The nature of uncompleted real estate projects is different from those of pure operating enterprises and completed real estate projects. This difference presents unique restructuring challenges. This article discusses various issues relating to financing distressed real estate projects, both in out-of-court workouts and in bankruptcy. Additionally, this article addresses some of the unique problems presented by uncompleted real estate projects and possible solutions to these problems.

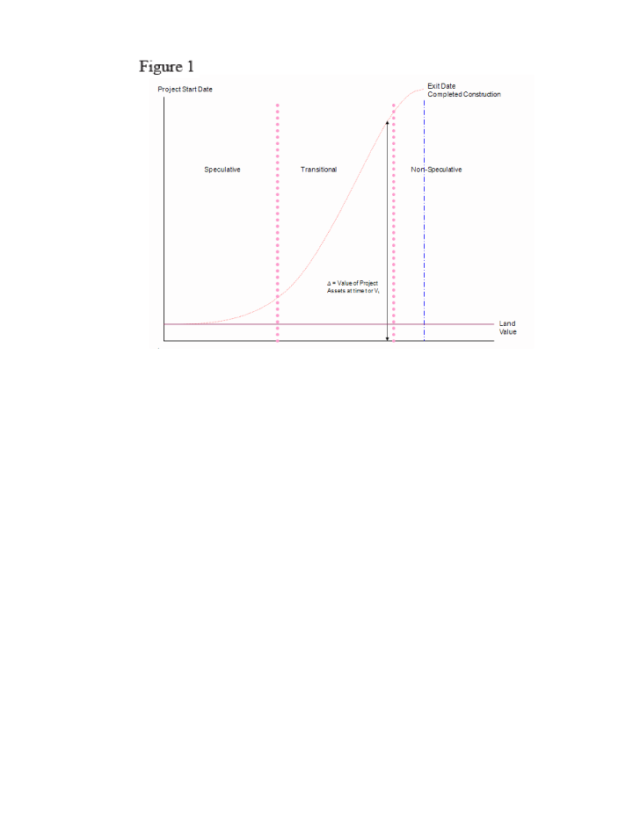

To aid the analysis, this article divides distressed real estate projects into three categories, depending on their development risk: speculative, transitional, and non-speculative. Speculative projects are projects where construction progress is so limited, or commercial circumstances have so changed, that project completion and the achievement of stable revenues is uncertain. The value of the existing real estate improvements is at or near zero, and the liquidation value of such assets may be near the land value less costs, such as demolition, etc.

Transitional projects are characterized by a significant measure of completion and pre-selling of the project. Completion of the project and the achievement of stable revenues is likely (although not certain) as long as sufficient liquidity is provided to fund the project to completion. The potential increase in value caused by real estate improvements involves some development risk, but less than at the earlier stages of the project, with such risk declining rapidly as the development of the project progresses. The liquidation value of the property at this stage of development reasonably could be valued based upon the expected value of the project after completion (discounted for development risk), less the cost of completion of the project.

Non-speculative projects are characterized by substantial completion and pre-selling of the project such that completion of the project and the achievement of stable revenues are relatively certain as long as sufficient liquidity is provided to the project to fund its completion. The liquidation value of such property is the value of the completed project less the cost of completion, with little or no discount attributable to development risk.

Although the financial and risk characteristics of each real estate project are different, it is generally the case that the speculative risks of the project decline as completion of a successful project becomes more certain. In other words, the valuation of a given real estate project increases as the project becomes less speculative. Rather than a straight-line increase in value that corresponds with incremental expenditure, the increase in value represented by the shrinking of project risk that results from additional development will likely produce a valuation curve in the shape of a flattened “S” (similar to that depicted in Figure 1 below). This S-shaped curve reflects that, over time, project value increases at a slow rate, which then increases more rapidly, and finally slows. The S-shaped curve reflects a period during which the speculative nature of the project changes at a significantly faster rate than at different periods during the life of the project until the speculative element of the project becomes, as the project develops to completion, a negligible feature of its valuation.

Imagine a commercial real estate project that is a certain amount of dollars away from completion of construction and sufficient sale or lease to operate profitably. Assume this hypothetical project has insufficient liquidity and cannot be completed without an injection of additional capital.

The necessary additional capital may be provided in an out-of-court restructuring either as debt or equity, which will depend upon, among other things, who is willing to put in the additional capital, the amount of risk involved (i.e., how speculative the project is given its current stage of development), and the negotiating leverage of the parties. Most likely, each constituent will have a different point of view. The secured lender may see that it can recognize the upside of the completed project by foreclosing, credit bidding, and completing the project with its own or third party capital. By contrast, the existing equity may seek to preserve the upside of a completed project but will be reluctant to give the project’s secured lender a free ride by providing the additional liquidity as equity, rather than as additional debt. If neither the senior lender nor the equity have the appetite for injecting additional capital, both may be willing to permit a third party to provide it.

The outcome of negotiations among the various stakeholders in the project will also be informed by the possible outcomes of a restructuring in a bankruptcy. The bankruptcy of the real estate project, while adding additional execution risks associated with all bankruptcy proceedings, provides the party willing to provide additional funding with leverage not available outside a bankruptcy, namely, the ability to consummate a transaction over the objections of other parties (whose consent, in an out-of-court restructuring, would be necessary). Accordingly, the threat of bankruptcy—and, more importantly, each party’s view of whether such transaction could successfully be implemented in a proceeding—will influence out-of-court negotiating dynamics, adding pressure to out-of-the-money creditors to compromise their claims and other creditors to seek negotiated solutions.

Evaluating the dynamics of a Chapter 11 case must be informed, in the first instance, by understanding how the value of the uncompleted project will be affected by the injection of new capital. To do so, we look to our previous depiction of project value, illustrated in Figure 1, and study two hypothetical bankruptcy features: the petition date and the effective date of the Chapter 11 plan. As is clear from Figure 1 above, where the petition date and exit date fall relative to the S-shaped curve showing value will materially affect the posture of the case.

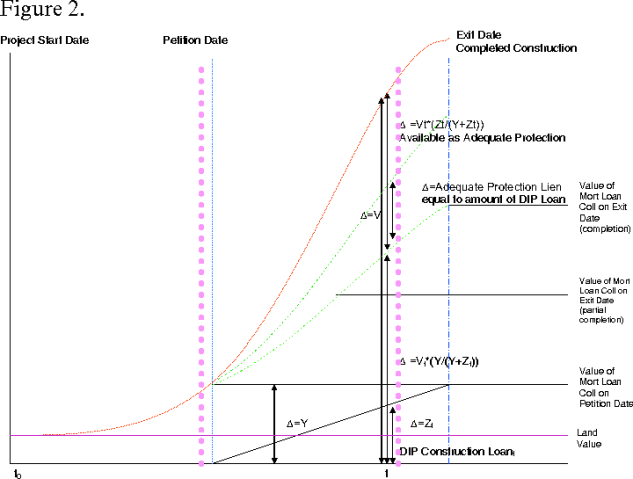

One means of funding construction in a bankruptcy case could be a postpetition loan. Postpetition loans are given superpriority administrative expense status under Section 503(b) of the Bankruptcy Code, meaning that a plan cannot be confirmed if such claim is not paid in full in cash on the effective date of the plan (unless such holder consents to a different treatment).

To prime an existing secured lender with a new secured postpetition loan, the debtor must be able to show, pursuant to Sections 364(c) and (d) of the Bankruptcy Code, that the debtor is unable to obtain unsecured credit, unable to obtain credit that is secured by a junior lien on the property, and that the interest of the holder of a lien on the property of the estate on which the senior lien is proposed to be granted is adequately protected.

To illustrate, assume that the sole secured financial creditor of the unfinished project is out of the money on the petition date (i.e., on the petition date, the amount of the secured lender’s claim is greater than the liquidation value of the collateral (land and partially completed improvements)). Pursuant to Section 361 of the Bankruptcy Code, adequate protection can be provided to such secured lender in one (or more) of the three following ways: (1) the court may order that the debtor provide periodic cash payments to the senior lender; (2) the court may order that the debtor grant to the secured lender an additional or replacement lien on assets to the extent that the priming lien results in a decrease in the value of the secured lender’s interest in the property; or (3) the court may order other relief resulting in the provision of the indubitable equivalent of the decrease in value of such secured lender’s interest in the property.

Although a secured lender may have a lien on all of the assets of the debtor prior to the commencement of a case in bankruptcy, this does not mean that its lien extends to all the increase in value created in the debtor’s assets after the commencement of a case. For instance, pursuant to Section 552 of the Bankruptcy Code, the postpetition effect of a prepetition grant of security is limited. Property (other than proceeds, products, offspring or profits of prepetition collateral) acquired by the estate after the petition date, is not subject to any lien resulting from any security agreement entered into by the debtor prior to the petition date.

Imagine that the project in question is, on the petition date, a partially built and partially sold time-share hotel that commenced bankruptcy to address a liquidity crisis caused by cost overruns. Assume that, during the bankruptcy case, the construction of the time-share hotel can be completed, as can sales of the balance of the time shares, to the point of a viably developed and occupied time-share hotel. During the progress of the construction in the bankruptcy case, raw materials and labor are purchased to finish the build-out and sell the project. To the extent that proceeds of a postpetition loan are used for the build out and sale and lease of the completed project, the value created by the postpetition accessions to the structure and sales arguably can be considered property acquired postpetition.

Looking again at Figure 1, the flattened S shape of the value curve of the real estate project implies significant accretion in the value of the commercial real estate project roughly during the transition period during which the project changes from speculative to non-speculative. A portion of the increase in the collateral value is attributable to the added value of prepetition property resulting from improvements and sales existing on the petition date, and some portion of the increase in collateral value is also due to the accretion in value of the collateral created by the additional construction and additional sales funded by the postpetition financing.

A prepetition lender is generally entitled under Section 552 of the Bankruptcy Code to “the proceeds, products, offspring and products” of its collateral “acquired by the estate.” Thus, each dollar of additional construction can be said to add additional value to the project, some of which is “profits” or “products” of prepetition collateral, some of which is “profits” or “products” of, and postpetition construction and sales, and some of which is accretion of the value of the postpetition construction and sales.

Commingled collateral problems have long been resolved, in the personal property context, by attributing accreted value in proportion to the value contributed with respect to the goods commingled in a mass.

This amount of postpetition assets on which a lien arguably can be granted as adequate protection can be expressed in simple arithmetic for all relevant times during the case. If the value of the collateral on the petition date is “Y” and, at any given time “t,” the value of the additional construction is “Zt” and the project value is “Vt,” then:

The proportion of the collateral in which the senior lender has an interest on account of its prepetition security interest can be expressed as:

Vt*(Y/(Y+Zt))

And the proportion of collateral in which the senior lender does not have interest and, therefore, is available to serve as adequate protection can be expressed as:

Vt*(Zt/(Y+Zt))

Note that Y is not designated with t because Y is a constant value in the case while Z is designated with t because Z increases as additional value is added as the project develops toward completion over time. In other words, at any point in time the value of the prepetition collateral (assumed for simplicity to be all assets on the petition date) is measured as of the petition date, while the value of postpetition additions to the real estate assets increases over time with the postpetition project expenditures and resulting build-out.

The Bankruptcy Code requires that the replacement lien or lien on additional collateral be only “to the extent that the [priming lien] grant decreases such entity’s interest in collateral.”

The secured lender might argue that the case will generate administrative expenses in excess of the postpetition accretion in value available for adequate protection. To overcome this argument, the debtor must show (among other things) that the accretion in value to the prepetition collateral resulting from postpetition liquidity injection exceeds the administrative expenses of the case.

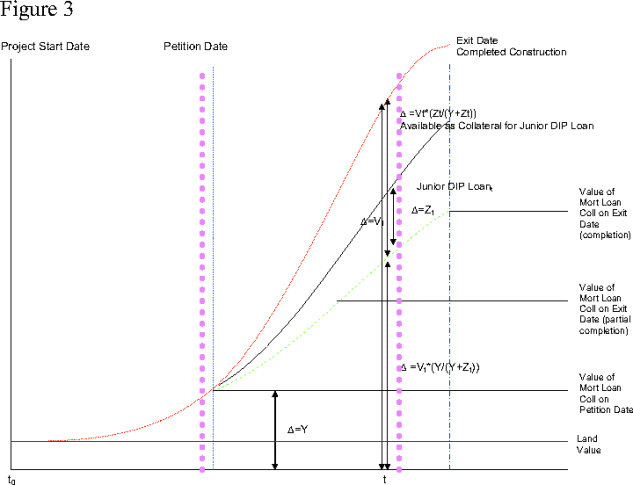

The same calculations described above relative to a priming postpetition loan could be applied to a postpetition loan that would be junior to the prepetition secured loan. In the case of a junior postpetition loan, the junior lender bears the risk of an unexpected decline in the value of the collateral. There is no serious question of adequate protection since there is no diminution in value of the prepetition secured lenders interest in the property resulting from the postpetition junior loan. Hybrid arrangements of junior and senior loans are also possible ways of addressing the concerns. Figure 3 below is a graphic depiction of a postpetition loan junior to the liens of the senior lender on the petition date.

The foregoing financing approaches are, of course, relatively simple to apply to a case where there are limited constraints on case duration allowing for completion of construction. In a bankruptcy, however, one of the first questions will be whether the real estate project is determined to be “single asset real estate” (SARE) as defined in Section 101 of the Bankruptcy Code.

any single property or project, other than residential real property with fewer than 4 residential units, which generates substantially all of the gross income of a debtor who is not a family farmer and on which no substantial business is being conducted by a debtor other than the business of operating the real property and activities incidental. 11 U.S.C. §101(51B).

Many real estate projects will satisfy this definition. If determined to be a SARE, the senior creditor may move under certain circumstances for relief from the automatic stay.

with respect to a stay of an act against single asset real estate under subsection (a), by a creditor whose claim is secured by an interest in such real estate, unless, not later than the date that is 90 days after the entry of the order for relief (or such later date as the court may determine for cause by order entered within that 90-day period) or 30 days after the court determines that the debtor is subject to this paragraph, whichever is later (A) the debtor has filed a plan of reorganization that has a reasonable possibility of being confirmed within a reasonable time; or (B) the debtor has commenced monthly payments that (i) may, in the debtor’s sole discretion, notwithstanding section 363(c)(2), be made from rents or other income generated before, on, or after the date of the commencement of the case by or from the property to each creditor whose claim is secured by such real estate (other than a claim secured by a judgment lien or by an unmatured statutory lien); and (ii) are in an amount equal to interest at the then applicable nondefault contract rate of interest on the value of the creditor’s interest in the real estate;

Id. at §362(d).

A SARE debtor must be prepared to propose different arrangements, which almost certainly require the rapid filing of a plan and disclosure statement, and a quick confirmation and effective date in order to avoid a successful motion by the prepetition secured lender for relief from the automatic stay. Obviously, whether a project is determined to be a SARE will materially affect the debtor’s options in the case (and will impact the strength of prepetition negotiating positions in an out-of-court restructuring).

Such a determination does not necessarily foreclose the debtor’s control over the case, however. First, even if the SARE debtor is unable to provide a plan within the 90-day period contemplated by Section 362(d) of the Bankruptcy Code, the SARE debtor may be able to avoid a dismissal of its case if, as additional adequate protection, it has a source of liquidity sufficient to keep current on its interest obligations to the secured lender. In light of this, a SARE debtor might need to consider bankruptcy earlier as a means of preserving some liquidity, although this would affect valuations and speculative risk at the time of filing.

In addition, for certain projects, the debtor will argue that it is not a SARE debtor. Courts typically consider three criteria to determine whether a debtor constitutes a SARE debtor: (1) whether the debtor owns a single property or project; (2) whether real property generated substantially all of the debtor’s income (i.e., does the sale of the property constitute all or substantially all of the income of the debtor, or does the debtor derive income from other sources (e.g., operation of restaurants, golf courses, spas, etc.), and (3) whether the debtor is involved in any substantial business other than the operation of its real property and activities incident to it.

It bears noting that, in Kara Homes, the bankruptcy court rejected the Kara debtors’ arguments that they were not a SARE debtor.

The Kara Homes court rejected these arguments and held that the debtors were each a SARE debtor. In so holding, the Kara Homes court noted that “to build and sell homes, it is often necessary to acquire the land on which to build homes, and plan the community in which they lie [and] market those homes for sale and maintain the properties.”

The Kara Homes decision has been criticized. The focus of this criticism centers on the Kara Homes court’s rejection of the argument that the development and sale of real estate constitutes the business of operating real property. The SARE debtor provisions of the Bankruptcy Code were added to address situations where a debtor owns property passively, and simply collects rents as a result of ownership. The development and sale of properties is not a passive activity, nor does it relate to simply the business of operating real property. While it is true that the Kara Homes affiliates simply owned the property and the parent engaged in other businesses, given that the enterprise was run as a single integrated operation, it appears inappropriate to separate the activities of the parent from the holdings of the affiliates.

Even if the court does not hold that the debtor is a SARE (or relief from the automatic stay is otherwise avoided), there would still be challenges to confirming a Chapter 11 plan if the priming loan has not been repaid and the project is not completed prior to confirmation. Assuming that the secured lender will object to confirmation of the plan, two hurdles must be surmounted. First, the debtor must identify an impaired accepting class, Second, the debtor must ensure that the plan can be confirmed over the secured creditors’ objection. Under the Bankruptcy Code, a Chapter 11 plan can be confirmed over the “no” vote of a secured creditor class if: (i) the collateral is sold and the secured lender’s lien attaches to the proceeds, (ii) the secured creditor receives the “indubitable equivalent” of the allowed amount of its secured claim, or (iii) the secured lender becomes a lender under a new loan.

Postpetition financing provided on a priming basis creates material grounds for a challenge if the debtor seeks to convert the postpetition loan into an exit facility that is senior to the new loan provided to the prepetition secured. On the one hand, the prepetition secured lender will argue that it is not retaining its liens if the postpetition financing converts to priming exit financing. On the other hand, the debtor will argue that the value of the collateral has increased sufficiently, as a result of improvements, and that the prepetition secured lender receives a junior lien on post-exit collateral that are worth more than its prepetition first priority lien the prepetition collateral. If the arguments with respect to adequate protection have held good—i.e., that the additional liens on collateral equal the decrease in value of the prepetition secured lender’s interest in the collateral—then the arguments supporting a post-exit second lien behind the exit facility arguably likewise hold good.

Alternatively, the debtor may argue that the prepetition secured lender will receive the “indubitable equivalent” of its claim by virtue of the issuance of new debt on market terms secured by a second lien on all of the collateral. The prepetition secured lender will argue against the proposition that the increase in collateral value is sufficient for the debtor to show, that it is “too evident to be doubted”

This article has explored restructurings of uncompleted real estate projects with a view toward the unique challenges presented by such assets. Both out of court and in restructuring situations will be influenced by the possibility of providing financing in a case that will lead to a reorganization of the debtors’ assets. This article provides a framework for analysis of the circumstances and the valuation dynamics of a distressed project and possible financing scenarios related thereto. The effect of recourse guaranties, completion guaranties, and intercreditor relationships are left to be separately evaluated, although they are likely to bear significantly—and in some cases, decisively—on the analysis.

Learn more about Bloomberg Law or Log In to keep reading:

See Breaking News in Context

Bloomberg Law provides trusted coverage of current events enhanced with legal analysis.

Already a subscriber?

Log in to keep reading or access research tools and resources.