be a settlor decision, during the period when a defined benefit plan is frozen, plan fiduciaries must continue to be vigilant with respect to their fiduciary obligations under ERISA. Plan fiduciaries must continue to ensure that the plan, albeit frozen, continues to be administered in accordance with its terms. Moreover, although benefits may cease to accrue under the plan, plan fiduciaries continue to be responsible for ongoing plan investments—the return on which can cause plan funding obligations to continue to increase notwithstanding the cessation of future plan accruals.

Plan Investments.

From an investment standpoint, the new liability structure resulting from the elimination of future accruals with a hard freeze will compel fiduciaries to review and likely shift their investment strategy. For example, the duration of plan liabilities may change, leading to the need for new fixed-income solutions. In addition, the willingness to take equity risk may be reduced to the extent that the plan has a more clearly defined end date, and annuities may become more attractive as the size of the plan decreases.

Investment glide-path strategies where asset allocations change as the plan’s funded status improves may need to be revisited in the investment policy statement or implemented more quickly than before the plan freeze. Typically a frozen plan will look to reduce its riskier equity exposure in turn for more liability-hedging, fixed-income exposure. From the perspective of a plan fiduciary, carefully evaluating investment strategies following a plan freeze can be critical to mitigating risk of asset volatility and potential increases in plan funding requirements notwithstanding the plan freeze.

Plan Accounting.

Once the plan freeze is announced, the employer will likely need to follow curtailment accounting as defined under FASB Accounting Standards Codification 715 (formerly called FAS 88). Under curtailment accounting, some portion of the plan’s unrecognized gains, losses, and plan amendments may need to be recognized immediately in that year’s corporate expense. This amount can be significant and is not generally budgeted, so potential plan accounting issues should be reviewed closely as part of the plan freeze analysis. In the following years, the accounting is quite similar to the pre-freeze methodology except for the reduction or elimination of service cost, which will likely reduce the level of ongoing pension plan expense.

Plan Amendments and Determination Letter Requests.

Although a defined benefit plan may be frozen, the plan must continue to comply with applicable laws from a documentation and operational perspective. Thus, freezing a plan does not take the employer off the hook for monitoring new statutory or regulatory developments. Employers must amend their plan from time to time (similar to plans that are not frozen) to include any plan design changes along with any statutory or regulatory developments,

From a plan document perspective, even though the plan has been frozen (by means of a formal plan amendment), the employer continues to have to maintain the plan’s qualified status, an obligation that will continue until such time as the plan is formally terminated. Thus, for example, the employer may continue to submit the plan for an IRS determination letter

Plan Compliance Reviews.

Assuming the plan has been amended to comply with changes in the law, the freeze period presents a good opportunity for plan fiduciaries to examine the plan operations to confirm that the plan is being operated in accordance with its terms. Invariably, over the years, the plan may have merged or acquired a number of other plans, collective bargaining commitments may have been made with various unions, early retirement and other forms of “window” programs may have been offered, and the plan may have been redesigned, all of which will have resulted in a potential change to the standard operation of the plan.

The benefit of conducting a compliance review during the freeze period is threefold: first, plan fiduciaries continue to have the obligation to ensure that the plan is being administered in accordance with its terms; secondly, the plan is to some degree static and allows for a disciplined review of plan terms and related operations; and thirdly, to the extent that the employer may wish to consider terminating the plan at some time in the future, identifying and addressing any potential issues of noncompliance during the freeze period will permit the plan termination to proceed far more smoothly than if an issue of noncompliance were to arise during the plan termination process.

Missing Plan Participants.

The freeze period represents an opportunity for employers to confirm that they have current contact information for all of the plan participants, particularly those participants who have deferred vested benefits and for whom the employer may not have had any contact with for many years since they left the employer’s employment. Even though a plan is frozen, participants must still commence receiving benefits in accordance with the terms of the plan.

Terminated participants due a benefit should be located prior to normal retirement age to avoid impermissible forfeitures. In addition, plan terminations can often be delayed if the employer is unable to locate deferred vested participants for purposes of offering a lump sum payment or an annuity contract. Thus, to the extent that the employer may consider a plan termination in the future, developing a comprehensive process for locating missing participants during the freeze period is a prudent undertaking and will also pay benefits down the road in terms of timing and avoiding delay in the event of a future plan termination.

Plan Disclosures.

Frozen defined benefit plans must continue to comply with ERISA’s reporting and disclosure requirements. Thus, the plan sponsor should generally assume that most of the reporting and disclosure requirements that apply to an ongoing plan will continue to apply to a frozen plan, e.g., summary plan descriptions, Annual Return/Report (Form 5500), Annual Registration Statement Identifying Separated Participants with Deferred Vested Benefits (IRS Form 8955-SSA), Annual Funding Notices

Nondiscrimination Testing.

Nondiscrimination testing for coverage and benefits is no longer required for a plan that is hard frozen (although it may be prudent to conduct final nondiscrimination testing as of the effective date of the hard freeze). If a plan is not frozen for all participants, however, over time, employers will be challenged by having two classes of employees—one with continued defined benefit accruals and one without. These two populations will need to be tested under the tax code Section 401(a) nondiscrimination rules to ensure that ongoing plan benefits are not biased in favor of highly compensated employees and that a certain minimum number (or percentage) of employees are covered by the plan.

Nondiscrimination issues may arise as the pension-eligible group shrinks and the remaining plan participants become more heavily weighted toward highly paid employees since they are typically longer-service employees.

Cash Outs During the Freeze Period.

To the extent that a defined benefit plan is frozen, the employer may want to consider other possible strategies to reduce plan costs. One approach that has received a fair amount of recent attention relates to amending the frozen (and in many cases ongoing) defined benefit plan to pay lump sums to participants who terminated employment with a vested deferred benefit.

From a financial perspective, such a strategy may serve to limit pension financial and demographic risk exposure; permit liabilities to be settled at a closely matched liability value; reduce future flat-rate PBGC premiums

While plans cannot normally force a participant to take a lump sum payment (other than in situations where the present value of the nonforfeitable accrued benefit is $5,000 or less), there may be situations where amending the plan to offer lump sum payments to former employees who have deferred vested benefits under the plan may make legal and financial sense. The cashout feature requires participant and spousal consent to be paid. In addition, the lump sum can only be offered once an employee has separated from service or the pension plan is terminated; even after a freeze, lump sums cannot be offered in an ongoing plan to current employees.

This “cash out” feature can facilitate a smooth transition in the event that the plan may be terminated in a future year, although commercial annuity providers may view such lump sum payments as resulting in a form of adverse selection with respect to their annuity pricing. This may occur, for example, if the insurers are of the opinion that the “less healthy” participants chose the lump sum, thus leaving the remaining participants for whom commercial annuity contracts may be purchased as having a fairly long life expectancy.

Review of Benefit Calculations.

Once the defined benefit plan has been frozen, there is now an opportunity to circle back and confirm that the data is accurate, frozen plan benefits have been properly calculated, and that all offsets and variable forms of compensation have been properly included (or excluded). Particularly with defined benefit plans that have been converted to cash balance plans, or plans that have had multiple collective bargaining commitments or merged or acquired numerous plans over the years, the freeze period is a great opportunity to review those earlier benefit calculations, or complete calculations for those that were not completed previously (depending on the nature of the freeze).

As a practical matter, complex defined benefit plans can have numerous variables that may be affected by human error, change of plan actuaries or plan administrators, or misinterpretation of plan documents or procedures, all of which can contribute to a miscalculation of benefits and perhaps possible overpayments (or underpayments) in the future.

During the freeze period, employers may wish to resolve historical data issues and conduct sampling of certain plan features or particular transactions to confirm that the plan is being properly administered in accordance with its terms. It would be best for plan fiduciaries to resolve these issues in advance of commencing payments, requesting an IRS determination letter, filing for relief for unrelated issues under the Employee Plans Compliance Resolution System, or beginning the process of terminating the plan.

Review Cost of Plan Termination.

During the freeze period, employers may want to consider the potential cost of terminating the plan at some time in the future. While the plan may (or may not) have sufficient plan assets to presently permit a standard plan termination, it is important that the employer evaluate the plan funding on a plan termination basis. Funding on a plan termination basis can often be quite an eye-opener for employers that may have assumed from recent plan valuations that the plan was overfunded. Funding on a plan termination basis involves some fairly conservative assumptions, including those for interest rates, retirement ages, and mortality. These assumptions, when contrasted with the plan’s normal assumptions, may result in the plan being far less well-funded than the employer may have originally understood.

The degree of funding (or underfunding) on a plan termination basis should be coordinated with the plan investment strategies during the freeze period and ongoing plan funding. While many defined benefit plans may not be sufficiently well-funded to permit a standard termination, coordinating an evaluation of the funded status of the plan on a termination basis along with the strategies described above will position the employer to consider its short- and long-term alternatives for the plan.

Nonqualified Plans.

Freezing a qualified defined benefit plant does not address issues that may arise under an employer’s nonqualified plan (e.g., excess benefit plans or supplemental executive retirement plans). To the extent that the qualified plan is frozen, employers may choose to similarly freeze future accruals under the nonqualified plan, or provide for nonqualified plan benefits to continue to accrue, notwithstanding the cessation of future accruals under the qualified plan. This nonqualified plan “continuing accrual” concept is quite common when the nonqualified plan is simply an excess plan intended to mirror the qualified plan benefits for levels in excess of the pay cap and tax code Section 415 limits.

During the freeze period, employers will want to review their nonqualified plan commitments and coordinate any changes to their nonqualified plan benefits, particularly in situations where the nonqualified benefit plan is offset by benefits payable from the qualified plan, and where the defined contribution plan benefit may have been enhanced due to the loss of the defined benefit plan future accruals. Frozen defined benefit plans also present some interesting accounting implications for nonqualified plans.

Conclusion

While freezing a defined benefit plan may become more popular in the future and make good financial sense for some employers, such a freeze does not preclude the employer from continuing to evaluate plan design, investment, and pre-plan termination strategies for the frozen plan and its assets, nor does it relieve the employer of all ongoing plan administration, costs, compliance, or fiduciary obligations.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.