Every state has a lost-and-found where it collects property that has been left behind, and possibly forgotten, by its owners. Last year, states’ unclaimed property funds held almost $42 billion—and some of that money came from retirement accounts.

A 2010 ING Direct survey found that one-half of American adults have left money behind in employer-sponsored retirement plans when they change jobs. Remarkably, almost one-in-five left $50,000 or more.

While there are may be many reasons that employees choose this course of action, the top five explanations are:

- It’s the easiest course of action.

- Employees are unaware they have money in the plan, or forget they do.

- Employees don’t have a meaningful amount of money in the plan.

- A contribution is made to the former employees’ account from a final paycheck.

- It’s believed to be less expensive to invest through the plan, than other options.

No matter the reason, it’s important to stay in touch with a former employer when retirement savings are left behind. All too often, former employees become missing plan participants. Perhaps, they move and forget to provide a forwarding address. Maybe, they fail to respond to correspondence. No matter how it happens, the number of missing plan participants has been increasing.

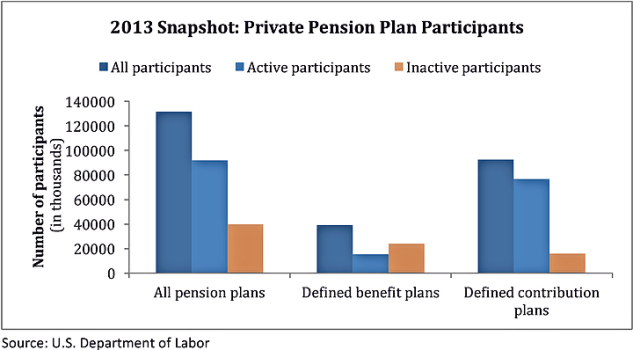

It’s difficult to quantify exactly how many missing participants there are in the United States. The most recent data from the U.S. Department of Labor (DOL) indicates there were about 132 million plan participants across the United States in 2013. They had almost $8 trillion invested in retirement plans. Almost one of every three participants was inactive. While not all inactive participants are missing participants, a significant percentage may be—like 15% to 20%—and that’s where the trouble starts for the plan sponsor and the participant.

Typically, savings in 401(k), pension, profit sharing, and other qualified employer-sponsored plans cannot be claimed under states’ unclaimed property laws because the Employee Retirement Income Security Act of 1974 (ERISA), a law requiring plan sponsors to act prudently and solely in the interest of plan participants and beneficiaries, preempts state laws.

When plan participants go missing, most plan sponsors have a well-defined process for former employees’ accounts. If a retirement plan is active, the sponsor may:

- Maintain missing participants’ accounts, which could become expensive for plan sponsors and active participants.

- Search for the missing participants, find out how they would like their assets distributed, and follow their instructions.

- Roll over accounts with $5,000 or less to an automatic rollover individual retirement account (IRA). (This is the Department of Labor’s preferred option.)

- Roll over a missing or unresponsive participant’s assets (after withholdings) to an interest-bearing bank account, like a certificate of deposit or savings account.

The rules are a bit different for plan sponsors who are terminating their retirement plans. If a plan is closing:

- Missing participants’ assets may be sent to a state’s unclaimed property department. If it happens, taxes are withheld from the amount distributed.

- Search for the missing participants, find out how they would like their assets distributed, and follow their instructions.

- Roll over accounts of any size to an automatic rollover IRA. (This is the Department of Labor’s preferred option.)

- Roll over a missing or unresponsive participant’s assets (after withholdings) to an interest-bearing bank account, like a certificate of deposit or savings account.

To regain control of these assets from a given state’s unclaimed property department, account owners or their beneficiaries must prove ownership. This can be done at any time, in most states, no matter how many years have passed. However, in the meantime, the account has neither earned interest nor had the opportunity to gain through investment.

Unclaimed Property Laws

Unclaimed property laws originally were put in place to protect property and return it to its rightful owners. The laws ensure that unclaimed property is turned over to the state after a certain period of time.

Unclaimed property covers a lot of territory. It includes tangible and intangible assets, such as:

- Bank, brokerage and mutual fund accounts

- Stocks and bonds

- Trust distributions

- Insurance payments or refunds

- Life insurance policies

- Annuities

- Certificates of deposit

- Safety deposit box contents, and

- Other types of assets

Typically, if an account holder cannot find the account owner, unclaimed property escheats, meaning it becomes the state’s legal property. Some states allow owners to claim their property at any time, even after it has been escheated. Others, such as Hawaii, Indiana, and New Hampshire, permanently transfer unclaimed property to the state after a period of time.

From an accounting standpoint, unclaimed property funds are recorded as state revenue, and can be used by states to balance their budgets. In recent years, some states have shortened dormancy periods, so assets can be claimed sooner, and some have hired contingent-fee auditors to seek unclaimed property. Often an auditor will work on behalf of 20 to 30 states simultaneously.

Supreme Court Justices Samuel Alito and Clarence Thomas recently offered a concurring opinion deriding states’ tendency to disregard the importance of finding property owners.

“In recent years, States have shortened the periods during which property must lie dormant before being labeled abandoned and subject to seizure…This trend—combining shortened escheat periods with minimal notification procedures—raises important due process concerns,” Alito wrote. “As advances in technology make it easier and easier to identify and locate property owners, many states appear to be doing less and less to meet their constitutional obligation to provide adequate notice before escheating private property. Cash-strapped states undoubtedly have a real interest in taking advantage of truly abandoned property to shore up state budgets. But they also have an obligation to return property when its owner can be located.”

In 2011, the National Association of Unclaimed Property Administrators reported that only about 5% of almost $44 billion of unclaimed property was returned to owners by states. Of course, some states have better track records than others.

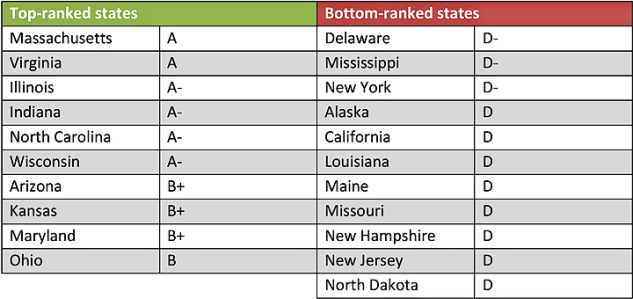

The Council On State Taxation (COST) issued its most recent scorecard on unclaimed state property statutes in 2013. A high grade indicates the state program seeks to unite owners with their property in the manner that is least burdensome to owners, holders and the state.

Delaware expects to claim more than $500 million in property this year and next year.

As the incorporation capital of the United States, the state benefits from priority rules, which indicate the state shown on the owner’s last-known address has the first right to claim property. If the property holder does not have an address for the owner, then the state of the holder’s domicile has the right to claim the property.

Non-Qualified Retirement Assets

If investors have retirement savings in non-ERISA accounts, such as a traditional IRAs, Roth IRAs, SEP or SIMPLE IRAs, or 403(b) plans, then these custodians should mark their calendars so they don’t forget to check in with the account holder each year.

States’ interest in these assets has been increasing, in part, because of the significant amount of money invested in these accounts. The good news is that IRAs are not considered unclaimed property, in most states, until the missing owner reaches age 70

That said, experts report that a few states have established IRA provisions in their unclaimed property statutes. For example, in Oregon, an IRA must be turned over to the state if the account holder has determined the owner is deceased and cannot distribute the assets to the beneficiaries.

Pennsylvania passed a bill that allows a Roth IRA to be claimed by the state three years after the owner reaches age 70

Find and Claim Your Retirement Assets

It’s important to keep track of your retirement savings, and any other unclaimed property that may belong to you. Here are three steps that can help you reclaim any assets that have gone missing.

- Contact former employers. Ask whether you had an account in their retirement savings plan. If you did, determine where the money is now.

- Search for unclaimed property. Visit websites like Missingmoney.com, unclaimed.org, and mtrustcompany.com/unclaimed-retirement-funds, and search unclaimed property lists.

- Seek missing pension assets. The Pension Benefit Guaranty Corporation maintains a list of unclaimed pensions on its website at http://www.pbgc.gov.

Don’t wait until you’re on the cusp of retirement to make sure you know where your retirement money is. If you know where your money is, make sure you stay in touch with the companies where you’ve invested it.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.