As employers throughout the country wrestle with the increasing costs and expenses of operating their businesses, pension plan sponsors continue to focus their attention on their defined benefit plans. Of particular concern to defined benefit plan sponsors is the financial volatility associated with the plan, along with the increasing legal and fiduciary risks that accompany managing what may be substantial liabilities.

This article discusses how best to identify these risks, and to evaluate possible strategies to mitigate them.

Pension Environment Today

Due to financial volatility, the evolving needs of the workforce, and the challenging legal and regulatory environment, few new defined benefit plans are being established today. Moreover, existing defined benefit plans are being scaled back or frozen and, as interest rates improve, may be terminated with increasing frequency.

While plan termination may be the ultimate solution for some employers, such a step can prove to be quite expensive, in particular for plans that are underfunded. Many employers that have evaluated plan termination alternatives have discovered that they may not be as well-positioned financially to terminate their plans as they may have thought. The actuarial assumptions and reserve and profit requirements reflected in insurance company annuity pricing for a plan termination generally result in a premium that is greater than the liability held by the plan sponsor for accounting and funding purposes. These factors can be expected to increase the amount of any underfunding and may result in the employer incurring significant cash funding requirements to terminate the plan. While plan termination remains an option for many of the better-funded plans, there are a number of strategic opportunities available to employers that may mitigate their legal and financial risks while continuing to permit them to maintain their plan.

Financial Liabilities Impacting Pension Plans

Pension plans present significant financial challenges for employers. Pension obligations, or the value of pension promises recorded on the financial statements of pension plan sponsors, have experienced tremendous growth during the past decade. This dramatic increase is primarily due to falling interest rates. For Standard & Poor’s 500 companies, for example, the aggregate value of pension obligations since the end of 2006 has grown by nearly 20 percent, from $1.45 trillion to $1.72 trillion. When coupled with modest asset returns during the same period, the average pension plan deficit (the excess of pension obligations over the value of plan assets) has increased by a little more than $300 billion, from $42 billion to $361 billion.

For many employers today, the defined benefit pension obligations that are reported on their financial statements can be particularly volatile and highly susceptible to swings in interest rates. This volatility can adversely impact the employer’s ability to obtain required financing and may impact the employer’s cash flow profile. Moreover, to the extent that the employer does not maintain pension funding levels of at least 80 percent, the employer may find that its ability to modify the plan in certain ways is limited and, depending on the funding level, may find that it must restrict the ability of participants to receive lump sums and other accelerated payment options.

Developing Legal and Financial Strategies

To Mitigate Pension Risks—Roles

Pension plan sponsorship brings with it a host of settlor and fiduciary obligations—both legal and financial. From the standpoint of the plan sponsor, decisions relating to the establishment, design, and termination of plans are viewed as settlor (nonfiduciary) functions rather than fiduciary activities governed by the Employee Retirement Income Security Act. Thus, plan sponsors may act in the best interest of the employer and its owners/shareholders when deciding whether to sponsor, redesign, freeze, or terminate their defined benefit plans. Activities undertaken to implement these decisions, however, generally are fiduciary in nature and must be carried out in accordance with ERISA’s fiduciary provisions.

Pension Risk Management—

Strategies for Consideration

Pension risk can take many forms and can include strategic, financial, interest rate, investment, longevity, regulatory, legal, and compliance risks. In response to these risks, risk management has moved to the forefront as one of the primary areas of concern for many pension plan sponsors. While there are a number of alternatives that may be considered to mitigate financial and legal pension risks, we will evaluate several of the more significant strategies, short of a standard plan termination, that employers should consider. These strategies can include benefit design, restructuring of investments, lump-sum payments, and group annuity contracts designed to reduce the potential for volatility in pension plan liabilities and the risk of adverse claims or litigation.

- Benefit Design Strategies: One strategy for mitigating the risks associated with increasing pension plan liabilities is to reduce the size of the liability. There are a variety of options to consider to achieve this objective, the first of which is often to modify the plan design. Making changes to the underlying plan design was the most popular response to the first so-called perfect storm of falling equity markets and falling interest rates that occurred during the period 2000 to 2002. Among the design alternatives frequently considered are to close the plan to new entrants, to freeze future accruals in the plan for all or a portion of the population (e.g., existing participants, certain nonunion populations, or new entrants), or to consider other changes to the plan formula such as converting to a cash balance plan or reducing the plan’s early retirement subsidies.

4 Due to the mature status of many pension plans and the fact that benefits already earned are generally protected and cannot be reduced or eliminated, changes in benefit design have a limited impact in terms of reducing plan obligations during the near term. See, e.g. 5 Aon Hewitt Survey of Fortune 500 Companies with Closed, Frozen or Terminated Pension Plans (2012). - Investment Strategies: From an ERISA fiduciary perspective, the plan fiduciaries are charged with investing plan assets in a prudent manner so as to have sufficient assets to meet the pension benefit obligations provided for under the plan. To the extent that the plan fiduciaries choose investments that perform poorly, despite prudently evaluating plan investment alternatives, the plan sponsor must make up any investment shortfall to have sufficient assets to meet its pension and plan funding obligations. By sponsoring a defined benefit plan, the employer has made a commitment to provide a particular retirement benefit to participants based on a number of factors including compensation and years of service—the risk that plan investments will perform better or worse than expected rests with the employer.

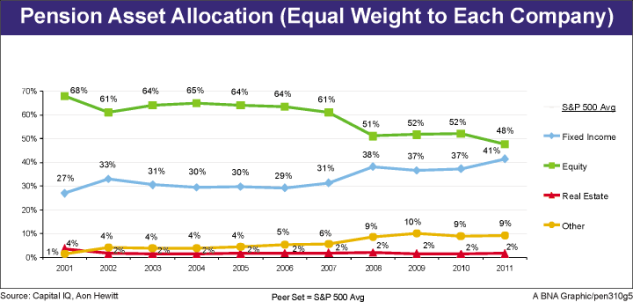

Pension plans historically were managed as a long-term commitment and, as such, the investment strategies in place were designed to provide optimal levels of returns during complete market cycles, typically resulting in portfolios with heavy allocations toward equities and other similar investments. A by-product of this approach was a high risk, high volatility portfolio with a significant asset-liability mismatch,

- Change in Pension Investment Strategy: Due to the maturation of pension plans, the shift toward closed and frozen plans, volatile capital markets, and the regulatory shift toward mark-to-market accounting

7 Mark-to-market accounting refers to the method of reflecting pension assets and liabilities at their market value, versus book value or a method that reflects long-term actuarial smoothing techniques. The most notable manifestation of mark-to-market accounting for pensions is the valuation of liabilities based on current market interest rates.

While this trend in asset allocation has continued to develop, with only 41 percent of pension plan assets allocated to fixed income on average, and more than 50 percent of plan assets still allocated to equity and alternative investments (generally hedge funds and private equity), significant risks remain with the investment strategies in place for many pension plans.

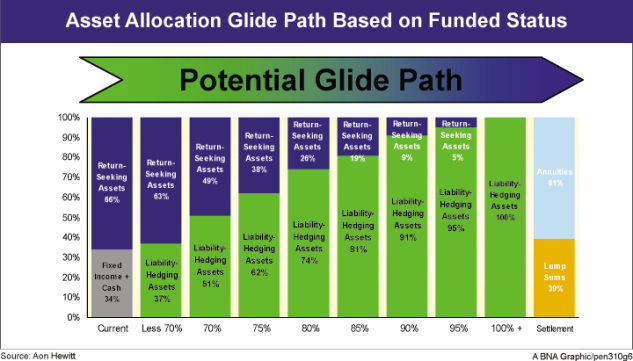

- Development of a Glide Path: For a variety of reasons, many plan sponsors conclude that continuing to take pension investment risk in the near term makes sense. Reasons vary from concern about the low level of interest rates and the resulting high level of bond prices, to the underfunded nature of many plans and the higher investment returns that are necessary to solve their pension underfunding problem. A preferred investment strategy that has emerged in response to these concerns is what is commonly referred to as a “glide path” approach. A glide path strategy, simply stated, reduces a pension plan’s risk by systematically shifting the investments away from equity and other return-seeking investments toward fixed income investments as the funded status of the plan improves. A typical glide path strategy is illustrated in the exhibit below:

A glide path strategy addresses many of the concerns that plan fiduciaries often encounter when considering de-risking plan investments, and results in a favorable buy low, sell-high discipline, as the assets being sold (e.g., equities) in response to funded status improvements have often just appreciated in value, and the assets being purchased (e.g., bonds) have often just depreciated in value (due to rising interest rates). As a result, this strategy has been followed with increasing frequency. Since 2007, based on an Aon Hewitt survey of corporate clients, the number of pension plan fiduciaries adopting a glide path approach has increased twelvefold, from 5 percent to 60 percent.

- ERISA Fiduciary Concerns:

The adjustment of a pension plan’s investment policy requires careful consideration as to what may be in the best interest of plan participants. At the same time, it is difficult to separate participant interests from the impact such investment policy may have on the plan sponsor. Guidance from the Department of Labor indicates that such a balance may be struck without running afoul of plan fiduciaries’ obligations to plan participants.

- Lump- Sum Strategies: Another effective risk mitigation strategy is to essentially reduce the size of the pension plan, typically through the settlement of a portion of the plan’s liabilities. While liability settlements can take a variety of forms, an approach that has seen tremendous activity of late is the payment of lump sums to participants. This strategy typically involves employers amending their pension plans to offer a temporary lump-sum payment option to terminated vested employees and beneficiaries who have not yet commenced their pension payments. More recently, this concept has been extended to retired employees who are already in payment status. The terminated vested and retired employees are the populations for whom the pension obligations often represent the most significant portion of the defined benefit plan liability. This strategy, if implemented, would permit the eligible participant (or beneficiary) to take a lump-sum equivalent payment in exchange for foregoing the right to his or her future annuity benefit under the plan.

- Financial Considerations: The ability to offer lump sums is an option that has existed for many years and is quite prevalent, in particular with hybrid plan designs such as cash balance plans. However, the popularity of offering lump sums increased significantly in 2012 due to changes in the minimum interest rates used in the lump-sum conversion factors as required by the Pension Protection Act (PPA).

9 109 P.L. 280 (Aug. 17, 2006). Previously, lump sums were required to be calculated using 30-year Treasury interest rates, while pension liabilities were measured using (higher) corporate bond rates. As an example, this meant that the settlement of an annuity with a liability of $100 would require a lump-sum payment ranging from $110 to $125, which generated a loss to the pension plan of $10 to $25. The PPA updated the minimum interest rate to be used for calculating lump sums to the corporate bond rate, generally the same rate used to measure the liability under the plan, so that a liability of $100 could be settled for a cash payment of approximately $100. This change was phased in during a five-year period, with full phase-in occurring in 2012. - Mortality Tables: The minimum lump-sum basis described above also includes a mandated mortality table. While the true economic liability will ultimately depend on the actual longevity experience of the population of the specific plan in question, future updates to required mortality assumptions are generally expected to result in longer life expectancies and result in higher pension liabilities. The payment of lump sums before these mortality table updates take effect can be another source of benefit to plan sponsors considering a lump-sum offering.

- Financial Considerations: The ability to offer lump sums is an option that has existed for many years and is quite prevalent, in particular with hybrid plan designs such as cash balance plans. However, the popularity of offering lump sums increased significantly in 2012 due to changes in the minimum interest rates used in the lump-sum conversion factors as required by the Pension Protection Act (PPA).

In evaluating the financial aspects associated with the payment of lump sums, there is more to consider than simply the interest rate and mortality table to be used. Usually, the lump sum offered to plan participants is the present value of the accrued benefit payable at normal retirement, typically at age 65. Plan sponsors must consider the true economic liability associated with this promise–what total cost does the plan sponsor expect to incur during the life of the payments to be made to the participant. In addition to the present value of the benefit, the economic cost of continuing to pay the participant’s pension benefit in the future should factor in future administrative costs and PBGC premiums associated with providing pension plan payments, the cost of which is not included in the lump-sum payment. To the extent the plan provides for payment of the accrued benefit at an earlier age on a subsidized basis, payment of a lump sum based on the age 65 benefit may provide an additional source of savings.

It is also noteworthy that, in certain instances, if the liability settled is sufficiently large, the event can trigger settlement accounting.

- Lump-Sum Payments–Issues and Considerations:

While the offer of a lump sum benefit may be financially very compelling for some employers, there are a number of design, administrative, and compliance-related issues that will need to be considered and addressed.

- Terminated Vested Employees: Terminated vested employees are widely regarded as the most attractive group to whom a lump-sum window should be offered. This group is most attractive because they have yet to begin to receive their pension, they tend to exhibit a high lump-sum election rate and often have smaller pension benefits deferred many years into the future. Thus, the fixed-dollar administrative costs and PBGC premiums for this group are greatest relative to the size of the pension obligation. Moreover, it is this group that may be viewed as having a limited ongoing connection to their former employer and for whom the offer of a lump sum may be most attractive.

- Retirees in Payment Status: For many years, the traditional view had suggested that a defined benefit plan may only offer a lump-sum distribution of the entire remaining accrued benefit to a retiree currently in pay status under certain very limited situations (e.g., upon a plan termination).

12

The traditional view, however, was apparently not the view of the Internal Revenue Service. In two private letter rulings issued in 2012,

• Miscellaneous Issues: Additional issues to be considered in connection with the lump-sum feature include addressing spousal consent,

- Group Annuity Settlement Strategies: The primary drawback with offering lump sums is that the plan sponsor has limited control over how much of the plan is actually settled, as this will depend on the percentage of participants who elect to take the lump sum. Lump-sum election rates tend to fall in the 40 percent to 60 percent range for terminated vested populations, with lower rates for current retirees. The purchase of a group annuity contract, however, under which the liabilities and supporting assets associated with some or all of the benefits under the pension plan are transferred to a third-party insurance company, allows the plan sponsor to control the amount of assets and liabilities that are settled. For example, a group annuity contract can be purchased for the entire participant population of a plan or a subset of that group, and would be required for all participants as part of a plan termination (absent a lump-sum payment to the participant).

- Financial Considerations: Annuities provide the greatest degree of certainty with respect to the amount of risk reduction, as once the pension plan obligations are properly transferred to the insurer, they are no longer the responsibility of the plan. However, there is a cost for this added degree of certainty. Typically the price of an annuity contract will exceed the accounting liability recorded on a plan sponsor’s balance sheet, at times by a significant amount. Unlike lump-sum payments to participants, which allow for settlement excluding the cost of administrative expenses, risk premiums (in the form of PBGC premiums), and mortality table updates—insurance companies’ group annuity premium costs may generally include a margin for many of these items.

Group annuity insurers must also use a liability discount rate reflective of the rate of return that can be achieved by the insurer on the assets once invested. Not only do insurers typically look to the returns available on investment-grade fixed income, they also must build in the effects of downgrades and defaults on those returns over time. This tends to result in the use of a lower discount rate, and hence a higher pension liability than is reflected in corporate financial statements. Altogether, annuity solutions do come at a premium as compared to the balance sheet liability and the lump-sum payment amounts but may be considered reasonable risk-adjusted prices for the true economic cost to the plan of delivering the promised pension benefits.

- Distribution of Annuities—Ongoing Plan: In the past, there was a concern that PBGC may oppose plan sponsors’ decisions to distribute annuity contracts with respect to benefits payable from an ongoing plan. The issue for PBGC was whether the use of third-party annuity contracts to pay pension benefits (without pursuing a more-formal plan termination process under PBGC guidelines)

16 See, e.g.,

et seq.17 DOL Interpretive Bulletin 95-1, 18 See, PBGC Request for Information, 19 PBGC decided not to take any further regulatory action or to provide specific guidance but indicated that it will continue to monitor industry practice to determine whether further regulatory guidance would be needed in the future.

With this acquiescence by PBGC, there was a general view that plan sponsors may eliminate certain of their pension liabilities by the purchase of annuity contracts from third-party annuity providers. Moreover, DOL regulations specifically authorize the transfer of pension benefit obligations to an insurance company as part of an annuity transaction.

Hughes Aircraft Co. v. Jacobson,

Notwithstanding the settlor’s ability to design a plan amendment to provide for the distribution of annuity contracts, the selection of an annuity provider involves the implementation of that decision and is very much a fiduciary decision that should conform to the requirements of DOL Interpretive Bulletin 95-1. Moreover, consideration may also be given to retaining an independent fiduciary to work with the plan fiduciaries to select a third-party annuity provider to ensure that plan sponsor financial considerations do not influence the final selection by the plan fiduciaries.

- Fiduciary Process for Annuity Purchases: While the process for selecting annuity providers is beyond the scope of this article, from a risk-mitigation standpoint, it is important to document the fiduciary process that is followed in selecting a group annuity contract provider. While DOL Interpretive Bulletin 95-1 provides guidance for the selection of the “safest available annuity,” it is important to note that the test of prudence by plan fiduciaries under ERISA is one of conduct not results.

22 Kirschbaum v. Reliant Energy, Inc., 526 F.3d 243 , 253, 43 EBC 2281 (5th Cir. 2008) (82 PBD, 4/29/08; 35 BPR 1034, 5/6/08).23 Compare Bussian v. RJR Nabisco, 223 F.3d 286 , 25 EBC 1120 (5th Cir. 2000)(27 BPR 1964, 8/22/00) (holding against the employer for failing to structure or conduct an independent and impartial investigation to select an annuity provider that would have been in the best interests of the participants) with Riley v. Murdock,890 F. Supp. 444 (E.D. NC 1995), aff’d83 F.3d 415 (4th Cir. 1996) (wherein the court found no fiduciary breach where pension committee retained independent advisers, conducted a thorough investigation of each insurer, and consulted with other employers that had purchased annuities from such insurers).

How to Move Forward With the De-Risking Strategy—Plan Governance

While it is obviously of critical importance to select the most appropriate de-risking strategy, strategies can be challenged and easily undermined if the plan sponsor does not have strong plan governance in place to effect these changes.

In determining how best to proceed with respect to pension de-risking strategies, plan sponsors must take care to establish and, more importantly, follow good plan governance. At the outset, it is important to distinguish the decisions to be made by the plan sponsor from the decisions to be made by the plan fiduciary in moving forward to de-risk pension obligations.

- Confirm Status of Decisionmaker: As noted earlier, plan design is a decision that is to be made by the plan sponsor in its settlor (nonfiduciary) capacity. To the extent that the de-risking strategy involves plan design, the plan sponsor will want to be sure to distinguish the process being followed by the corporate decisionmakers from decisions that may be made by plan fiduciaries in implementing such design decisions. Thus, for example, the plan sponsor should be certain to develop a record indicating that the action is being taken in a corporate capacity (This is particularly true when certain decisionmakers may have dual roles—being both corporate and fiduciary decisionmakers). It is also important for corporate decisionmakers not to confuse their respective roles, or engage in conduct that may be inconsistent with the corporate decisionmaking. Inconsistencies can arise when, for example, expenses incurred by corporate decision makers in evaluating alternative designs to the pension plan are paid from plan assets.

24 Expenses associated with assessing various alternative settlement strategies should normally be paid from corporate (not plan) assets. To the extent that the expenses associated with assessing various alternative settlement strategies are paid from plan assets, such payment may itself be a prohibited transaction under ERISA and may defeat any effort to assert an attorney-client privilege to protect such deliberations. See, e.g., Wildbur v. Arco Chemical Co., 974 F.2d 631 , 16 EBC 1235 (5th Cir. 1992) (when an attorney advises a plan administrator or other fiduciary concerning plan administration, the attorney’s clients are the plan beneficiaries for whom the fiduciary acts, not the plan administrator); see also, Washington-Baltimore Newspaper Guild, Local 35 v. Washington Star Co.,543 F. Supp. 906 , 909, 3 EBC 1741 (D.D.C. 1982). - Plan Documents and Amendments: To the extent that the employer has made a decision to de-risk its pension through any number of alternatives discussed above, it is important that the plan be amended to provide for such settlement activity (to the extent that the plan terms do not presently contemplate the specific activity).

25 In Lee v. Verizon Communications, 2012 U.S. Dist. BL 321438 (N.D. Tex. Dec. 7, 2012)(236 PBD, 12/11/12; 39 BPR 2413, 12/18/12), for example, while the court held for the plan fiduciary, the decision was noteworthy in that it underscored the potential areas that plaintiffs may assert in challenging a plan settlement strategy (e.g., plaintiffs alleged that, among other things, the plan fiduciary breached its fiduciary duties in purchasing annuity contracts for retirees when the plan document purportedly did not authorize such purchase). 26 Curtiss-Wright v. Schoonejongen, 514 U.S. 73 , 18 EBC 2841 (1995). - Plan Communications: The communication strategy associated with pension settlements has taken on increased importance in recent years. Clear and concise communications, along with ample time for participants to consider any pension settlement in which participants are required to make a decision, along with access to any necessary resources (e.g., financial advisers), are now critical elements of a pension settlement strategy. From a planning standpoint, each settlement strategy may introduce new communication considerations. There is a concern, for example, that the participant may select the lump sum in the interest of having access to immediate cash without fully appreciating the financial implications to his or her future (or current) retirement. The risk to the employer is that the participants receiving the lump sums may invest the assets poorly or use the money for nonretirement purposes such that, once the money is gone, they may find themselves short of income and return to the employer alleging that the employer misrepresented the impact of taking the lump sum and did not fully disclose all of the information important in making a lump-sum decision. While the prospect for litigation in this area may be years off, employers and plan fiduciaries need to be mindful of this potential exposure. To address this issue, employers planning to implement a settlement strategy should review their plan terms, prior disclosures, and previously distributed plan communications to confirm that they have reserved the right to modify plan terms and to terminate or otherwise modify plan provisions for current and former employees, whether in pay status or expecting to commence payments in the future. Moreover, in disclosing the information that would be material to the participant in making a decision to elect a pension settlement, factors such as loss of PBGC protection (by reason of a lump-sum payment or annuity distribution) and the elimination of lifetime and surviving spouse payments (for those electing the lump sum) should be considered in any plan disclosure. These and other disclosures may go a long way to mitigating the risk that individuals will allege, years later, that they were not properly informed of the material issues associated with the pension settlement offer.

27 For example, a participant may elect a lump-sum option out of concern that his or her employer may not be financially sound and may not be in business when the pension payments become due. The fact that PBGC may guarantee the payment of certain nonforfeitable benefits may be of interest to participants who are considering whether to leave their accrued benefits in the employer plan with the expectation of receiving annuity payments years in the future. See, e.g., - Serious Consideration of Strategies: The timing of the decision to offer a pension settlement alternative to participants is also of significant importance, particularly if the program may be offered during a time when participants may be in a position to decide on their pension benefits (e.g., should the participant take a lump sum from the pension plan out of concern that the employer’s long-term prospects may not be good, or wait and receive an annuity from a third-party insurance company that may be more protective with respect to a future income stream). Many times, the process for an employer to evaluate different alternatives can span many months and involve several false starts and changes in direction. At the same time, participants may be making retirement-related decisions that could be impacted by the final pension settlement strategy. While the employer has a duty to avoid material misrepresentations to plan participants, this duty does not require the employer to predict an ultimate decision to offer a pension settlement program so long as it fairly discloses the progress of its serious considerations to make a program available to affected employees. Indeed, the courts have noted that a fiduciary has a duty not only to inform a plan participant of new and relevant information as it arises, but also to advise him of circumstances that may impact decisions to be made by the participant.

28 Fischer v. Philadelphia Electric Company, 96 F.3d 1533 , 20 EBC 1905 (3rd Cir. 1996), cert denied,520 U.S. 1116 , 20 EBC 2656 (1997); McAuley v. IBM,165 F.3d 1038 , 22 EBC 2425 (6th Cir. 1999); see also, Berlin v. Michigan Bell Telephone Co.,858 F.2d 1154 , 1164, 10 EBC 1217 (6th Cir. 1988). - Consider Independent Fiduciary: Despite the best of intentions, plan fiduciaries who function in dual capacities (i.e., they have corporate responsibilities on behalf of the company and also are plan fiduciaries charged with acting on behalf of plan participants) may be challenged to defend their fiduciary actions. To the extent that there is a concern that fiduciary decisionmakers may be perceived as having a conflict of interest and may be taking action in the interest of the plan sponsor (and not plan participants), consideration may be given to retaining an independent fiduciary who can either advise the fiduciary committee, be a voting member of the committee, or ultimately be the final decisionmaker.

- Review Investment Committee Charters and Procedures: To the extent that the pension plan’s policies and procedures are well-developed and provide guidance at the committee level, employers need to be certain that such policies and procedures are followed or should amend the policies and procedures in advance of the action to be taken. As part of this review, it may present a good opportunity to remind plan fiduciaries of their responsibilities and that their actions are to be taken in the best interest of the plan participants. As noted earlier, having procedures is not the same as following the procedures—employers should document that each procedure has been followed by the appropriate parties.

- Document Actions Taken: Despite efforts to make the correct decision, the absence of a strong written record can undermine even the most prudent decisions. In memorializing the action taken, whether in a settlor or a fiduciary capacity, it is important that the record indicate the capacity in which the decisionmakers acted (settlor or fiduciary), the documentation considered and relied upon, alternatives considered, and any independent third parties brought in to advise the decisionmakers. To the extent that this written record is created at or about the time of the action taken, it will go a long way to supporting the prudence of the action taken.

Conclusion

Pension risk management strategies can be most effectively managed by integrating some or all of the above strategies. What may work best for one employer, however, may be inappropriate for other employers. From the perspective of the employer and prudent plan fiduciary, the task of reducing risk within a defined benefit plan may be most effectively achieved by deploying various alternatives into a single, coherent strategy based on the employer’s particular situation. While plan design and asset allocation studies are often critical first steps, employers and plan fiduciaries will benefit significantly by evaluating the alternative strategies. While the employer may ultimately choose to pursue some, all, or none of these strategies, having evaluated the alternatives and made a conscious decision as to how to proceed will provide support to the employer and plan fiduciary to the extent that there are any future challenges or claims by participants and beneficiaries with respect to managing pension plan risks.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.