Introduction, Background, and Explanation of Attachment

As plan administrators and the many service providers to retirement plans covered under the Employee Retirement Income Security Act of 1974, as amended, are finding, there are significant challenges to responding to the revised reporting requirements of Schedule C of the Department of Labor’s Form 5500. These are due principally to the following:

- the unprecedented breadth of the disclosure requested;

- the extreme granularity of the information involved (amounts must be listed across approximately 58 established codes);

- reporting rules that apply to many entities not traditionally subject to ERISA, such as mutual funds registered under the Investment Company Act of 1940, and those private investment funds that limit “benefit plan investor” money to less than 25 percent of each class of equity interests in the fund;

1 This result arguably is inconsistent with Congress’ and the DOL’s general approach to demarcating situations in which look-through treatment is, and is not, appropriate with respect to an ERISA plan’s investment in a pooled vehicle. This is particularly noteworthy because when Congress last considered the rule (in 2006), it effected changes to that rule under the Pension Protection Act. If limiting benefit plan investors to below 25 percent in each class of equity in a private investment fund is sufficient to block any ERISA taint, the strength of the DOL’s position to do the contrary here is uncertain. A similar result (and policy concern) would appear to obtain with respect to registered investment companies under the Investment Company Act of 1940. See also DOL Advisory Opinion 2009-04A. - the interconnected and complex nature of commercial and financial transactions generally, with multiple participants, diverse distribution networks of products and services, and diffuse business models that sometimes frustrate the goal of uniform and compatible reporting and systems.

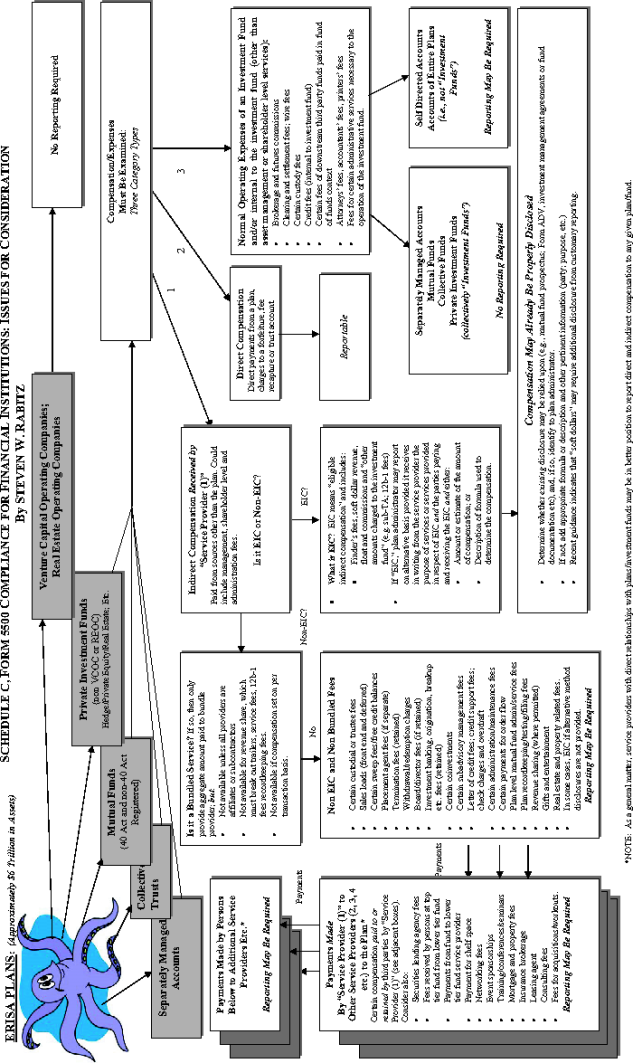

It is no wonder that for many plan administrators and financial services companies, ERISA is beginning to feel like a very large octopus, and that providing the information envisioned by Schedule C may require (to paraphrase Sir Winston Churchill) a good deal of toil, tears, sweat … and ink.

For illustrative purposes, the Attachment to this article provides a visual, hypothetical example of the types of information a large financial institution may need to consider in the context of Schedule C reporting. Because the Attachment is not tailored to any particular product, service, or business, it is by design general in nature. In addition, as the changes to Schedule C are new, a number of interpretations are possible as a result of continuing uncertainty of these requirements as applied to service providers. Nevertheless, it may prove to be a helpful starting point for those service providers trying to grasp the totality of the mission at hand. The reality, unfortunately, may be even more complex for many institutions.

Currently Effective: Breadth and Depth

Overview.

The revised Schedule C rules were promulgated in 2007 by the U.S. Department of Labor and become effective for the 2009 plan year for ERISA plans with over 100 participants. The rules will also affect service providers receiving, directly or indirectly, $5,000 or more in reportable compensation during the applicable reporting year. This means that for most calendar year plans, filings will be due at the end of July 2010. There is anecdotal evidence suggesting that requests for information are already accelerating and many plan officials, administrators and financial services companies are doing their best to comply with the sea change in reporting burdens.

To appreciate the level of detail that is required by the revised rules, consider that the DOL expressly refers to items such as “float” (including, presumably, transaction float), 12b-1 fees, soft dollar payments, and commissions. Banking, consulting, recordkeeping, wire transfer, check overdraft, other common “third party administrator” fees, and revenue sharing (where permitted) are other elements of a potentially large (and nonexclusive) list of reportable items. In some instances, a specific dollar amount (i.e., not a formula or estimate) may be required.

Although experience suggests that most financial institutions genuinely seek to comply with all legal and regulatory requirements, the rules provide two incentives to do so, even where, as here, the technical obligation is imposed on the plan’s administrator:

- An administrator generally is required to notify the Labor Department of the identity of any service provider that fails to provide the requisite information.

2 The DOL has indicated for the 2009 plan year that it will not enforce this provision to the extent that a service provider gives the plan administrator a statement to the effect that despite good faith efforts, the service provider was unable to timely make recordkeeping changes to meet the challenges of proper reporting.

- Failure to provide such information carries with it the very real commercial possibility that an ERISA plan will limit or terminate its involvement with that service provider.

3 A fiduciary’s decision to select and maintain a relationship with a given service provider is based on a variety of factors. Fiduciaries typically discharge their duties of prudence in evaluating any given relationship with the plan in its totality. As a general matter, it is difficult to see how a fiduciary would be acting solely in the best interest of plan participants and beneficiaries by terminating an otherwise productive relationship for the plan solely on the basis of any minor failure to provide some of the more granular information contemplated by Schedule C.

Categories of Reportable Compensation

Amounts required to be reported under the revised rules fall into three general buckets:

Direct Compensation.

“Direct compensation” is, in essence, the compensation paid to a service provider directly by a plan. Direct compensation includes direct payments from a plan, charges to a plan’s forfeiture or recapture account and charges to a participant’s account or trust account.

Indirect Compensation.

“Indirect compensation” is any compensation that is paid to a service provider but not directly by the plan, if the compensation is received in connection with a person’s position with the plan or for services rendered to the plan, and the person’s eligibility for a payment or the amount of the payment is based, in whole or in part, on services that were rendered to the plan or on a transaction or series of transactions with the plan.

For example, where a plan administrator is paid for recordkeeping services through 12b-1 fees or other compensation from an investment option offered under the plan, that payment would constitute indirect compensation. Other examples of indirect compensation include finders’ fees, revenue sharing, 12b-1 fees, sub transfer fees, soft dollar services and gifts and entertainment.

The DOL notes that indirect compensation

… includes, among other things, payment of ‘finder’s fees’ or other fees and commissions by a service provider to an independent agent or employee for a transaction or service involving the plan. Thus, commissions received from a person, other than those received directly from the plan or plan sponsor, in connection with the sale of an investment, product, or service to a plan would be reportable indirect compensation. The treatment of the commission as reportable indirect compensation is not dependent on whether the seller or the agent has any other relationship to the plan other than the sale itself.

Eligible Indirect Compensation.

“Eligible indirect compensation” is a subset of “indirect compensation” that may be reported to the DOL under a somewhat more flexible regime if the plan administrator receives written disclosure of:

- the existence of the eligible indirect compensation;

- the service provided for the eligible indirect compensation;

- the amount or estimate of the compensation or a description of the formula used to calculate the eligible indirect compensation; and

- the identity of the parties paying and receiving the eligible indirect compensation.

Eligible indirect compensation includes amounts that (i) are paid or charged to an account subject to the reporting rules and (ii) are reflected in the value of the plan’s investment, such as asset based management fees, finders’ fees, soft dollar revenue, 12b-1 fees, float, and other transaction based fees reflected in the investment of the participating plan, and which are not deemed “operating expenses” of an investment fund. The terms “operating expense” and “investment fund” are both key toward a proper understanding of Schedule C.

According to the DOL,

[a]mounts charged against the fund for … ordinary operating expenses, such as attorneys’ fees, accountants’ fees, printers’ fees, are not reportable indirect compensation for Schedule C purposes. Also, brokerage costs associated with a broker-dealer effecting securities transactions within the portfolio of a mutual fund or for the portfolio of an investment fund that holds “plan assets” for ERISA purposes, should be treated for Schedule C purposes as an operating expense of the investment fund not reportable indirect compensation paid to a plan service provider or in connection with a transaction with the plan. [Emphasis supplied]

This exception for “operating expenses” is potentially very helpful, insofar as it applies to an “investment fund.” The term “investment fund” includes both vehicles such as mutual funds, private investment funds, and bank collective vehicles in which multiple parties invest, and “separately managed investment accounts that contain assets of an individual plan.”

Mutual Funds, Below 25 Percent Funds

One of the most controversial aspects of the revised Schedule C rules is that it covers entities not traditionally subject to ERISA. Perhaps no other aspect of the revised rule more evidences Schedule C’s tentacle-like approach to the unsuspecting, and mutual fund complexes and hedge fund advisors would be well advised to pay close attention. Recent guidance indicates that among the entities covered by the revised Schedule C compensation reporting requirements are:

… registered investment companies (commonly referred to as mutual funds) … and other investment funds that do not hold “plan assets”. . . . Thus, for instance, fees paid to persons for management of a real estate hedge fund that [was not subject to the fiduciary responsibility provisions of ERISA because it limited benefit plan investor participation to below 25 percent of each class of equity interests] would be reportable Schedule C compensation, but property management fees paid to persons managing the underlying properties owned by the funds could be treated as ordinary operating expenses of the fund.

For many investment vehicles, such as mutual funds, bank collective funds, “below 25 percent” hedge funds, real estate investment trusts, and separately managed accounts and insurance company pooled separate accounts, this means that the investment vehicle will need to monitor amounts charged against the value of the fund or account or that are reflected in the value of the plan’s investment.

Operational and Interpretative Challenges

Even where an item may qualify for the alternate reporting regime of eligible indirect compensation, service providers may find themselves having to provide more information than the Securities and Exchange Commission or other regulators traditionally have required. For example, with respect to soft dollars, the DOL recently noted that “[i]f the disclosures that meet the securities laws’ requirements do not include the information necessary to meet the eligible indirect reporting option, additional disclosures would be required for a plan to take advantage of the alternative reporting option for eligible indirect compensation.”

Given the complexity of many commercial relationships, with many unaffiliated companies often involved in the product and service distribution chain, reporting can often be intricate and involved. For example, the DOL describes the following situation:

A mutual fund pays eligible indirect compensation to a fund administrator, advisor, or distributor (a “fund agent”). In turn, the fund agent pays fees to the recordkeeper for “compliance services” provided to one or more participating plans, including discrimination testing, QDRO administration, and Form 5500 preparation. The recordkeeper is not an affiliate of the mutual fund or the fund agent.

With respect to that example, the DOL asks whether the mutual fund payment to the recordkeeper is reportable indirect compensation, and if so, whether the fee received by the recordkeeper is eligible indirect compensation.

Plan recordkeepers may receive fees for shareholder services and recordkeeping services directly or indirectly from investment providers under a wide variety of arrangements. Among others, they may receive compensation from fund agents (such as fund administrators, advisers or distributors) as well as other agents, representatives or intermediaries such as mutual fund “platform” providers, broker-dealers, banks, and insurance companies. The fees for compliance services received by the recordkeeper from the mutual fund agent are reportable indirect compensation. The alternative reporting option for eligible indirect compensation would not apply to such payments because the payments are not among the categories listed in the Schedule C instructions for eligible indirect compensation… . . Amounts received by a plan recordkeeper from fund agents would not constitute eligible indirect compensation … .[emphasis supplied]

Another potential hurdle is that each entity in the distribution chain and may have different ways of recording, capturing, and maintaining any information that may be requested under Schedule C. For example, assume that a recordkeeper enters into an “alliance” arrangement with an independent broker-dealer to provide services offered together as a “package” sold by agents of the broker-dealer under separate contracts or arrangements with the plan. Assume further that in connection with this alliance arrangement, the broker-dealer pays compensation to the recordkeeper on either a flat per-participant fee basis or an asset-based fee basis on the value of plans’ investments in mutual funds or other investment vehicles offered to the plans by the broker-dealer.

In such an arrangement (which is not uncommon), the broker-dealer might pay the compensation for plan administration and recordkeeping services the recordkeeper provides to the broker-dealer’s plan clients. According to the DOL’s guidance, compensation paid by the broker-dealer to the recordkeeper is indirect compensation.

The DOL’s answer to that question is “Not necessarily.” The DOL explained:

One purpose of the Schedule C reporting structure is to provide plan fiduciaries with better information regarding the flow of amounts that represent fees received in connection with services provided to the plan. Accordingly, it is possible that a person could receive a fee that would constitute indirect compensation and pass some of that fee on to another person for whom the amount passed on would also represent reportable indirect compensation. In such a case, the information reported regarding the first and second person who received the fee could include a description of the total fee received and the portion of the fee passed on to the next level recipient. Alternatively, it may be that the consolidated bundled fee reporting option could be used instead of reporting revenue sharing compensation received by individual members of the bundle. On the other hand, if an intermediary fund agent is merely a conduit for transmission of the revenue sharing fee to the ultimate recipient, the conduit would not itself be receiving any reportable compensation by acting as the conduit.

Because an administrator generally must look to a plan’s service providers (broker-dealers, investment managers, custodians, third-party administrators, record keepers, etc.) to obtain the requisite information, many financial services companies have been developing and implementing systems to provide the data that will be required. But it has not been, and will not be, easy, and the costs involved often have been (and are likely to continue to be) staggering, particularly where different chains of unaffiliated entities are involved. Broker-dealers, trustees, custodians, recordkeepers, transfer agents, and many other financial market participants have a lot to digest here.

More fundamentally, of course, aside from even these considerations is the question of when an ERISA plan may be a customer or consumer of any given product or service. For example, many asset managers often deal with counter-parties and service providers with respect to their total assets under management without identifying the underlying clients involved. The question has important implications. Unfortunately, DOL has not provided an unambiguous answer for all facts and circumstances.

Gifts, Gratuities, and Entertainment as Reportable Indirect Compensation

DOL believes that gifts, gratuities, and entertainment may be forms of reportable indirect compensation. In general, all amounts of gifts, entertainment, and other gratuities paid to or provided in respect of the plan’s assets need to be reported, unless the aggregate amount of such gifts and gratuities received by a service provider with respect to the plan is less than $100 per year provided each gift or gratuity is less than $50 (ignoring in some cases items that are less than $10 for purposes of this test).

To illustrate the level of detail the DOL has in mind, consider that it has expressly highlighted items such as “coffee mugs,” “calendars,” “greeting cards,” “plaques,” “certificates,” “trophies,” and “similar items …displaying a company logo,” any of which may, at least for reporting purposes, be viewed as presumptively de minimis, (because their value is likely less than $10)

All of this would be difficult enough if one were dealing solely with ERISA plans. But life being what it is, financial services relationships are not always segregated between ERISA and non-ERISA business. Consider the following question posed by DOL with respect to gifts, gratuities, and entertainment that involve multiple “end” clients: “If a person providing services to the plan is provided a meal or other entertainment based on a general business relationship that includes both ERISA and non-ERISA business, is it required to be reported on the Schedule C?”

The DOL’s answer? “It depends,” as explained in the following DOL guidance:

The Schedule C instructions state that indirect compensation would not include compensation that would have been received had the service not been rendered to the plan or the transaction had not taken place with the plan and that cannot be reasonably allocated to the service(s) performed or transaction(s) with the plan. However, if a person’s eligibility for receipt of a gift (such as meals, travel, or entertainment) is based, in whole or in part, on the value (e.g., assets under management, contract amounts, premiums) of contracts, policies, or transactions (or classes thereof) placed with ERISA plans, the gift would constitute reportable indirect compensation for Schedule C purposes.

Similarly, available DOL guidance asks the following in the context of business conferences at which, say, a plan sponsor, investment manager, trustee, or custodian may be an invited participant:

For Schedule C reporting purposes, where a service provider has received free attendance at a conference or seminar that constitutes reportable indirect compensation, is it adequate to report payments for meals, hotel, transportation costs, and other individual expenses? Must the plan administrator also report that portion of the expenses attributable to every conference attendee for costs such as guest speaker fees and other conference overhead?

The answer, according to DOL guidance, is as follows:

Waiver of any conference registration fee would also be reportable indirect compensation. Conference overhead expenses, such as guest speaker fees, conference space rental, continental breakfast and other refreshment expenses normally included in the cost of the conference registration fee, are not reportable indirect compensation for Schedule C reporting purposes.

Independent of all of the above, the DOL has indicated on numerous occasions that the guidance given in respect of the reporting on gifts and entertainment is just that: guidance on reporting. Service providers need to continue to think about the more basic question as to the permissibility of gifts, gratuities, or entertainment to persons dealing in plan assets in the first place. Indeed, in several places, the DOL notes:

CAUTION …Filers are strongly cautioned that gifts and gratuities of any amount paid to or received by plan fiduciaries may violate ERISA and give rise to civil and criminal penalties.

Given the detail and granularity of DOL’s guidance, its posture regarding gifts and entertainment,

That said, even where service providers try in earnest to comply with the DOL’s reporting requirements and to be responsive to its sensitivities concerning gifts and entertainment, the many intricacies and hurdles can be difficult to overcome. How, for example, does an institution with separate business lines with different points of contact with any given client— and where, for a variety of reasons, these business units have no reason to talk to one another for regulatory purposes—develop and implement company-wide systems to aggregate potential items of gifts and entertainment for purposes of the reporting rules under Form 5500, and if applicable, to assure compliance with the de minimis limits?

That question, and the myriad permutations that flow from it, are particularly difficult to answer when one considers that in “real life,” many institutions deal with “undisclosed” or “omnibus” accounts, which often make tracking and/or good faith compliance with either the Schedule C reporting rules or good faith attempts to adopt reasonable dollar limits difficult. Managing these tasks for clients such as mutual funds or hedge funds, which may have “undisclosed” ERISA money, adds even more complexity.

Conclusions

In sum, the revised Schedule C reporting rules present daunting challenges. There is good reason for one to view the revised rules under Schedule C as the proverbial octopus: reaching not only those accounts that have always been subject to ERISA, but many of those that have not. Moreover, the power of that reach must be considered in the context of the potential granularity of the information to be provided, the interconnectivity of market participants and service providers in legitimate product distribution, and the fact that much of the information being required to be reported has not been so required previously.

One wonders, however, whether the extraordinary additional toil, tears, sweat … and ink that will be expended to comply fully and accurately with these new disclosure requirements will result in significantly improved disclosure to plan fiduciaries – disclosure that will enable them to make materially better evaluative judgments for the plans they serve. Or, as some fear, will the deluge of additional information merely result in so many information “trees” that the fiduciaries serving the plans will be unable to see, as it were, the forest.

Time will tell. For now, many plan administrators and service providers find themselves swimming in the same ocean, responding in their own way to this new regulatory creature that compels their attention.

Attachment

Steven W. Rabitz’s chart outlining hypothetical situations under Schedule C appears on the following page. The Attachment also may be viewed at: Attachment or http://op.bna.com/pen.nsf/r?Open=foln-84sse9.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.